Navigating the 2025 Texas Dental Fee Schedule: A Comprehensive Guide for Patients and Providers

The landscape of healthcare costs is perpetually shifting, a complex mosaic of economic pressures, regulatory changes, and technological advancements. For millions of Texans, understanding the cost of essential services like dental care is not merely a matter of financial planning but a significant factor in accessing and maintaining oral health. As we look toward 2025, the dental fee schedule in Texas stands at a critical juncture, influenced by persistent inflation, evolving insurance contract structures, and the state’s unique demographic and economic profile. This article aims to be the definitive guide to this complex topic, dissecting the forces that shape dental pricing, providing a detailed analysis of expected costs for common procedures, and offering actionable strategies for both patients and dental practices to navigate the financial aspects of oral healthcare effectively. We will move beyond simplistic price lists to explore the very mechanics of how fees are determined, demystifying terms like UCR (Usual, Customary, and Reasonable), PPO allowable amounts, and the profound difference between a fee schedule and what a patient actually pays. Whether you are a patient concerned about your family’s budget, an employer designing a benefits package, or a dental professional striving for a sustainable practice, the insights that follow will equip you with the knowledge needed to make informed decisions in the evolving Texas dental market of 2025.

1. Understanding the Concept of a Dental Fee Schedule

What is a Dental Fee Schedule? It’s Not a Single Price List

A common misconception is that there exists a single, universally mandated “dental fee schedule” for Texas that all dentists must follow. In reality, the American dental care system is predominantly private and market-driven. Therefore, a dental fee schedule is best understood as the comprehensive list of charges that a dental practice sets for every procedure and service it offers. This is known as the Full Fee or UCR Fee (a term we will explore in depth). Crucially, this is the price charged to a patient who has no dental insurance or whose insurance plan pays based on the practice’s full fee schedule.

However, the story becomes significantly more complex when dental insurance is introduced. Each dental insurance company negotiates its own Allowed Amount or PPO Fee with dentists who choose to join their network. In exchange for being listed as a “preferred provider” and receiving patient referrals from the insurer’s directory, the dentist agrees to accept this lower, pre-negotiated fee as payment in full for covered services. This means that for any given procedure, there are at least two potential prices: the dentist’s full UCR fee and the discounted PPO allowable fee for patients with that specific insurance. This layered system is the primary reason for confusion and frustration among patients.

The Key Players: Dentists, Insurance Companies, and Patients

The dynamics of the dental fee schedule are governed by the interactions between three core entities:

-

The Dental Provider: The dentist or dental practice is a business that must cover its overhead—rent, staff salaries, state-of-the-art equipment, supplies, insurance, and continuing education—while also generating a profit. They establish their UCR fee schedule based on these costs, their level of expertise, the local market, and the perceived value of their services. They have the autonomy to set their fees but are constrained by market competition and insurance contracts.

-

The Insurance Payer: Insurance companies act as intermediaries. They collect premiums from individuals or employers and pool the risk. To control their costs, they create networks of providers who agree to discounted rates. Their primary interest is in managing their financial liability, which often leads to fee schedules that may not keep pace with a practice’s rising costs.

-

The Patient: The patient is the consumer of dental services and, ultimately, the financier, either directly through out-of-pocket payments or indirectly through insurance premiums and co-pays. The patient’s financial responsibility is determined by the complex interplay between the dentist’s UCR fee, the insurance company’s allowed amount, and the specific terms of their benefit plan (deductibles, co-insurance, annual maximums).

UCR (Usual, Customary, and Reasonable): The Myth of “Standard” Pricing

The term “UCR” is often used but widely misunderstood. It is not a government-mandated price nor a median price for a region. Instead, it is a methodology used by insurance companies to determine the “reasonableness” of a dentist’s fee when the dentist is out-of-network.

-

Usual: The fee that a specific dentist most frequently charges for a given procedure.

-

Customary: The range of fees charged by dentists of similar training and experience within a specific geographic area.

