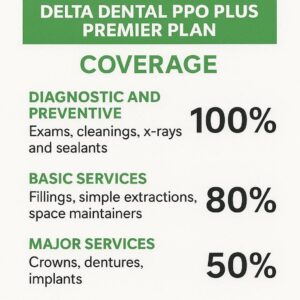

delta dental ppo plus premier plan coverage

- On

- InDENTAL COVERAGE

Choosing a dental insurance plan can often feel like navigating a maze. You know you need it, but understanding the difference between “in-network,” “out-of-network,” and those confusing plan names is a challenge for almost everyone.

If you have a plan that includes Delta Dental PPO and Premier networks, you are holding one of the most flexible dental insurance products on the market. But flexibility can sometimes lead to confusion. What exactly is the difference between a PPO provider and a Premier provider? Why does your dentist’s “tier” status affect your bill?

We are going to break this down in the simplest way possible. Think of this as your friendly guide to understanding exactly how your coverage works, how to save money, and how to avoid unexpected bills.

By the end of this article, you will feel confident walking into your next dental appointment, knowing exactly what your insurance will pay for and what you might owe.

Table of Contents

ToggleUnderstanding the Delta Dental Network Structure

Before we dive into the specifics of coverage, it is essential to understand how Delta Dental organizes its dentists. They do not treat all dentists equally, and that is actually good news for your wallet—if you know how it works.

Delta Dental operates on a tiered network system. While there are several types of networks across different states, the two you will encounter most frequently in a “PPO Plus Premier” plan are the PPO network and the Premier network.

What is the Delta Dental PPO Network?

The PPO network is the “preferred” network. These are dentists who have agreed to the deepest discounts in exchange for being part of Delta Dental’s most extensive referral list.

When you visit a dentist in the PPO network:

-

You get the highest level of benefits. The plan typically covers a larger percentage of the cost.

-

You pay the lowest out-of-pocket costs. Because the dentist has agreed to a contracted fee schedule, you are not responsible for the difference between the dentist’s usual fee and the allowed amount.

-

No balance billing. This is a crucial point. If the dentist charges $200 for a cleaning, but the PPO contracted rate is $120, the dentist agrees to accept $120. You only pay your portion (e.g., copay or coinsurance) of that $120.

What is the Delta Dental Premier Network?

The Premier network is Delta Dental’s original network. It is larger and includes dentists who have agreed to a discount, but not as steep of a discount as the PPO network.

When you visit a dentist in the Premier network:

-

You are still “in-network,” but at a different tier.

-

Benefits are slightly lower. Your insurance will still pay a portion, but the percentage of coverage might be reduced compared to a PPO dentist.

-

There is a higher cost structure. While the dentist agrees to accept a pre-negotiated fee (the “Premier fee schedule”), that fee schedule is generally higher than the PPO fee schedule.

-

You avoid balance billing (mostly). Similar to PPO, the dentist agrees not to charge you above the negotiated Premier fee for covered services.

The “Plus” in PPO Plus Premier

The “Plus” in the plan name indicates that you have access to both networks. You are not limited to just one. This gives you a massive pool of dentists to choose from.

Think of it this way: The PPO network is the “Gold Tier” and the Premier network is the “Silver Tier.” You have access to both, but the rewards (lower costs) are better if you choose the Gold Tier.

How Coverage Differs Between Tiers

Now that we know the difference between the two networks, let’s look at how the coverage actually works. Most Delta Dental PPO Plus Premier plans follow a classic 100/80/50 structure, but the percentages can shift depending on which tier you are in.

Preventive Care: The 100% Coverage

Preventive care is the foundation of dental health. Usually, these services are covered at 100% with no deductible if you visit a PPO dentist.

-

PPO Dentist: 100% covered. You pay $0 for cleanings, exams, and X-rays (subject to frequency limits).

-

Premier Dentist: Often still 100% covered, but sometimes the plan applies the deductible or covers it at a slightly lower percentage (like 90%). You need to check your specific Summary of Benefits.

Basic Procedures: Fillings and Extractions

This is where the tier difference becomes more noticeable. Basic procedures include fillings, simple extractions, and root canals (though root canals are sometimes categorized as major).

-

PPO Dentist: Typically covered at 80%. You pay the remaining 20% of the negotiated PPO fee.

