If you are a UPMC for Life member—or if you are considering enrolling—you probably have questions about your dental benefits. Dental health is a critical part of your overall wellness, and understanding your coverage can save you from unexpected bills and help you keep your smile healthy.

UPMC for Life offers a variety of Medicare Advantage plans. While these plans are primarily known for hospital and medical coverage, most of them include dental benefits. However, not all dental coverage is created equal. Depending on whether you have an HMO (Health Maintenance Organization) or PPO (Preferred Provider Organization) plan, your benefits, costs, and the network of dentists available to you will look very different.

This guide is designed to be your go-to resource. We will walk you through everything you need to know, from preventive care like cleanings and X-rays to major procedures like crowns and dentures. We will also look at how to read your plan documents and how to maximize your benefits so you aren’t leaving money on the table.

Before we dive into specific numbers and procedures, it is important to understand how UPMC for Life structures its dental coverage. UPMC for Life is the Medicare Advantage division of UPMC Health Plan. They serve a large population in Pennsylvania, particularly in the western part of the state, though they have a growing presence elsewhere.

Medicare Advantage plans (Part C) are required to offer at least the same coverage as Original Medicare (Parts A and B). However, Original Medicare does not cover routine dental care. Because of this, Medicare Advantage plans like UPMC for Life often add dental benefits as “supplemental benefits” to attract members.

The Two Main Types of Plans: HMO vs. PPO

When looking at your UPMC for Life dental coverage, the first thing you need to identify is whether your plan is an HMO or a PPO. The difference significantly impacts your experience.

UPMC for Life HMO (HMO-POS) Plans

These plans generally require you to choose a primary care provider (PCP). For dental coverage, you are usually restricted to a specific dental network. If you go to a dentist outside of this network, you will likely pay the full cost out-of-pocket with no coverage from the plan. HMO plans typically have lower monthly premiums and predictable copays for services.

UPMC for Life PPO Plans

PPO plans offer more flexibility. You do not need a referral to see a specialist, and you have the freedom to see dentists both in and out of the network. While staying in-network saves you the most money, you still get partial coverage if you choose an out-of-network provider. PPO plans usually come with a higher monthly premium but offer a broader choice of dentists.

Important Note: Not every UPMC for Life plan includes dental coverage. Some plans are “D-SNPs” (Dual Special Needs Plans) for those who qualify for both Medicare and Medicaid, which may have different dental benefits. Always verify your specific Summary of Benefits to confirm what is included.

UPMC for Life Dental Coverage

What Does UPMC for Life Dental Coverage Typically Include?

Most UPMC for Life Medicare Advantage plans categorize dental services into three tiers: preventive, basic, and major. Understanding these tiers will help you budget for your dental care throughout the year.

Preventive Dental Care

Preventive care is the foundation of dental health. These services are designed to catch problems early and maintain your oral hygiene. In most UPMC for Life plans, preventive care is covered at 100% or with a very low copay.

Routine Exams (usually 2 per year): Your dentist will check for cavities, gum disease, and oral cancer.

Cleanings (usually 2 per year): Professional cleaning to remove plaque and tartar.

Bitewing X-rays (usually 1 set per year): X-rays that help detect decay between teeth.

Panoramic X-rays (usually 1 every 3-5 years): A full view of your jaw and teeth.

Fluoride Treatments: Often covered for members at high risk of decay.

Basic services address common dental issues that require treatment. Coverage for these services usually ranges from 50% to 80% after you meet your deductible.

Fillings: Repairing cavities in teeth.

Simple Extractions: Removing teeth that are visible above the gum line.

Root Canals (Anterior/Bicuspid): Treating infection in the front or middle teeth.

Periodontal Maintenance: Deep cleanings for patients with gum disease.

Major Dental Care

Major services are the most expensive procedures. Coverage here is usually lower, often around 50% , and there may be a waiting period (typically 6 to 12 months) for new members.

Crowns: Caps placed over damaged teeth.

Bridges: Replacing missing teeth by anchoring to adjacent teeth.

Dentures: Full or partial sets of replacement teeth.

One of the most common questions regarding dental coverage is, “How much will this cost me?” With UPMC for Life, the cost structure can be a bit complex because it often involves a combination of a plan premium, a dental deductible, and service-specific copays.

Monthly Premiums

Many UPMC for Life plans offer a $0 monthly premium for the medical portion of the plan. However, if the plan includes dental benefits, the premium might be slightly higher than a plan without dental, or the dental benefits are built into the $0 premium structure.