-

Reasonable: A fee that is justifiable for a particularly complex or unusual procedure.

For example, if an out-of-network dentist in Houston charges $1,500 for a crown, the insurance company will check this against its UCR data for Houston. If their data shows that the “customary” range for crowns in Houston is $1,200 to $1,400, they may deem only $1,400 as “reasonable.” They will then calculate their payment (e.g., 50% of $1,400 = $700) based on that lower figure, leaving the patient responsible for the $200 “overage” ($1,500 – $1,400) plus their 50% co-insurance, leading to a significant surprise bill. This highlights why understanding network status is critical for patients.

2. The Major Forces Shaping the 2025 Texas Dental Fee Landscape

The dental fee schedule for 2025 is not created in a vacuum. It is the direct result of a confluence of powerful economic, social, and technological forces. Understanding these drivers is key to anticipating changes and contextualizing the numbers.

The Inflationary Hangover: Economic Pressures on Practice Costs

The high inflation rates of the early 2020s have had a lasting impact, creating a new, elevated cost baseline for dental practices. Everything from utilities and rent to the cost of dental supplies—gloves, masks, anesthetic, composite resin, and ceramic blocks for crowns—has seen a permanent step-up in price. A box of gloves that cost $10 in 2020 may now cost $16. This increased cost of goods sold (COGS) must be absorbed by the practice and is a primary factor necessitating fee increases to maintain profitability and sustainability.

The Labor Squeeze: Rising Salaries for Dentists, Hygienists, and Assistants

The healthcare labor market remains exceptionally competitive. There is a high demand for skilled dental hygienists and assistants, leading to upward pressure on wages and benefits to attract and retain top talent. Furthermore, new dental graduates often enter the profession with significant student debt, influencing their earning expectations and the fees they must charge to service that debt and establish a practice. This upward trend in labor costs, which typically constitutes the largest portion of a practice’s overhead, is a non-negotiable driver of fee schedule adjustments.

Technological Investment: The Cost and Benefit of Digital Dentistry

The digital transformation of dentistry has brought about remarkable improvements in patient care, comfort, and efficiency. Technologies like intraoral scanners (replacing messy impressions), CAD/CAM systems for same-day crowns, and cone-beam CT (CBCT) scanners for advanced imaging represent significant capital investments—often totaling hundreds of thousands of dollars. While these technologies can improve workflow and patient satisfaction, they also carry substantial costs for acquisition, maintenance, and training. To justify this investment and achieve a return, practices often incorporate a premium into their fees for procedures utilizing this advanced technology.

Regulatory and Compliance Burdens: The Hidden Cost of Doing Business

Dental practices in Texas must navigate a complex web of state and federal regulations. This includes compliance with the Health Insurance Portability and Accountability Act (HIPAA), OSHA standards for infection control, and state board regulations. Meeting these standards requires ongoing training, updated documentation, and often, investment in specific software or equipment (e.g., secure patient portals, medical waste disposal services). These “hidden” costs of compliance contribute to the practice’s overhead and, by extension, influence the fee schedule.

Geographic Disparities: Why Fees in Plano Differ from Those in Lubbock

Texas is a vast and economically diverse state. The cost of living and operating a business in a high-density, affluent suburban area like Southlake or The Woodlands is substantially higher than in a rural community in the Panhandle. This disparity is directly reflected in dental fee schedules. A practice in an area with high commercial rent, high property taxes, and a patient base with a higher average income will typically have a higher UCR fee schedule than a practice in a lower-cost rural area, even for identical procedures.

3. A Detailed Breakdown of Common Procedures and Projected 2025 Fees

To translate these abstract forces into tangible numbers, let’s examine a projected range of fees for common dental procedures in Texas for 2025. The table below provides a synthesized model based on analysis of current trends, economic data, and industry reports. It is critical to remember that these are estimated ranges and actual fees will vary by practice, location, and case complexity.