-

Premier Dentist: Typically covered at 80% of the Premier fee. Since the Premier fee is higher than the PPO fee, your 20% co-insurance is calculated on a higher number. You pay more.

Major Procedures: Crowns, Bridges, and Dentures

Major procedures are the most expensive, and the coverage difference here can be substantial.

-

PPO Dentist: Typically covered at 50%. You are responsible for the other 50% of the PPO negotiated rate.

-

Premier Dentist: Typically covered at 50% of the Premier fee. Again, because the base fee is higher, your half of the bill is significantly higher.

A Quick Comparison Table

To visualize this, let’s say you need a crown. A PPO dentist charges $1,000 (the contracted rate). A Premier dentist charges $1,300 (the contracted rate).

| Service | Network Tier | Negotiated Fee | Plan Pays (50%) | You Pay (50%) |

|---|---|---|---|---|

| Crown | PPO | $1,000 | $500 | $500 |

| Crown | Premier | $1,300 | $650 | $650 |

| Difference | +$300 | +$150 | +$150 |

As you can see, for the exact same crown, staying in the PPO network saves you $150 out of pocket.

Key Factors That Influence Your Final Bill

Understanding the network is just the first step. Several other moving parts determine how much money you will actually hand over at the dental office.

The Calendar Year Maximum

Most Delta Dental plans have a calendar year maximum. This is the maximum amount the insurance company will pay for your care in a single year (usually January 1 to December 31).

-

Common range: $1,000 to $2,000 per person.

-

How it works: If your crown costs $1,000 and the plan pays $500, you have $500 less available for the rest of the year. If you need a second crown or a root canal, you might hit your maximum.

-

Note: If you use a Premier dentist, you will hit your annual maximum faster because the insurance pays higher fees for the same procedures.

The Deductible

Most plans have a deductible—an amount you must pay out of pocket before the insurance starts paying its share.

-

Typical amount: $50 per person, up to $150 per family.

-

Application: Usually, the deductible applies to Basic and Major services. Preventive care is often “deductible waived.”

Frequency Limitations

Dental insurance is designed to prevent over-utilization. Your plan will specify how often you can get certain services.

-

Cleanings: Usually two per year (every 6 months).

-

X-rays: Bitewing X-rays are typically covered once a year. Full mouth X-rays (FMX) are usually covered once every 3 to 5 years.

-

Crown replacements: Most plans will only pay for a crown replacement on the same tooth every 5 to 7 years unless there is a documented medical necessity (like decay under the old crown).

“Upgraded” Materials

This is a common point of confusion. If your dentist recommends a “premium” material—like a ceramic crown instead of a porcelain-fused-to-metal (PFM) crown—the insurance will usually only pay up to the cost of the standard material.

-

Example: The plan covers a PFM crown at $1,000. You want a zirconia crown that costs $1,500.

-

Result: The insurance pays its portion based on the $1,000 allowance. You are responsible for the remaining $500 difference in material cost plus your co-insurance.

In-Network vs. Out-of-Network: A Critical Distinction

It is vital to distinguish between Premier and Out-of-Network. Many people confuse Premier dentists as being “out-of-network” because the costs are higher. They are not.

-

PPO: Deepest discount. Highest coverage.

-

Premier: Moderate discount. Moderate coverage.

-

Out-of-Network: No discount. Lowest coverage.

If you visit a dentist who is in neither the PPO nor the Premier network, your plan changes drastically. You will likely have to pay the full bill upfront and submit a claim for reimbursement. The insurance will pay based on “Usual, Customary, and Reasonable” (UCR) fees, which are often much lower than what the dentist actually charges. You are then responsible for the balance—a process called balance billing.

Important Note: Always verify your dentist’s network status before your appointment. A dentist might be “in-network” for Delta Dental overall, but only for the Premier tier. Call the number on the back of your card or check the Delta Dental website to confirm they are “PPO” status.

How to Maximize Your Delta Dental PPO Plus Premier Plan

You have the plan; now let’s make it work for you. Here are practical strategies to get the most value out of your coverage.

1. Choose a PPO Dentist for Major Work

If you are getting a filling, crown, bridge, or implant, the savings between a PPO and Premier dentist can be hundreds of dollars. It is worth the effort to find a PPO provider for expensive procedures.

2. Understand Your “Year” and “Maximum”

If your plan resets on January 1st, and you have a $1,500 maximum, try to schedule major work in the same calendar year. If you need two crowns, doing them in the same year means you might pay less overall than splitting them across two years (because you pay the deductible twice).

