The Ultimate Guide to Affordable Dental Insurance for College Students

The life of a college student is a complex tapestry woven with threads of academic pursuit, social exploration, and profound personal growth. It is a time defined by late-night study sessions, the forging of lifelong friendships, and the exhilarating, often daunting, journey toward independence. Yet, amidst this whirlwind of lectures, exams, and extracurricular activities, a critical aspect of well-being is frequently relegated to the bottom of the priority list: dental health. For many students, the transition to college also marks the first time they are solely responsible for their own healthcare, a responsibility that is often complicated by the constraints of a tight budget. The high cost of dental procedures—from a simple cleaning that can exceed $100 to a root canal that can soar into the thousands—can feel like an insurmountable barrier, leading many to postpone or forgo essential care entirely. This neglect, however, can have severe consequences, transforming a minor, manageable issue into a major dental emergency that is not only painful but also financially catastrophic. The myth that young, healthy individuals are immune to significant dental problems is a dangerous one; cavities, gum disease, and wisdom tooth complications do not discriminate based on age or academic status.

This comprehensive guide is designed to dismantle those barriers and demystify the path to affordable dental care for the modern college student. We will embark on a detailed exploration of the various insurance landscapes available to you, from student health plans and parental policies to state-sponsored programs like Medicaid and individual marketplaces. We will dissect the often-overlooked yet crucial differences between dental insurance and dental discount plans, empowering you to make an informed decision that aligns with your unique financial and health needs. Furthermore, recognizing that insurance is not the only solution, we will provide an exhaustive resource on alternative pathways to care, with a special focus on locating and utilizing free and low-cost dental clinics, particularly for students residing in New Jersey. Our mission is to equip you with the knowledge, strategies, and resources necessary to proactively manage your oral health, ensuring that your smile remains as bright and healthy as your future, without plunging your finances into disarray. Your dental health is an integral component of your overall wellness and academic success; it is time to give it the attention it deserves.

1. Why Dental Care is Non-Negotiable for College Students

The Oral-Systemic Health Link: More Than Just a Pretty Smile

For decades, dentistry was viewed as a siloed field, concerned solely with the health of teeth and gums. Modern medical research has fundamentally shattered this misconception, revealing a profound and bidirectional relationship between oral health and overall systemic health. The mouth serves as a gateway to the body, and the state of one’s oral cavity can have far-reaching implications. Periodontal disease, a severe form of gum infection characterized by inflammation and bleeding, is not an isolated condition. The same bacteria responsible for destroying gum tissue and the bone supporting the teeth can enter the bloodstream through compromised gum tissue, traveling throughout the body and contributing to a host of serious medical issues. Numerous peer-reviewed studies have established strong correlations between chronic periodontal disease and the development or exacerbation of cardiovascular diseases, including endocarditis (an infection of the inner lining of the heart) and atherosclerosis (clogged arteries). Furthermore, the inflammatory response triggered by gum disease can worsen blood sugar control, creating a dangerous feedback loop for individuals with diabetes. For college students, who often experience high levels of stress, poor sleep, and erratic eating habits—all factors that can compromise the immune system—maintaining good oral health becomes a critical line of defense in preserving their overall physical well-being.

