Finding the right dental insurance can sometimes feel like navigating a maze. You search for a plan, find one that fits your budget, and then you see the fine print: “Waiting period applies for major services.” For anyone dealing with an immediate dental issue—like a toothache that won’t quit or a broken filling—waiting six to twelve months for coverage is simply not an option.

This is where dental insurance no waiting period plans come into the picture. These policies are designed to offer benefits from day one, or very shortly after your policy becomes effective.

But is “no waiting period” insurance too good to be true? Are there catches? And how do you choose the right one?

This guide will walk you through everything you need to know. We’ll cover how these plans work, the different types available, the costs involved, and the specific scenarios where they make the most sense. By the end, you’ll have all the information you need to make a confident decision and get the dental care you need, when you need it.

Important Note: This article provides general information about dental insurance plans. Coverage details, waiting periods, and costs vary significantly by provider, your location, and the specific plan you choose. Always read the official policy documents carefully before enrolling.

What Does “No Waiting Period” Dental Insurance Actually Mean?

Let’s start with the basics. In the world of insurance, a waiting period (also known as an elimination period) is the time you must wait after purchasing a policy before you can use your benefits for certain types of care.

Most traditional dental insurance plans use a tiered waiting period system:

Preventive Care: Usually no waiting period (cleanings, exams, X-rays are covered immediately or after a very short time).

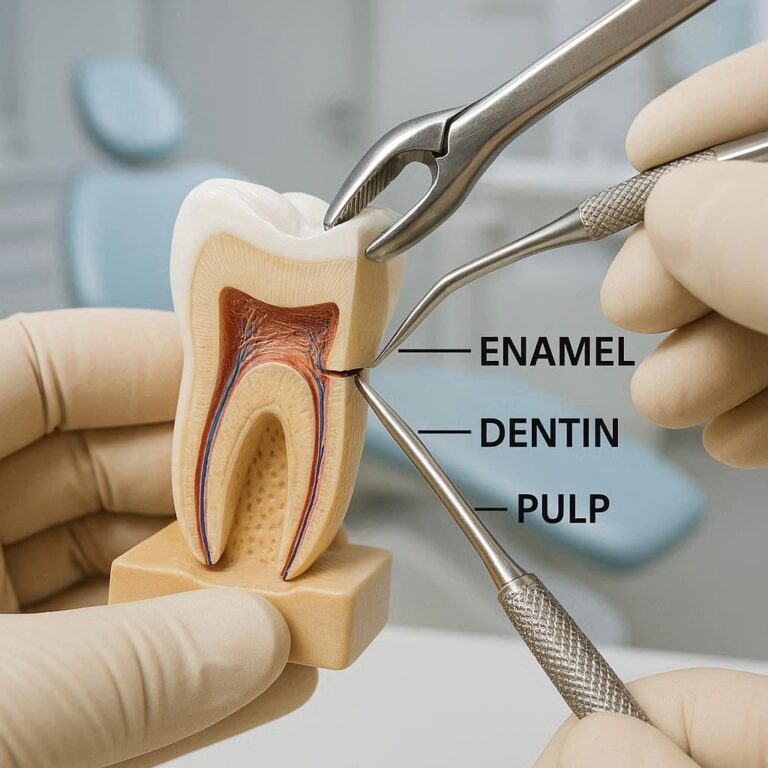

Basic Care: Often a 3 to 6-month wait (fillings, simple extractions, root canals).

Major Care: Often a 6 to 12-month wait (crowns, bridges, dentures, implants).

Therefore, dental insurance with no waiting period means that the standard time delays for basic and/or major services are reduced or eliminated entirely.

The Difference Between “No Waiting Period” and “Immediate Coverage”

It’s important to be precise with language here. While the main keyword is “dental insurance no waiting period,” plans usually fall into two categories:

True No Waiting Period (Immediate Coverage): You can schedule an appointment for a filling or even a crown the day your coverage starts, and the insurance will pay its share according to the plan’s benefits.

Reduced Waiting Period: Some plans might have a very short waiting period, such as 30 or 90 days, for major work. While technically a wait, this is significantly shorter than the industry standard of 12 months.