Projected 2025 Texas Dental Fee Ranges for Common Procedures

| Procedure Code | Procedure Name | Description | Projected 2025 UCR Fee Range (Texas) | Projected 2025 PPO Allowed Range (Estimated) |

|---|---|---|---|---|

| D0120 | Periodic Oral Evaluation | Routine exam | $75 – $125 | $50 – $80 |

| D0150 | Comprehensive Oral Evaluation | New patient exam | $125 – $200 | $90 – $140 |

| D0274 | Bitewing X-Rays (4 films) | Cavity-detecting X-rays | $75 – $150 | $55 – $100 |

| D0330 | Panoramic X-Ray | Full jaw X-ray | $125 – $250 | $90 – $175 |

| D1110 | Adult Prophylaxis (Cleaning) | Routine cleaning | $100 – $175 | $75 – $120 |

| D1208 | Topical Fluoride (Adult) | Preventive fluoride treatment | $35 – $65 | $25 – $45 |

| D1351 | Sealant (per tooth) | Plastic coating for grooves | $45 – $75 per tooth | $30 – $55 per tooth |

| D2140 | Amalgam Filling (1-surface) | Silver filling | $150 – $250 | $110 – $180 |

| D2391 | Composite Filling (1-surface) | Tooth-colored filling | $175 – $325 | $125 – $225 |

| D2330 | Composite Filling (2-surfaces) | Tooth-colored filling | $225 – $425 | $160 – $300 |

| D2750 | Crown – Porcelain Fused to Metal | Cap for a tooth | $1,200 – $1,800 | $900 – $1,300 |

| D2740 | Crown – All Ceramic / Porcelain | Tooth-colored cap | $1,400 – $2,200 | $1,000 – $1,600 |

| D4341 | Periodontal Scaling & Root Planing (per quadrant) | Deep cleaning for gum disease | $250 – $450 per quad | $180 – $320 per quad |

| D6010 | Surgical Extraction (Single Tooth) | Removal of a tooth requiring surgery | $250 – $600 | $180 – $425 |

| D7240 | Surgical Extraction (Impacted Tooth) | Removal of a wisdom tooth | $350 – $800+ per tooth | $250 – $600+ per tooth |

| D9220 | Deep Sedation / General Anesthesia (first 30 mins) | Anesthesia services | $350 – $650 | Varies Widely |

| D6065 | Implant Abutment | Connector piece for implant crown | $450 – $800 | $350 – $600 |

| D6056 | Implant Crown (Custom Abutment) | Crown on an implant | $1,800 – $3,200 | $1,300 – $2,300 |

Note: PPO Allowed Ranges are estimates and will vary significantly by insurance carrier and specific contract.

Preventive Care: Prophylaxis, Examinations, and Radiographs

Preventive care is the foundation of oral health and, from a cost perspective, represents the best value for patients. The fees for a routine adult prophylaxis (cleaning) and examination are projected to see moderate increases into the $100-$175 range. While this may seem straightforward, it’s important to note that many insurance plans cover preventive services at 100%, meaning the patient’s out-of-pocket cost may be $0 if they are in-network and have no additional fees for a perio check. However, if a patient presents with signs of gum disease and requires a more involved procedure like scaling and root planing (“deep cleaning”), the cost escalates significantly, as this is typically categorized as a “basic” or “periodontal” service with co-insurance applied.

Basic Restorative: Amalgam and Composite Fillings

The shift from silver amalgam fillings to tooth-colored composite resins is nearly complete, driven by patient demand for aesthetics and the adhesive properties of composite that often allow for more conservative tooth preparation. As shown in the table, a one-surface composite filling is projected to range from $175 to $325. The fee increases with the number of surfaces involved. The choice of material can also be a point of insurance contention; some older plans may still reimburse at the lower amalgam rate, leaving the patient responsible for the difference in cost for the composite.