3. Use Preventive Care Diligently

Do not skip your cleanings. Since they are covered at 100% (usually), they are your best tool to avoid costly major procedures later. A $200 filling is cheaper than a $1,500 crown.

4. Ask for a Pre-Treatment Estimate

For any procedure costing over $300, ask your dentist to submit a pre-treatment estimate (predetermination) to Delta Dental. This is not a claim; it is a prediction of what insurance will pay. It is free and gives you a written document outlining your out-of-pocket costs before the work begins.

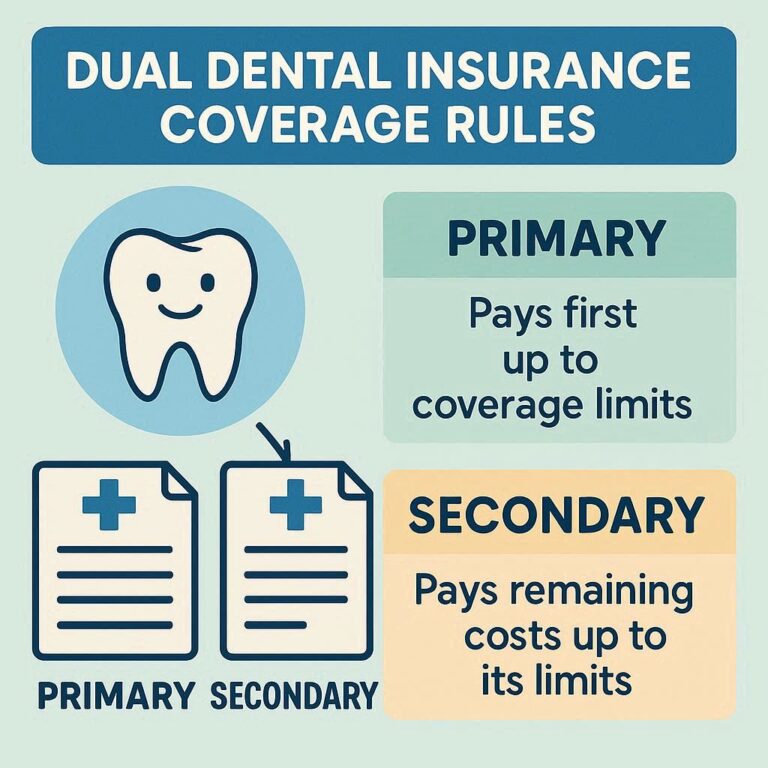

5. Coordinate Benefits if You Have Two Plans

If you are covered by your employer’s plan and your spouse’s plan, you can “coordinate benefits.” Usually, the primary plan pays first, and the secondary plan may cover some of the remaining balance. This can significantly reduce your out-of-pocket costs for major procedures.

Common Questions About Delta Dental PPO Plus Premier

Let’s address some of the most frequent questions people have when trying to use their plan.

Does my plan cover orthodontics (braces)?

It depends entirely on your specific employer group. Some PPO Plus Premier plans include orthodontic coverage for children (or adults), while others do not. If orthodontics is covered, there is usually a separate lifetime maximum (e.g., $1,500 to $2,500) that is separate from your annual maximum. Orthodontic coverage often applies to both PPO and Premier orthodontists, but the discounts are deeper with PPO orthodontists.

What about implants?

Dental implants are typically covered, but they are treated as a “major” service. The coverage usually applies to the implant fixture (the screw) and the abutment/crown. However, the plan often separates the benefits. You might have a $1,500 annual maximum, and an implant can cost $3,000 to $5,000. In this case, the insurance pays up to the maximum, and you pay the rest. A PPO dentist will have a lower contracted rate for the implant, saving you money.

Do I need a referral to see a specialist?

Generally, with a PPO plan, you do not need a referral to see a specialist like an endodontist (root canal specialist) or oral surgeon. However, if you want the highest level of coverage, you should ensure that specialist is in the PPO network, not just Premier.

Why did my dentist say I owe more than the insurance said?

This happens for two common reasons:

-

UCR vs. Billed Amount: If you went out-of-network, the insurance paid what they deem “reasonable,” but the dentist charges more. You owe the difference.

-

Non-Covered Services: Some services, like nitrous oxide (laughing gas) or certain types of sedation, may not be covered at all. You are responsible for 100% of those costs.

