What Is Basic Dental Care Coverage? A Complete Guide to Understanding Your Plan

Dental insurance can feel like reading a document written in a secret code. You see words like “deductibles,” “coinsurance,” and “annual maximums.” Your eyes might glaze over. But here is the good news: understanding the foundation of your policy is easier than you think.

At the heart of almost every dental plan lies something called basic dental care coverage. This is the engine that drives your routine visits and keeps your mouth healthy without breaking the bank.

So, what is basic dental care coverage exactly?

In simple terms, it is the part of your dental insurance policy that pays for essential services to prevent, diagnose, and treat common dental problems. Think of it as the middle ground. It is not major surgery like crowns or bridges. But it is also more than just a simple cleaning. Basic coverage includes fillings, extractions, root canals (sometimes), and periodontal treatments.

This article will walk you through everything you need to know. We will explore what is included, what is left out, how much you will pay, and how to pick the right plan for your family. Let us dive in.

Why Understanding Basic Dental Coverage Matters

Many people sign up for dental insurance through their employer or a private marketplace. They pay the monthly premium and assume everything is covered. Then, the bill arrives after a simple filling. Confusion sets in.

Understanding your basic coverage saves you money. It also reduces stress. When you know what your plan pays for, you can plan your treatments. You can ask your dentist the right questions. You can avoid surprise costs.

According to the National Association of Dental Plans, over 77% of Americans have some form of dental coverage. Yet, most do not know the difference between Class I, Class II, and Class III services. That lack of knowledge costs consumers hundreds of dollars every year.

Important Note: No two dental plans are identical. Always read your specific policy’s Summary of Benefits. This article provides general guidelines. Your plan may have unique exceptions or limits.

The Three Tiers of Dental Coverage

To truly understand basic care, you need to see the big picture. Most dental insurance providers divide services into three main categories or “classes.”

Preventive Care (Class I)

This is the foundation. Preventive care keeps problems from starting. Most plans cover these services at 100%. That means you pay nothing out-of-pocket if you stay in-network.

Preventive services usually include:

-

Routine oral exams (twice per year)

-

Professional cleanings (prophylaxis)

-

Bitewing X-rays (once or twice per year)

-

Fluoride treatments (for children)

-

Sealants (for children’s molars)

Basic Care (Class II)

This is our main topic. Basic care treats common problems that have already started. Plans typically cover 70% to 80% of the cost. You pay the remaining 20% to 30% as coinsurance.

Major Care (Class III)

This is for serious dental work. Major care includes crowns, bridges, dentures, and implants. Plans usually cover only 50% of these costs. You pay the other half.

Here is a simple table to visualize the differences.

| Service Type | Common Procedures | Typical Plan Coverage | Your Responsibility |

|---|---|---|---|

| Preventive (Class I) | Cleanings, exams, X-rays | 100% | $0 (in-network) |

| Basic (Class II) | Fillings, extractions, root canals | 70% – 80% | 20% – 30% coinsurance |

| Major (Class III) | Crowns, bridges, dentures | 50% | 50% coinsurance |

What Specific Procedures Fall Under Basic Dental Care Coverage?

Let us get specific. When you visit a dentist and they say you need a filling or a tooth pulled, that is basic care. Here is a detailed breakdown of the most common procedures covered.

Restorative Fillings

When a cavity forms, your dentist removes the decay and fills the hole. This is the most common basic procedure. Fillings restore the tooth’s shape and function.

Most basic plans cover:

-

Amalgam (silver) fillings

-

Composite (tooth-colored) fillings on front teeth

-

Some plans cover composite on back teeth, but you may pay extra

What you might pay: If your plan covers 80% of a $200 filling, you pay $40.

Simple Extractions

Sometimes a tooth cannot be saved. A simple extraction removes a tooth that is visible above the gum line. This is different from a surgical extraction, which involves cutting into the gum.

Basic coverage almost always includes simple extractions. Surgical extractions (like wisdom teeth removal) may fall under major care or require a separate rider.

Root Canal Therapy (Anterior and Premolar)

A root canal saves an infected tooth by removing the nerve and pulp. However, coverage depends on which tooth is involved.

-

Root canal on a front tooth (incisor or canine): Usually covered as basic care.

-

Root canal on a premolar: Often covered as basic care.

-

Root canal on a molar: Many plans classify this as major care. Molars are harder to treat, so the cost is higher.

Always check your plan. Some policies cover all root canals at the basic level. Others split them.

Periodontal (Gum) Treatment

Gum disease is common. Basic coverage often includes non-surgical treatments for early to moderate gum disease.