For plans with enhanced dental benefits (higher annual maximums), you might see a premium ranging from $20 to $60 per month.

Annual Deductible

This is the amount you must pay out-of-pocket before the plan starts paying for services (excluding preventive care, which is often covered before the deductible).

HMO Plans: Often have no dental deductible, or a very low one (around $50).

PPO Plans: Typically have a dental deductible ranging from $50 to $150 per year.

Copays and Coinsurance

Copay: A fixed amount you pay for a service (e.g., $10 for a cleaning, $50 for a filling).

Coinsurance: A percentage of the cost you pay (e.g., you pay 20%, the plan pays 80%).

Annual Maximum

This is the most important number to look for. The annual maximum is the cap on what the insurance will pay for your dental care in a calendar year.

Basic Coverage: Some plans have a low annual maximum, around $500 to $1,000 .

Enhanced Coverage: Many UPMC for Life plans now offer enhanced benefits with an annual maximum of $1,500 to $3,000 .

No Maximum: Some premium plans (often D-SNPs) may have no annual maximum for medically necessary dental work.

Important Note: If you need major work, like multiple crowns or a bridge, you may hit your annual maximum quickly. It is wise to discuss treatment plans with your dentist to prioritize what is covered in the current year versus the next.

How to Find a UPMC for Life Dentist

Finding a dentist who accepts your insurance is crucial. If you have an HMO plan, this step is non-negotiable; you must stay in-network. If you have a PPO, you have flexibility, but staying in-network will save you money.

Step 1: Use the UPMC Health Plan Provider Directory

The most reliable resource is the official UPMC Health Plan website. They maintain a real-time directory of in-network dentists.

Go to the UPMC Health Plan website.

Navigate to “Find a Provider.”

Select your specific plan type (UPMC for Life HMO or PPO).

Filter by “Dentistry.”

Look for dentists who are “accepting new patients.”

Step 2: Verify Before You Book

Even if a dentist is listed online, it is a good habit to call the office and confirm three things:

“Do you accept UPMC for Life [HMO/PPO]?”

“Are you currently accepting new patients?”

“Do you accept my specific plan ID number?” (Some offices may have limits on which sub-plans they accept.)

Step 3: Check for Specialists

If you need an orthodontist, oral surgeon, or periodontist, ensure they are also in-network. In HMO plans, you may need a referral from your primary care dentist to see a specialist.

Tips to Maximize Your UPMC for Life Dental Benefits

Dental insurance is often described as “use it or lose it.” Because benefits reset every calendar year, it is financially wise to make the most of your coverage.

1. Schedule Your Two Cleanings

Preventive visits are usually free or low-cost. By attending your two recommended cleanings and exams per year, you not only maintain your oral health but also establish a relationship with your dentist. If an issue arises, you are more likely to catch it early when treatment is cheaper.

2. Understand Your “Plan Year”

Most UPMC for Life dental plans operate on a calendar year (January 1 – December 31). Your deductible and annual maximum reset on January 1st. If you have been putting off a crown, and you have remaining benefits in November, schedule it immediately. If you wait until January, you will have to meet a new deductible and start fresh on your annual maximum.

3. Ask for a Pre-Treatment Estimate

Before undergoing expensive procedures like crowns, bridges, or implants, ask your dentist to submit a pre-treatment estimate to UPMC. This is not a guarantee of coverage, but it tells you exactly how much the plan will pay and how much you will owe. This prevents surprise bills.