The Domino Effect of Neglect: From Cavity to Crisis

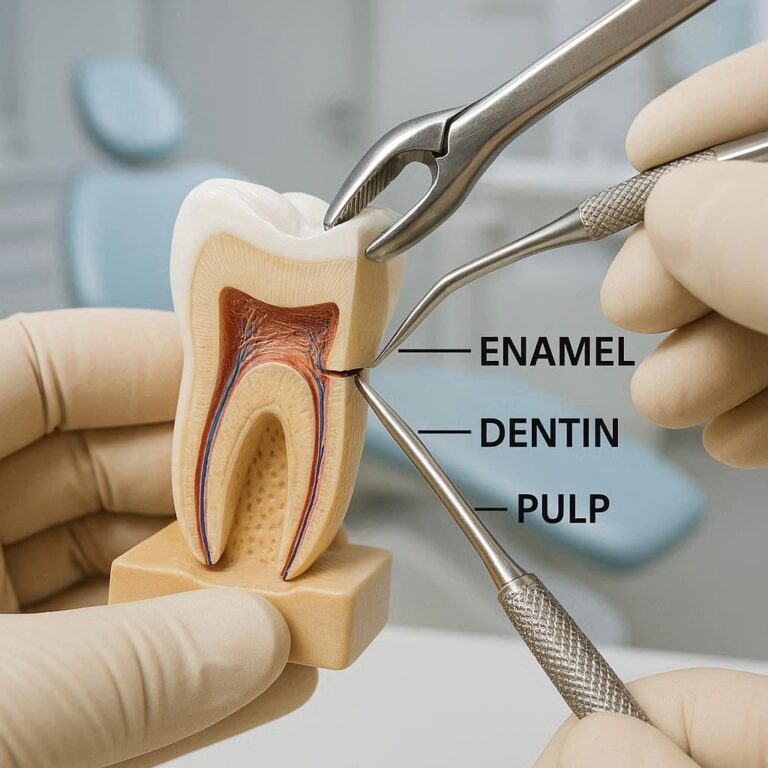

The trajectory of dental neglect often follows a predictable and costly pattern, a domino effect that begins with a single, overlooked issue. Consider a common scenario: a student notices a slight sensitivity to cold in a molar but, burdened by exams and a limited budget, decides to ignore it. This sensitivity is likely the early warning sign of a cavity—a small area of decay in the tooth’s enamel. Left untreated, the cavity progresses, boring deeper into the tooth structure. Within months, the decay may reach the dentin, a softer layer beneath the enamel, causing more persistent pain. Ignoring this stage leads the bacteria to the tooth’s pulp, the innermost chamber containing nerves and blood vessels. This infection, known as pulpitis, causes severe, often debilitating, toothache. At this point, the student is faced with a dental emergency. The simple, inexpensive filling that could have resolved the issue at the first sign of sensitivity is no longer an option. The required treatment is now a root canal, a procedure that is not only significantly more complex and painful but also exponentially more expensive, often costing between $800 and $1,500 for a molar. If even the root canal is delayed, the infection can spread to the root tip, forming an abscess. This can lead to systemic infection, hospitalization, and the eventual loss of the tooth, necessitating a dental implant or bridge—procedures that can cost thousands of dollars. This domino effect illustrates a fundamental truth of dentistry: procrastination is profoundly expensive, both in terms of financial cost and physical discomfort.

The Impact on Academic Performance and Social Confidence

Beyond the physical pain and systemic health risks, poor dental health can inflict a significant toll on a student’s academic performance and psychological well-being. A severe toothache is not a minor distraction; it is an all-consuming pain that can make concentrating on lectures, reading complex texts, or studying for crucial exams nearly impossible. The sleep deprivation that often accompanies dental pain further erodes cognitive function, memory retention, and the ability to perform under pressure. The repercussions extend beyond the library and lecture hall. Dental issues, particularly those that are visible, such as stained, crooked, or missing teeth, can severely impact self-esteem and social confidence. In an environment where students are constantly forming new relationships, networking for future opportunities, and participating in interviews for internships and jobs, the confidence to speak and smile freely is invaluable. The self-consciousness associated with dental problems can lead to social withdrawal, anxiety in group settings, and a reluctance to engage fully in the collegiate experience. Investing in dental health, therefore, is not merely a medical or financial decision; it is an investment in one’s academic success, social fulfillment, and long-term professional trajectory.

2. Navigating the Maze of Dental Insurance Options

Understanding the different avenues for obtaining dental coverage is the first step toward securing affordable care. Each option comes with its own set of rules, benefits, and limitations.

Staying on Your Parents’ Plan: The ACA and Age 26 Rule

One of the most straightforward and cost-effective solutions for many traditional-aged undergraduate students is to remain on their parents’ dental insurance plan. The Affordable Care Act (ACA) mandates that health insurance plans that offer dependent coverage must allow children to stay on their parent’s plan until they turn 26 years old. This provision typically extends to embedded dental coverage or stand-alone dental plans purchased by the parents. This can be an ideal situation, as the student benefits from coverage without directly paying the premiums. However, several critical factors must be considered. First, you must verify that your parents’ plan includes dental benefits, as not all health plans do. Second, you need to confirm the network of dentists covered by the plan. If you are attending college out-of-state, the plan may have a limited or non-existent network of providers in your college town, potentially rendering the coverage much less useful or requiring you to pay higher out-of-network costs. It is essential to contact the insurance provider or use their online provider directory to locate in-network dentists near your campus before assuming this is a viable option.