Covered services may include:

-

Scaling and root planing (deep cleaning)

-

Periodontal maintenance (follow-up cleanings after active treatment)

-

Topical antibiotic placement

Emergency Palliative Treatment

If you crack a tooth on a Friday night and need emergency care to stop the pain, basic coverage applies. Palliative treatment relieves discomfort without fixing the underlying problem. It buys you time.

What Is Usually NOT Covered as Basic Care?

Knowing what is excluded is just as important as knowing what is included. Here are common procedures that fall outside basic coverage.

-

Cosmetic dentistry: Teeth whitening, veneers, and bonding for cosmetic reasons.

-

Orthodontics: Braces or clear aligners for adults or children (unless you have a separate orthodontic rider).

-

Major restorations: Crowns, inlays, onlays, and bridges.

-

Dentures: Partial or complete dentures.

-

Dental implants: The implant post, abutment, and crown.

-

Surgical extractions: Impacted wisdom teeth or teeth requiring incisions.

-

General anesthesia or sedation: Unless medically necessary for a covered procedure.

Note: Some plans offer “enhanced” or “plus” basic coverage. These might include more root canals or even simple crowns. Read your policy carefully.

How Cost Sharing Works for Basic Dental Care

Dental insurance does not work like medical insurance. You will encounter several cost-sharing mechanisms. Understanding these will help you budget.

Deductible

This is the amount you pay before your insurance starts paying. For basic care, you must meet your deductible first.

Example: Your plan has a $50 annual deductible. You get a filling that costs $150. You pay the first $50. Then insurance covers 80% of the remaining $100. You pay $20 more. Total out-of-pocket: $70.

Most dental deductibles range from $50 to $100 per person per year. Some plans waive the deductible for preventive care.

Coinsurance

This is the percentage you pay after meeting your deductible. For basic care, coinsurance is typically 20% to 30%.

If your coinsurance is 20%, you pay twenty cents for every dollar of covered services. Insurance pays eighty cents.

Annual Maximum

This is the most your insurance will pay in a single year. Most annual maximums range from $1,000 to $2,000 per person.

Here is the catch: The annual maximum applies to basic and major care combined. Preventive care usually does not count against the maximum.

Example: Your annual maximum is $1,500. You get a root canal ($1,000) and three fillings ($600 total). Insurance pays $1,500. You pay the remaining $100 plus your coinsurance amounts.

Waiting Periods

Many plans impose waiting periods for basic care. A waiting period is the time you must be enrolled before coverage kicks in.

-

Preventive care: Usually no waiting period.

-

Basic care: 3 to 6 months waiting period is common.

-

Major care: 6 to 12 months waiting period.

If you need a filling during your first month, you might pay full price. Always ask about waiting periods before enrolling.

A Real-World Example: Sarah’s Basic Dental Visit

Let us walk through a realistic scenario. Sarah has a dental plan with the following terms:

-

Deductible: $50

-

Basic coinsurance: 20% (plan pays 80%)

-

Annual maximum: $1,500

-

No waiting period (she has been enrolled for over a year)

Sarah visits her dentist for a regular checkup. The dentist finds two small cavities.

Step one – Preventive visit:

-

Exam: $60 (covered at 100% – Sarah pays $0)

-

Cleaning: $90 (covered at 100% – Sarah pays $0)

-

Bitewing X-rays: $50 (covered at 100% – Sarah pays $0)

Step two – Basic treatment:

-

Two composite fillings: $300 total

Sarah has not met her deductible yet this year. She pays the first $50. The remaining balance is $250. Insurance pays 80% of $250, which is $200. Sarah pays the remaining 20%, which is $50.

Total out-of-pocket for Sarah:

-

Deductible: $50

-

Coinsurance on fillings: $50

-

Grand total: $100

Without insurance, Sarah would have paid $500 for the entire visit. Her basic coverage saved her $400.

Basic Dental Coverage vs. Discount Dental Plans

Many people confuse traditional dental insurance with discount dental plans. They are not the same thing.

Traditional Dental Insurance (What We Are Discussing)

-

You pay a monthly premium.

-

You meet a deductible.

-

Insurance pays a percentage (80% for basic care).

-

You have an annual maximum.

-

Networks apply.

Discount Dental Plans

-

You pay an annual membership fee.

-

No deductibles or annual maximums.

-

No coinsurance percentages.

-

You receive a flat discount (e.g., 20% off fillings).

-

You pay the reduced price directly to the dentist.

Which is better? For basic care, traditional insurance often wins if you need multiple fillings or a root canal. Discount plans work well if you only need preventive care and one or two small procedures per year.

How to Choose a Plan with Strong Basic Dental Coverage

Not all basic coverage is created equal. Here are the specific features to look for when comparing plans.

Look for 80% Coinsurance on Fillings

Some plans offer only 70% coverage for basic care. That 10% difference adds up. A $300 filling costs you $90 with 70% coverage. The same filling costs $60 with 80% coverage.