Major Restorative: Crowns, Bridges, and Dentures

This category represents some of the most significant investments in dental care. A crown, required to restore a tooth that is broken, heavily decayed, or has had a root canal, is a complex procedure involving multiple steps and laboratory fees. The projected UCR fee for an all-ceramic crown in 2025 is $1,400 to $2,200. The type of material (PFM, e.max, zirconia) influences the cost, with high-strength zirconia offering exceptional durability and aesthetics at a premium. For patients missing teeth, a fixed bridge or partial denture involves even more laboratory work and planning, with costs scaling accordingly. It is in this category that patients most frequently encounter the limitations of their annual maximum benefit, often $1,000-$1,500, which may cover only a fraction of a single crown.

Endodontics: Root Canal Therapy

Root canal therapy, often feared but financially significant, involves the removal of infected pulp from inside a tooth. Fees are highly dependent on the tooth in question, with front teeth (incisors) having a single canal being less expensive than molars, which can have three or four canals. A molar root canal (DCode D3348) could range from $1,200 to $2,000 or more. Many patients are referred to endodontic specialists for this procedure, who may have a higher fee schedule reflecting their advanced training and specialized equipment.

Periodontics: Scaling and Root Planing

As mentioned, this “deep cleaning” is the primary non-surgical treatment for periodontitis (gum disease). It is typically billed by quadrant (one of the four sections of the mouth), with fees per quadrant projected at $250-$450. A full-mouth treatment would therefore involve four separate quadrant fees, representing a substantial financial outlay. Insurance coverage for periodontal services is often less generous than for basic restorative care, with co-insurance rates of 50-80% being common.

Oral Surgery: Simple and Surgical Extractions

The cost of a tooth extraction varies dramatically based on complexity. A simple extraction of a visibly loose tooth might be in the $150-$300 range. However, a surgical extraction, requiring incision and bone removal (common for wisdom teeth), can cost $350-$800 per tooth. The addition of sedation or general anesthesia adds several hundred dollars more. This is a key area where a pre-treatment estimate from the insurance company is vital to avoid unexpected bills.

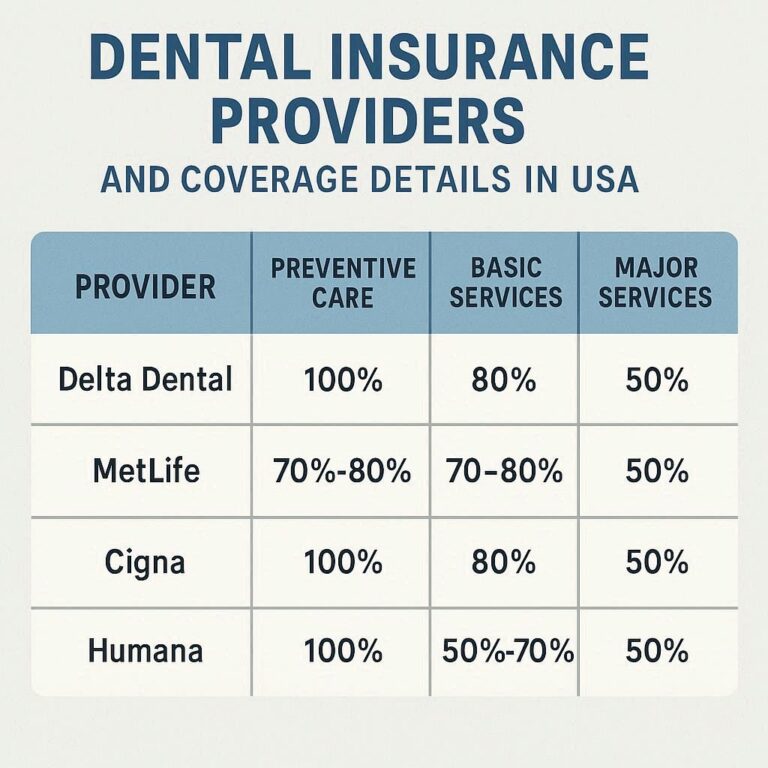

4. The Insurance Lens: How PPOs, HMOs, and Medicaid Dictate What You Pay

Understanding the type of dental plan you have is arguably more important than knowing the dentist’s UCR fee schedule, as it is the plan that ultimately determines your financial responsibility.