Regional Variations: Why Your Plan Might Look Different

It is important to note that Delta Dental is a federation of independent companies. While the “PPO Plus Premier” branding is common, the specific fee schedules and coverage details can vary significantly by state.

For example:

-

Delta Dental of California: Often uses a “PPO” and “Premier” structure with very clear tier differences.

-

Delta Dental of Michigan/Ohio/Indiana: May have slightly different network names or fee schedules.

-

Delta Dental of New York: Might have different frequency limitations.

Always refer to your specific “Schedule of Benefits” (the document you received when you enrolled). This document is the legal description of your plan. If you cannot find it, you can usually log into your Delta Dental member portal to download a copy.

The Future of Your Dental Benefits

Understanding your “delta dental ppo plus premier plan coverage” is not just about saving money today; it is about strategic health planning.

Many people make the mistake of choosing dentists based solely on proximity or familiarity, without checking network status. If you have been seeing a “Premier” dentist for years and are happy with them, that is great. However, if you are facing a significant treatment plan—such as a bridge, multiple crowns, or full-mouth rehabilitation—it is worth asking your dentist if they are also in the PPO network, or if they can refer you to a PPO specialist.

If your current dentist is not in the PPO network, do not be afraid to ask for a “network status change.” Sometimes, dentists choose to be in the Premier network only, but they may be willing to accept the PPO fee schedule for you if you are a long-term patient with a large treatment plan. It never hurts to ask.

List: Steps to Take Before Your Next Appointment

To ensure you are maximizing your coverage, follow this checklist:

-

Verify Network Status: Log in to your Delta Dental account and confirm your dentist is listed as “PPO” (not just “Premier”).

-

Confirm Your Maximum: Check how much of your annual maximum you have left. If you have $1,500 left and it is October, you might want to schedule major work before December 31st.

-

Check Deductible Status: If you haven’t had any work done this year, you might need to pay your deductible. Factor that into your budget.

-

Ask for a Pre-Treatment Estimate: For anything beyond a filling, get this in writing.

-

Review Frequency Limits: Ensure you are not scheduling a cleaning if you had one three months ago (unless medically necessary).

Conclusion

Navigating dental insurance does not have to be a headache. The Delta Dental PPO Plus Premier plan offers one of the most flexible networks available, giving you access to a vast number of dentists. The key to saving money lies in understanding the difference between the PPO and Premier tiers.

To put it simply: Stay in the PPO network to minimize your out-of-pocket costs. Use the Premier network for convenience or if your preferred dentist is only available there, but be prepared for slightly higher costs.

By verifying network status, understanding your annual maximum, and utilizing preventive care, you can keep your smile healthy without breaking the bank. Take control of your benefits today—your future self (and your wallet) will thank you.

Frequently Asked Questions (FAQ)

Q: Is Delta Dental Premier considered in-network?

A: Yes, Premier dentists are considered in-network, but they are a different tier than PPO dentists. You will receive coverage, but your out-of-pocket costs will generally be higher than if you visited a PPO dentist.

Q: Can I switch from a Premier dentist to a PPO dentist mid-treatment?

A: Yes, you can generally switch dentists at any time. However, if you have started a procedure like a crown or bridge, the new dentist may need to start over, potentially incurring additional costs. It is best to complete major work with one dentist if possible.

Q: Does my plan cover cosmetic dentistry (like veneers or teeth whitening)?

A: Generally, no. Delta Dental PPO Plus Premier plans are designed for medically necessary dental care. Cosmetic procedures aimed at improving appearance rather than function are typically not covered.

Q: What happens if I go to an out-of-network dentist?

A: You will likely pay more. The dentist does not have to accept the insurance company’s fee schedule, meaning you may be responsible for the difference between what the insurance pays and the dentist’s full fee. You will also usually have to pay upfront and wait for reimbursement.

Q: How do I find a Delta Dental PPO dentist near me?

A: You can use the “Find a Dentist” tool on the Delta Dental website. Be sure to filter the search to show only “PPO” or “PPO Plus Premier” network dentists, rather than selecting all networks.

Additional Resource

For the most accurate and up-to-date information regarding your specific plan, including finding in-network providers and downloading your personalized Schedule of Benefits, visit the official Delta Dental member portal.

dentalecostsmile

Newsletter Updates

Enter your email address below and subscribe to our newsletter