When shopping around, you’ll need to look closely at the “Schedule of Benefits” to see exactly when coverage for each type of procedure begins.

Why Do Standard Insurance Plans Have Waiting Periods?

To understand why “no waiting period” plans are special, it helps to know why waiting periods exist in the first place. Insurance companies are in the business of managing risk. Without waiting periods, someone could wake up with a toothache, buy a plan online, and get a $2,000 crown the next day for the cost of a single monthly premium. The insurance company would lose money on that transaction.

Waiting periods are a safeguard for the insurer. They prevent people from only signing up for insurance when they need expensive care and then dropping it immediately after. This concept is called “adverse selection,” and waiting periods are the primary tool to combat it.

“No waiting period” plans handle this risk differently. Instead of making you wait, they usually manage risk through higher premiums, lower annual maximums, or waiting periods for specific pre-existing conditions. We’ll explore these trade-offs in detail later.

Who Benefits Most from No Waiting Period Plans?

These plans aren’t for everyone, but they are a perfect fit for specific situations. Here’s who gets the most value:

Individuals with Immediate Dental Needs: This is the most common reason. If you have a tooth that’s been bothering you, a broken restoration, or you know you need a bridge, waiting a year is impractical and potentially painful. Immediate coverage allows you to address the problem right away.

New Employees During Open Enrollment: If you’re starting a new job and missed the initial enrollment window, or if you’re self-employed and buying an individual plan, a no-waiting-period policy ensures you’re covered for any issues that might arise shortly after you enroll.

Those Nearing Medicare Age: Many people retire and lose their employer-sponsored dental coverage. If you’re enrolling in a Medicare Advantage plan with dental benefits or a standalone dental plan, you want to ensure continuity of care without a service interruption.

People Who Prefer Predictability: Knowing you have full benefits from day one provides incredible peace of mind. You don’t have to worry about a dental emergency wiping out your savings because you’re still in a waiting period.

Individuals with a History of Dental Anxiety: If you’ve avoided the dentist for a while and are ready to go back, you might be facing several necessary procedures. A plan with no waiting periods allows you to tackle your treatment plan immediately, without delaying care further.

The Trade-Offs: What to Watch For

While the allure of immediate care is strong, it’s crucial to understand that “no waiting period” plans often balance this benefit in other areas. They aren’t necessarily “better” than traditional plans; they are simply structured differently. You should always look at the whole picture.

1. Higher Premiums

This is the most common trade-off. Because the insurance company is taking on more risk by letting you use benefits immediately, they often charge a higher monthly or annual premium compared to a similar plan with a standard 6 or 12-month waiting period.

2. Lower Annual Maximums

The annual maximum is the total amount the insurance company will pay for your care within a policy year (usually January to December). Typical plans have a maximum of $1,500, $2,000, or $2,500 per person. Some no-waiting-period plans might have a lower annual maximum, perhaps $1,000 or $1,500, to limit the insurer’s financial exposure in that first year.

This is a very important detail. Many dental insurance plans, including some with no waiting periods, will not cover a tooth that was already missing or extracted before your coverage started. They may also have limitations on teeth that had received root canal treatment or other major work prior to enrollment. Always check for a “Missing Tooth Clause” in the policy. It will explicitly state that the plan will not provide benefits for a prosthetic (like a bridge or implant) to replace a tooth that was missing before the effective date of coverage.

4. Scheduled vs. Indemnity Plans

Some very low-cost “no waiting period” options are actually discount plans or scheduled benefit plans, not true insurance. A discount plan gives you a membership card that entitles you to a discount (e.g., 20% off) at participating dentists. A scheduled benefit plan pays a fixed dollar amount for each procedure, which is often much less than what the dentist charges, leaving you to pay the difference. True insurance, known as indemnity or PPO plans, pays a percentage of the dentist’s contracted rate.

Comparison: No Waiting Period vs. Traditional Plan

To make the differences crystal clear, let’s look at a hypothetical comparison. Remember, these are examples for illustrative purposes.

As you can see, with Plan A you pay more per month for the convenience of immediate coverage, but you have a lower safety net ($1,500 max) for the year. Plan B is cheaper and offers a higher max, but you cannot use it for major work in the first year.