The PPO Model: Discounted Fee Schedules and Network Participation

Preferred Provider Organization (PPO) plans are the most common type of dental insurance. The model is built on a trade-off:

-

For the Patient: You get a larger network of providers and the flexibility to see out-of-network dentists (though at a higher cost). Your out-of-pocket costs are determined by the insurer’s lower “allowed amount.”

-

For the Dentist: They gain access to a stream of patients from the insurer’s directory but must accept a discounted fee, which may be 20-40% below their UCR.

The critical concept for PPO patients is the Annual Maximum. This is the total amount the insurance will pay for covered services in a benefit year (typically $1,000-$1,500). Once this cap is reached, the patient is responsible for 100% of the dentist’s UCR fee. This maximum has remained stagnant for decades, failing to keep pace with inflation and the rising cost of dental care, making it a significant point of frustration.

HMOs (Capitation Plans): A Fixed Monthly Fee per Patient

Dental Health Maintenance Organizations (DHMOs or HMOs) operate on a capitation model. The insurance company pays the dentist a fixed monthly fee (a “capitation” payment) for each patient enrolled in their practice, regardless of whether that patient receives care. In return, the dentist agrees to provide specific services to the patient for very low co-pays (e.g., $10 for a cleaning, $25 for a filling). While this can be affordable for patients seeking basic care, it can create a financial disincentive for the dentist to perform more complex procedures, and the network of providers is typically much more restricted than with a PPO.

Texas Medicaid (STAR Health & CHIP): A Government-Mandated Fee Schedule

Texas Medicaid operates on a true, state-mandated fee schedule. The state sets the maximum amount it will pay for every single dental procedure covered under the program for children (CHIP) and limited adult benefits. This fee schedule is notoriously low, often 30-50% below the average PPO allowed amount. As a result, many dentists cannot afford to participate in the Medicaid program because the reimbursement does not cover their overhead. This creates significant access-to-care issues for low-income populations in Texas.

Understanding Your Explanation of Benefits (EOB)

The EOB is not a bill but a critical document that explains how the insurance company processed a claim. It deciphers the financial transaction:

-

Total Charge: The dentist’s UCR fee.

-

Plan Discount: The difference between the UCR and the allowed amount (if in-network).

-

Allowed Amount: The negotiated rate the insurance recognizes.

-

Plan Pays: The insurance’s portion (e.g., 80% of the allowed amount).

-

Patient Responsibility: Your portion, including any deductible, co-pay, and co-insurance.

Reading your EOB carefully is the single best way to understand what you are being charged for and why.

5. Strategies for Patients: Managing Out-of-Pocket Dental Costs in 2025

Facing rising dental costs requires a proactive and strategic approach.

The Power of Preventive Care: The Most Cost-Effective Investment

The most powerful financial strategy in dentistry is prevention. Investing in twice-yearly cleanings and exams, which are often fully covered by insurance, is exponentially cheaper than waiting for a small cavity to become a large one requiring a root canal and crown, which could cost thousands of dollars out-of-pocket.

Maximizing Your Dental Insurance Benefits

-

Know Your Plan: Understand your annual maximum, deductible, and coverage percentages for different procedure types.

-

Use Your Benefits: If you have unused benefits at the end of the year, schedule treatment before they expire.

-

Time Major Procedures: If you need two crowns and have a $1,500 maximum, consider getting one crown in December and the second in January to utilize two years’ worth of maximums.

Exploring Alternative Payment Options: Dental Savings Plans and In-House Membership Clubs

Many practices now offer in-house membership plans for uninsured patients. For an annual fee (e.g., $300-$400 for an individual), patients receive preventive care (exams, cleanings, X-rays) for free or at a steep discount, plus a percentage off other services. These plans are often a better value than traditional insurance for patients who do not have access to an employer-sponsored plan.