Check the Waiting Periods

If you know you need a filling or extraction soon, avoid plans with long waiting periods. Some PPO plans have zero waiting periods for basic care. Others require six months.

Verify Root Canal Classification

Call the insurance company and ask directly: “Is a molar root canal covered as basic or major care?” Get the answer in writing. This single question can save you $500 or more.

Review the Annual Maximum

A $1,000 annual maximum is low. A $2,000 maximum is generous. If you expect to need multiple basic procedures, aim for a higher maximum. Some plans offer unlimited maximums, but premiums are higher.

Confirm Your Dentist Is In-Network

Out-of-network dentists can balance bill you. That means they charge the difference between their fee and what insurance pays. Stay in-network for basic care to maximize your savings.

What to Do If Your Basic Coverage Is Insufficient

Sometimes your plan just does not cover what you need. Here are practical alternatives.

Ask About Payment Plans

Many dental offices offer in-house financing. You can pay for a root canal or multiple fillings over six months with no interest. Always ask before saying no to treatment.

Consider a Dental School

Dental schools offer reduced fees. A filling might cost $50 instead of $200. Students perform the work under supervision. Appointments take longer, but the savings are real.

Use a Health Savings Account (HSA) or Flexible Spending Account (FSA)

If you have an HSA or FSA through work, you can use pre-tax dollars for basic dental care. This effectively gives you a 20% to 30% discount, depending on your tax bracket.

Negotiate the Cash Price

If you do not have insurance or have met your annual maximum, ask for the cash price. Many dentists offer a 10% to 15% discount for same-day payment with cash or credit card.

Common Myths About Basic Dental Care Coverage

Let us clear up some misunderstandings.

Myth 1: “Basic coverage pays for everything except cleanings.”

Truth: Basic coverage is limited to specific procedures. It does not cover crowns, bridges, implants, or most orthodontics.

Myth 2: “I can use my basic coverage immediately after signing up.”

Truth: Waiting periods often apply. Read your contract. Some plans delay basic coverage for three to six months.

Myth 3: “If my dentist says I need it, insurance will pay.”

Truth: Insurance companies have their own definitions of medical necessity. Your dentist may recommend a composite filling on a back tooth. Your plan may only pay for an amalgam filling. Always verify coverage before treatment.

Myth 4: “Basic coverage has no dollar limits.”

Truth: The annual maximum applies. Once you hit that limit, you pay 100% of all basic and major care costs until the plan year resets.

How to Maximize Your Basic Dental Benefits

You pay for your insurance every month. Make sure you get your money’s worth.

Schedule Treatment Before the Year Ends

Most plans reset on January 1st. If you have not used your basic coverage, schedule that filling or extraction in December. Do not lose your benefits.

Bundle Procedures

If you need two fillings and a deep cleaning, do them all in the same calendar year. This helps you meet your deductible once instead of twice.

Ask for a Pre-Treatment Estimate

Before any non-emergency basic procedure, ask your dentist to send a pre-treatment estimate to your insurance company. This is a formal prediction of what they will pay. It is not a guarantee, but it is highly accurate.

Maintain Preventive Care

This sounds obvious, but it is critical. Regular cleanings and exams catch small cavities early. A small filling is basic care. A large cavity that needs a crown is major care. Preventive care saves you from paying for major care later.

A Complete Checklist: Questions to Ask Your Insurance Company

Before you enroll in a plan or schedule a procedure, ask these specific questions.

-

What is my deductible for basic care?

-

Has my deductible been met for this year?

-

What is my coinsurance percentage for fillings? For extractions? For root canals?

-

Is there a waiting period for basic services? If yes, how long?

-

What is my annual maximum?

-

How much of my annual maximum have I used so far?

-

Does my plan cover composite fillings on back teeth?

-

Are molar root canals covered as basic or major?

-

Is my dentist in-network for basic services?

-

Does my plan require a referral for basic care?

Write down the answers. Keep them with your insurance card.

The Future of Basic Dental Coverage

The dental insurance industry is changing slowly. But there are positive trends.

Increased Coverage for Preventive Basics

More plans now cover three cleanings per year instead of two, especially for patients with gum disease. Some plans cover four cleanings annually for diabetics and pregnant women.

Tele-dentistry for Basic Triage

Some insurers now cover virtual consultations. You can send photos of a toothache to a dentist. They determine if you need basic care (a filling) or emergency care. Tele-dentistry visits often cost $0 to $10.

Higher Annual Maximums

Employer-sponsored plans are slowly raising annual maximums from $1,000 to $1,500 or $2,000. Inflation in dental costs makes lower maximums nearly useless. Expect this trend to continue.