Types of Dental Plans with No Waiting Periods

When you start your search, you’ll encounter several types of products. It’s helpful to know the landscape.

1. Indemnity Plans (Traditional Insurance)

These are “fee-for-service” plans. You can usually go to any dentist you choose. You pay the bill upfront, and the insurance company reimburses you for a set percentage (e.g., 80% for a filling) after you submit a claim. Some indemnity plans offer no waiting periods, but they tend to be on the more expensive side.

2. PPO Plans (Preferred Provider Organization)

This is the most common type of dental insurance today. You choose a dentist from a network of providers who have agreed to discounted rates. This keeps your out-of-pocket costs lower. Many PPO plans are available with a no-waiting-period rider (an add-on) or as a specific plan variant. This is often the sweet spot for value and coverage.

3. Dental Discount Plans (Not Insurance)

As mentioned earlier, these are not insurance plans but membership programs. You pay a low monthly or annual fee and get access to a network of dentists who provide services at a reduced rate. There are no waiting periods because there are no insurance claims. You simply pay the discounted fee at the time of service. This can be a great option for someone who needs a lot of work done immediately and doesn’t want to deal with insurance claim forms, annual maximums, or deductibles. However, you are responsible for 100% of the discounted cost.

4. Employer-Sponsored Plans

If you have a job that offers dental benefits, check your summary plan description. Some employers negotiate with insurance carriers to waive or reduce waiting periods for their employees as a way to attract and retain talent. You might find that your company’s plan offers immediate coverage for all services, which is a significant perk.

How to Find and Evaluate the Best Plan for You

Finding the right plan requires a bit of detective work. Here’s a step-by-step guide to help you navigate the process.

Step 1: Assess Your Dental Needs

Before you even look at a plan, be honest about what you need.

Do you have an emergency? If you’re in pain, you need a plan with no waiting period for anything.

Do you have a treatment plan? If your dentist has already told you that you need three fillings and a crown, you have a clear idea of the costs involved. You can use this to calculate potential savings.

Are you generally healthy? If you just want coverage for cleanings and the “just in case” scenario, a traditional plan with waiting periods might be perfectly adequate and save you money on premiums.

Step 2: Focus on the “Evidence of Coverage” (EOC)

Don’t rely on the marketing brochure. The EOC, also called the “Schedule of Benefits” or “Certificate of Coverage,” is the legally binding document. When researching “dental insurance no waiting period,” look for these specific sections:

Waiting Periods Section: This will explicitly list the waiting time for each class of service (Type A, B, C, or Preventive, Basic, Major). It should clearly state “0 months” for the services you need.

Limitations and Exclusions: This section is just as important. Here you will find the “Missing Tooth Clause” and other limitations, such as waiting periods for procedures on the same tooth (e.g., no new crown on a tooth that had a filling in the last 12 months).

Frequency Limitations: Insurance plans limit how often they’ll pay for certain procedures. For example, they might only cover two cleanings per year or one crown per tooth every five years. Make sure these align with your needs.

Step 3: Check the Dentist Network

If you’re choosing a PPO plan, ensure your current dentist is in the network. You can usually find a “Find a Dentist” tool on the insurance company’s website. If you don’t have a dentist, you can use this tool to find a provider near you. Going out-of-network with a PPO usually means higher out-of-pocket costs.

Don’t just look at the monthly premium. Calculate your potential total first-year cost. Total First-Year Cost = (12 x Monthly Premium) + Deductible + Estimated Co-pays/Coinsurance

Then, compare that number to the cost of your expected dental work without insurance. This will give you a realistic picture of your savings.

Realistic Scenarios: What You Can Expect

To help ground this information, let’s walk through a couple of common scenarios.

Scenario A: The Emergency Fix

The Person: Sarah wakes up with a throbbing toothache. She hasn’t had dental insurance for two years. She calls an endodontist and learns a root canal and crown will cost roughly $2,500 out-of-pocket.

Her Goal: Get coverage to help pay for this immediate, necessary procedure.