Dental savings plans, offered by companies like Careington or Aetna Dental Access, are not insurance. They are discount programs where you pay an annual fee to access a network of dentists who have agreed to provide services at a pre-negotiated discount.

The Importance of Pre-Treatment Estimates

For any procedure expected to cost more than a few hundred dollars, always request a pre-treatment estimate from your dentist. They will submit a proposed treatment plan to your insurance company, which will then send back an EOB showing exactly what they will cover and what your out-of-pocket cost will be. This eliminates surprises.

Seeking Care at Dental Schools and Federally Qualified Health Centers (FQHCs)

For patients with severe financial constraints, dental schools (like the UT Health San Antonio School of Dentistry) and FQHCs are excellent options. Care is provided by dental students (under faculty supervision) or at a sliding-scale fee based on income, making comprehensive care much more affordable, though often with longer appointment times.

6. Strategies for Dental Providers: Managing a Profitable and Ethical Practice

For dentists, managing fees is a delicate balance between practice sustainability and patient accessibility.

Conducting an Annual Fee Schedule Analysis

A proactive practice will conduct a detailed annual analysis of its fee schedule. This involves:

-

Benchmarking: Comparing your fees to local and national data sources to ensure they are competitive and reflective of your practice’s value and costs.

-

Overhead Calculation: Precisely calculating your practice’s overhead percentage. If your overhead is 70% and you are charging a PPO-allowed fee of $1,000 for a crown, you are only keeping $300 before taxes. This math dictates the necessity of fee adjustments.

-

Analyzing PPO Contracts: Regularly reviewing the reimbursement rates of each PPO plan you participate in. Dropping a plan with chronically low reimbursement that has not increased in years may be a necessary business decision.

The Art of Communicating Value and Cost to Patients

Transparency builds trust. Use visual aids, intraoral camera images, and models to help patients understand their dental conditions and the necessity of proposed treatment. When discussing cost, use a financial consultation to clearly outline the investment, explain insurance benefits and limitations, and present all payment options upfront. This reduces “sticker shock” and improves case acceptance.

Implementing and Promoting In-Office Dental Membership Plans

As mentioned, these plans are a win-win. They provide predictable care for patients without insurance and create a stable, recurring revenue stream for the practice, reducing dependence on volatile insurance reimbursements.

Efficient Insurance Contract Management: To Participate or Not to Participate?

The decision to be a PPO provider is a major one. The benefit is a steady flow of new patients. The downside is accepting lower fees. Many successful practices are adopting a “hybrid” model: they participate in a few select PPOs with the best reimbursement and focus on attracting direct, fee-for-service patients through exceptional service and marketing, for whom they can charge their full UCR fee.

Leveraging Technology to Improve Operational Efficiency

Investing in technology should be viewed not just as a cost but as a means to improve profitability. Digital impressions with an intraoral scanner reduce lab resubmissions and chair time. Automated appointment reminders reduce no-shows. Efficient practice management software streamlines billing and claims submission. These efficiencies allow the practice to see more patients or reduce operational stress without necessarily raising fees dramatically.

7. The Future of Dental Pricing: Trends to Watch Beyond 2025

The forces shaping dental fees are dynamic. Several trends will influence pricing models in the years to come.

The Rise of Teledentistry and Its Impact on Fee Structures

Teledentistry, which saw accelerated adoption during the COVID-19 pandemic, allows for remote consultations and monitoring. This may lead to new, lower fee codes for “virtual visits” used for triage, post-op checks, and minor consultations, making certain aspects of care more accessible and affordable.

Value-Based Care vs. Fee-for-Service

The traditional fee-for-service model pays for activity (drilling and filling). The emerging value-based care model aims to pay for outcomes (keeping patients healthy). In such a system, a practice might be rewarded financially for reducing the incidence of cavities or gum disease in its patient population, potentially shifting the economic incentives in fundamental ways.