Frequently Asked Questions (FAQ)

1. Is a tooth extraction considered basic or major dental care?

A simple extraction (tooth visible above the gum line) is almost always basic care. A surgical extraction (impacted or broken below the gum line) is often major care or requires a separate benefit.

2. Does basic dental coverage include anesthesia?

Generally, no. Local anesthesia (numbing shots) is included in the procedure cost. General anesthesia or IV sedation is usually not covered for basic procedures unless medically necessary.

3. Can I use basic coverage immediately after buying a policy?

Not always. Many plans impose a 3 to 6 month waiting period for basic services. Some employer plans waive this if you had prior coverage. Always check.

4. What happens if I need a crown after a root canal?

The root canal may be basic care. The crown is major care. You will pay two different coinsurance amounts. The crown will likely be covered at 50%, not 80%.

5. Does basic coverage pay for X-rays?

Yes, but diagnostic X-rays (bitewings and periapicals) are usually preventive care, not basic. Full-mouth X-rays (FMX) may be covered under basic or major, depending on the plan.

6. Are night guards for teeth grinding considered basic care?

Rarely. Most plans consider night guards (occlusal appliances) as major care or exclude them entirely unless you have documented severe bruxism with tooth damage.

7. What if my dentist says I need a filling, but my insurance denies it?

You can appeal the decision. Your dentist can submit clinical notes and X-rays. Many denials are overturned on appeal. Do not accept the first “no” as final.

8. Does basic coverage include periodontal surgery?

No. Periodontal surgery (flap surgery, gum grafts) is typically major care. Scaling and root planing (deep cleaning) is basic care. Surgery is a higher level.

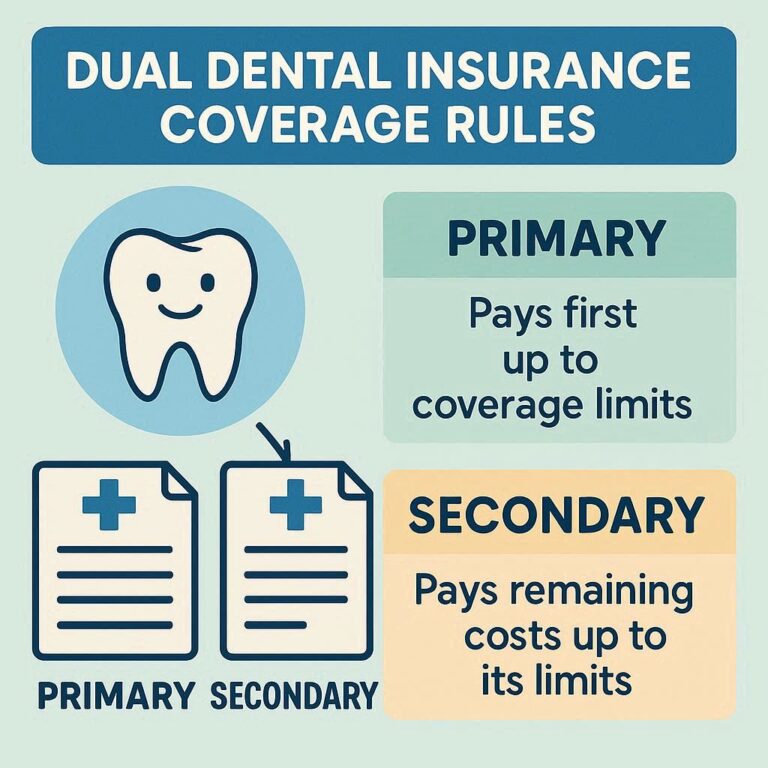

9. Can I have two dental insurance plans?

Yes. If you have coverage through your employer and your spouse’s plan, you can coordinate benefits. The primary plan pays its share. The secondary plan may pay some or all of your remaining coinsurance.

10. Is basic dental coverage worth it if I have healthy teeth?

Yes. The value is in the preventive care. Cleanings and exams are usually free. If you develop one cavity, the insurance pays for most of the filling. The premium often costs less than paying out-of-pocket for two cleanings and one filling per year.

Additional Resource

For an official, unbiased guide to comparing dental plans and understanding your rights, visit the National Association of Dental Plans (NADP) website.

👉 Link: www.nadp.org/consumers/

This resource provides a glossary of terms, a plan comparison tool, and state-specific consumer assistance contacts.

Conclusion

Basic dental care coverage is the workhorse of your insurance policy. It pays for fillings, simple extractions, root canals on front teeth, and gum treatments. Most plans cover 70% to 80% of these costs after you meet a small deductible. Understanding what is included, what is not, and how waiting periods and annual maximums work will save you money and frustration. Always read your specific policy, ask questions before treatment, and use your benefits before they expire each year.