The Reality: Sarah needs a plan with no waiting period for major care. She researches and finds a PPO plan with a $50/month premium, a $50 deductible, and a $1,500 annual max. She enrolls and makes an appointment for the following week. The total cost: Root canal and crown ($2,500). Insurance covers 50% after deductible: ($2,500 – $50) * 50% = $1,225. Sarah pays the rest ($1,275) plus her first month’s premium ($50) = $1,325 total out-of-pocket. She saved over $1,000 compared to having no insurance at all.

Scenario B: The Planned Treatment

The Person: Mark knows he needs a new bridge to replace a missing tooth. He has a treatment plan from his dentist estimating $3,500.

His Goal: Find a plan that will contribute the most toward this planned, major expense.

The Reality: Mark finds a “no waiting period” plan with a $60/month premium and a $1,500 annual max. He enrolls. He gets the bridge done. Insurance pays 50% of the $3,500 cost after his $50 deductible, hitting its $1,500 maximum payout. He pays the rest. Over the year, his total cost is premiums ($720) + deductible ($50) + balance of bill ($2,000) = $2,770. Without insurance, he’d pay $3,500. He saved $730, but still had a significant out-of-pocket expense because the total cost exceeded his plan’s annual maximum.

These scenarios show that while no-waiting-period insurance is incredibly helpful, it’s not a magic bullet. It’s a tool to reduce, not eliminate, your financial responsibility.

Frequently Asked Questions (FAQ)

Q: Is there really dental insurance with no waiting period for anything?

A: Yes, plans exist that offer immediate coverage for preventive, basic, and major services. However, they are less common than traditional plans and often come with higher premiums or a lower annual maximum. It is vital to read the fine print to ensure “major” services are truly covered from day one.

Q: Can I use no-waiting-period insurance immediately for pre-existing conditions?

A: This is tricky. While there may be no waiting period, the “Missing Tooth Clause” is a common exclusion. If a tooth was already extracted before your coverage started, the plan likely won’t pay for an implant or bridge to replace it. For a tooth that needs a filling or crown, it is often covered, provided it wasn’t missing.

Q: Are discount dental plans the same as no-waiting-period insurance?

A: No, they are fundamentally different. A discount plan is not insurance. You pay a fee to get access to reduced rates from participating dentists. There are no claims, no deductibles, and no annual maximums. You pay the dentist directly at the time of service. It’s a good alternative for immediate needs but works differently than traditional insurance.

Q: How much does dental insurance with no waiting period cost?

A: Costs vary widely based on your age, location, and the plan’s coverage levels. You can generally expect to pay a higher monthly premium—potentially 20% to 50% more—than for a comparable plan with standard waiting periods. Individual plans can range from $30 to $80 or more per month.

Q: Does Medicare cover dental with no waiting period?

A: Original Medicare (Parts A and B) does not cover routine dental care. Some Medicare Advantage (Part C) plans offer dental benefits. The specifics, including waiting periods, vary by plan. You would need to compare Medicare Advantage plans in your area to find one with immediate dental coverage.

Q: What is a typical annual maximum for these plans?

A: It is common for no-waiting-period plans to have a lower annual maximum in the first year to offset the risk for the insurer. You might see maximums around $1,000 to $1,500, whereas traditional plans might offer $1,500 to $2,000 from the start.

Additional Resources

Navigating the world of dental benefits can be complex. For unbiased, official information and tips on choosing a plan, we recommend visiting the National Association of Dental Plans (NADP) website. They are the non-profit trade association representing the dental benefits industry and offer excellent consumer resources.

[Visit the NADP Consumer Education Page] (You can link this to: https://www.nadp.org/Resources-for-Consumers)

Conclusion: Is a No Waiting Period Plan Right for You?

Dental insurance with no waiting period is a powerful solution for those who need care immediately and want to avoid costly delays. By understanding the trade-offs—typically higher premiums or lower annual maximums—you can make an informed choice that balances your need for instant coverage with your long-term budget. Whether you’re facing an unexpected toothache or planning a major dental procedure, these plans offer a valuable path to maintaining your oral health without the frustrating wait. Always compare the details, read the fine print, and choose a plan that fits your unique dental health journey.