Consolidation and the Growth of Dental Service Organizations (DSOs)

The trend of solo practices being purchased by DSOs (like Heartland Dental, Pacific Dental Services) continues. DSOs can achieve economies of scale in purchasing and administrative functions, which can control costs. However, their fee schedules and PPO contract negotiations are centralized, which could lead to more standardized regional pricing.

Consumerism and Price Transparency Tools

Patients are becoming more empowered healthcare consumers. There is growing demand for upfront, transparent pricing. We can expect to see more practices and third-party tools that allow patients to easily compare costs for common procedures between different providers, increasing competition and pressure on practices to justify their fees with superior service and outcomes.

8. Conclusion

The 2025 Texas dental fee schedule is a multifaceted system, reflecting a balance between rising practice costs and the mechanisms of insurance reimbursement. For patients, proactive prevention, understanding insurance nuances, and exploring alternative payment plans are key to managing expenses. For providers, strategic fee analysis, clear communication, and efficient practice management are essential for sustainability. Ultimately, navigating this landscape successfully requires both parties to be informed, proactive partners in the pursuit of oral health.

9. Frequently Asked Questions (FAQs)

Q1: Is there an official, state-published dental fee schedule for Texas in 2025?

A: No. There is no single, official fee schedule for private dental practices. The only state-mandated fee schedule is for the Texas Medicaid program. Private practice fees are set by individual dentists, though they are heavily influenced by PPO insurance contracts.

Q2: Why did my dentist’s fees go up in 2025, but my insurance company’s allowed amount stayed the same?

A: This is a common occurrence. Your dentist raises their UCR fees to cover rising practice costs. However, your insurance company’s contract with your dentist may lock in the “allowed amount” for a year or more. If you are in-network, you are protected and only pay your portion of the allowed amount. The “discount” you see on your EOB simply becomes larger. If you are out-of-network, you would be responsible for the difference.

Q3: My dentist is recommending an all-porcelain crown, but my insurance only covers the cost of a PFM crown. Is this allowed?

A: Yes, this is a common practice called a “benefit downgrade.” The insurance company bases its payment on the cost of the least expensive professionally acceptable alternative (often a PFM crown). If you and your dentist choose a more expensive material (all-porcelain), you are responsible for the difference in cost between the two crown types, in addition to your standard co-insurance.

Q4: What is the single most important thing I can do to avoid a surprise dental bill?

A: Always obtain a pre-treatment estimate for any non-preventive procedure costing more than a few hundred dollars. This is a formal submission from your dentist to your insurance company that will return a detailed breakdown of what they will pay and what you will owe.

Q5: My dental insurance has a $1,500 annual maximum. Is that enough?

A: For basic preventive and minor restorative care, it may be sufficient. However, for a single major procedure like a crown or a bridge, it can be exhausted quickly. This $1,500 maximum has been largely unchanged for 30+ years, while dental costs have risen substantially, making it increasingly inadequate for comprehensive care.

10. Additional Resources

-

Texas State Board of Dental Examiners (TSBDE): Provides information on licensee verification, patient rights, and filing a complaint. https://www.tsbde.texas.gov/

-

American Dental Association (ADA): Offers a wealth of consumer information on oral health and dental procedures. https://www.mouthhealthy.org/

-

Texas Health and Human Services (Medicaid & CHIP): Information on eligibility and covered services for state programs. https://www.hhs.texas.gov/

-

National Association of Dental Plans (NADP): Provides consumer guides to understanding different types of dental plans. https://www.nadp.org/

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute financial, legal, or medical advice. Dental fee schedules are complex and subject to change. The data presented here is a synthesized model for illustrative purposes and should not be used for billing, claims, or financial planning. Always consult directly with your dental provider, insurance company, or a qualified professional for specific information regarding fees, coverage, and financial responsibilities. The author and publisher are not liable for any decisions made based on the content of this article.

Date: October 30, 2025

Author: The Health Policy Analysis Group