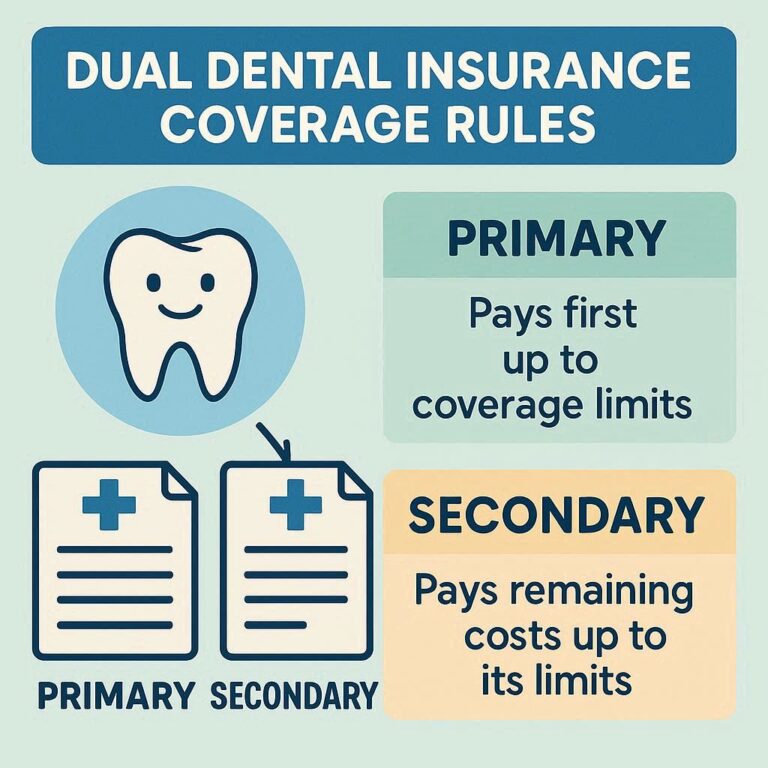

4. Combine Benefits (If Applicable)

If you have a spouse with separate dental insurance (perhaps through an employer), you may be able to coordinate benefits. This means one plan pays its portion, and the other covers some of the remainder. This is called “coordination of benefits.” UPMC for Life typically acts as the primary payer if it is your primary insurance.

Common Questions About UPMC for Life Dental

Are Dental Implants Covered?

This is a frequent question, and the answer is nuanced. Dental implants are considered a major service. While some older UPMC for Life plans do not cover implants at all, many newer plans (especially PPOs with enhanced benefits) offer partial coverage.

Typically, if implants are covered, they fall under the “major services” category with a 50% coinsurance. However, there is often a separate limit for implants (e.g., one implant per year) or a requirement that the implant is medically necessary (to restore chewing function) rather than cosmetic.

Do I Need a Referral to See an Orthodontist?

It depends on your plan type.

HMO: Usually, yes. You need to see your primary care dentist first, who will issue a referral if orthodontic work is medically necessary (usually only for children or severe jaw issues).

PPO: Usually, no. You can typically go directly to an orthodontist, though coverage for adult orthodontics is rare in Medicare Advantage plans.

What Happens if I Move Out of State?

UPMC for Life primarily operates in Pennsylvania and a few surrounding areas. If you move outside of the service area, you generally cannot keep your UPMC for Life plan. You would need to enroll in a new Medicare Advantage plan in your new state or switch to Original Medicare with a standalone Part D plan. Dental coverage would end when your membership ends.

Can I Keep My Current Dentist?

If your current dentist is in the UPMC for Life network, yes. If not, you have a few options:

If you have a PPO, you can stay with your dentist but pay more (out-of-network costs).

If you have an HMO, you would likely need to switch to an in-network dentist to have coverage.

Realistic Scenarios: How Coverage Works in Practice

To make this more tangible, let’s look at two hypothetical members and how their UPMC for Life dental coverage might apply.

Scenario 1: Sarah, Preventive Care Focus

Sarah has a UPMC for Life HMO plan with a $0 premium and no dental deductible. Her plan covers two cleanings and exams per year at 100%.

The Visit: Sarah goes for her cleaning. She also gets bitewing X-rays.

The Cost: Sarah pays a $0 copay. The plan pays the contracted rate ($120) to the dentist.

Outcome: Sarah maintains her dental health with no out-of-pocket cost.

Scenario 2: Mark, Major Dental Work

Mark has a UPMC for Life PPO plan. He pays a $40 monthly premium. His plan has a $50 dental deductible and a $1,500 annual maximum. He needs a crown (major service) which costs $1,200.

Step 1: Mark must meet his $50 deductible first (if he hasn’t had any other dental work that year).

Step 2: After the deductible, the plan pays 50% of the cost for the crown ($600).

Step 3: Mark pays the remaining 50% ($600).

Total Out-of-Pocket for Mark: $50 (deductible) + $600 = $650.

Annual Maximum Remaining: $1,500 – $600 = $900 left for the rest of the year.

If Mark needed a second crown in the same year, the plan would cover another $600, leaving him with only $300 left in his annual maximum for the year.

Verify Your Plan Details: Plan benefits change annually. The coverage you had in 2024 may differ from your 2025 benefits. Always read the “Annual Notice of Changes” (ANOC) letter sent by UPMC each fall.

D-SNP Plans Offer More: If you qualify for a Dual Special Needs Plan (D-SNP) because you have both Medicare and Medicaid, your dental benefits are often significantly more generous. These plans frequently offer no annual maximum for medically necessary dental services, including dentures and extractions.

Emergency Dental Care: Most UPMC for Life plans cover emergency dental care (e.g., pain relief, trauma) even if it is not from a regular dentist. However, follow-up care (like a crown after a root canal) usually falls under your standard benefits.

Waiting Periods: If you are new to the plan, some major services may have a waiting period. This means you must be enrolled for 6 or 12 months before the plan will pay for crowns or dentures. This is to prevent people from joining the plan, getting expensive work done, and then leaving.

How UPMC for Life Compares to Standalone Dental Plans

Sometimes, members wonder if they should stick with the dental benefits included in their Medicare Advantage plan or purchase a separate standalone dental plan. Here is a quick comparison.

Feature

UPMC for Life Dental (MA Plan)

Standalone Dental Plan

Cost

Often included in $0 premium plans.

Requires a separate monthly premium ($20-$50).

Annual Maximum

Usually $500 – $3,000.

Can be higher ($1,000 – $2,500), but some have no max.

Major Services

Coverage varies; often 50% after deductible.

Often 50% after deductible; may have higher limits.

Convenience

One bill, one insurance card for medical/dental.

Separate card, separate billing.

Orthodontics

Rarely covered for adults.

Sometimes covered for children; rarely for adults.

Which is better?

If you only need preventive care and have a low risk of major dental issues, the UPMC for Life dental coverage is usually sufficient and cost-effective. If you know you need multiple crowns, bridges, or have a history of complex dental needs, you might consider a supplemental standalone plan to increase your total coverage, provided you are willing to pay a second premium.

Navigating Your Plan Documents

Insurance documents can feel overwhelming. To understand your dental coverage, you need to look at two specific documents.

The Summary of Benefits

This is a short (usually 8-10 page) document that highlights what the plan covers. Look for the section titled “Dental Services.” Here you will find the copays, deductibles, and annual maximums in plain language.

The Evidence of Coverage (EOC)

This is the comprehensive contract (over 100 pages). If you want the exact legal details of your coverage, including definitions of “medically necessary” or how appeals work, this is the document to read. You can usually find it in your online UPMC account.

Additional Resource: Maximizing Your Oral Health

While insurance covers the cost, your oral health depends on your daily habits. To get the most out of your UPMC for Life dental coverage, pair it with good hygiene.

Brush twice daily with fluoride toothpaste.

Floss daily to prevent gum disease. Gum disease is the leading cause of tooth loss in adults.

Don’t skip your annual exam just because your teeth feel fine. Oral cancer screenings are a vital part of preventive visits.

For more detailed information on maintaining oral health as you age, the National Institute of Dental and Craniofacial Research offers excellent free resources on senior dental care.

Conclusion

UPMC for Life dental coverage is a valuable benefit that goes far beyond what Original Medicare offers. Whether you are enrolled in an HMO plan with low copays or a PPO plan with greater flexibility, understanding the structure of your benefits—including preventive care coverage, the annual maximum, and the distinction between basic and major services—is the key to using them effectively.

By taking the time to find an in-network dentist, scheduling your preventive visits, and planning for major procedures with your annual maximum in mind, you can protect your smile without breaking the bank. Remember, dental health is deeply connected to overall health, affecting everything from nutrition to heart health. Use your benefits wisely, stay informed about your plan changes each year, and never hesitate to ask your dentist’s office to verify your coverage before a procedure.

Frequently Asked Questions (FAQ)

1. Does UPMC for Life cover dental implants?

It depends on your specific plan. Many newer UPMC for Life PPO and D-SNP plans offer partial coverage for implants under “major services” (typically 50% coinsurance). However, some older HMO plans may not cover implants at all. Check your Evidence of Coverage or call customer service to verify.

2. How many cleanings does UPMC for Life cover per year?

Most UPMC for Life plans cover two routine cleanings and exams per calendar year. Some plans may allow three if deemed medically necessary for gum disease management.

3. Can I see any dentist with UPMC for Life?

If you have a PPO plan, you can see any dentist, but you will pay less if you stay in-network. If you have an HMO plan, you must see a dentist within the network to receive coverage; otherwise, you will pay the full cost.

4. What is the annual maximum for dental coverage?

The annual maximum varies by plan. It can range from $500 for basic plans to $3,000 or more for enhanced benefit plans. Some D-SNP plans have no annual maximum for medically necessary services.

5. Is there a waiting period for major dental work?

Sometimes, yes. If you are a new member, your plan may impose a 6 to 12-month waiting period before covering major services like crowns, bridges, or dentures. Preventive and basic services typically do not have waiting periods.