University-Sponsored Student Dental Plans

Many colleges and universities recognize the dental care gap faced by their students and have responded by offering sponsored student dental insurance plans. These plans are often offered as a voluntary, opt-in benefit, separate from the mandatory student health insurance plan. They are typically negotiated by the university to provide competitive group rates that are more affordable than individual plans on the open market. The primary advantage of these plans is their convenience and campus-centric design. The provider networks are often built to include dentists in the immediate college community, making it easy to find a local, in-network provider. The plans are also designed with a student budget in mind, often focusing on high-level preventive care (cleanings, exams, X-rays) with low or no copays, while offering discounted rates for basic and major procedures. To explore this option, students should visit their university’s student health services website or contact the office directly to inquire about the availability of a dental plan, request a detailed summary of benefits, and understand the enrollment periods, which are often limited to the start of the academic year or during open enrollment windows.

Medicaid (NJ FamilyCare): Eligibility and Coverage for Students

Medicaid, known as NJ FamilyCare in New Jersey, is a joint federal and state program that provides health coverage to low-income individuals and families, including comprehensive dental benefits for children and, importantly, for adults as well. The expansion of Medicaid under the ACA has made many more low-income adults, including college students, eligible for coverage. Eligibility is primarily based on modified adjusted gross income (MAGI). For a single individual in 2025, this often means an income below approximately $20,000 per year (this threshold is updated annually). Many full-time students, particularly those who work part-time or not at all, may fall within this income bracket and qualify for NJ FamilyCare. The dental benefits under NJ FamilyCare for adults are robust, typically covering preventive services (cleanings, exams, X-rays) at 100%, basic restorative services (fillings) with a small copay, and even major services like root canals, crowns, and dentures, often subject to prior authorization. For eligible students, NJ FamilyCare represents the most comprehensive and affordable dental coverage available, often with no monthly premium. Application can be made online through the NJ FamilyCare website at any time during the year.

The Health Insurance Marketplace (Get Covered NJ)

For students who do not qualify for Medicaid, cannot stay on their parents’ plan, and find the university plan unsuitable, the Health Insurance Marketplace, known as Get Covered NJ, is a viable alternative. This state-based marketplace was established under the ACA and allows individuals to shop for and purchase health and dental insurance plans. Dental coverage on the marketplace is offered in two ways: bundled with a Qualified Health Plan (QHP) or as a stand-alone dental plan. It is important to note that while medical insurance for children is an Essential Health Benefit that must be offered, adult dental coverage is not. Therefore, you must actively seek out a plan that includes it. The marketplace offers a structured shopping experience, allowing you to compare plans from different insurers based on premium cost, deductibles, copays, and provider networks. Depending on your income, you may also qualify for premium tax credits and cost-sharing reductions that can significantly lower your monthly costs for a health plan, though these subsidies generally do not apply to stand-alone dental plans. The open enrollment period for Get Covered NJ typically runs from November 1 to January 31, but certain qualifying life events, such as losing other coverage, moving, or getting married, can trigger a Special Enrollment Period, allowing you to enroll outside of the standard window.

Individual Dental Insurance Plans: A Direct Purchase

If none of the above options are feasible, students can always purchase a dental insurance plan directly from an insurance company. Major carriers like Delta Dental, Cigna, Guardian, and MetLife all offer individual and family plans that can be purchased online or through an agent. This route offers the most flexibility, as you can choose from a wide variety of plan types (DHMO, PPO) and benefit levels to find one that precisely matches your needs and budget. The downside is that these plans can be more expensive than group plans offered through a university or employer, as you are not benefiting from the risk-pooling that lowers group rates. When shopping for an individual plan, it is crucial to pay close attention to waiting periods, particularly for major services like crowns and root canals. Many individual plans impose waiting periods of 6 to 12 months for basic services and 12 to 24 months for major services, meaning you cannot receive coverage for those procedures until you have been enrolled in the plan for that length of time. This makes individual plans a better option for proactive, preventive care rather than a solution for an immediate dental problem.

3. Dental Insurance vs. Dental Savings Plans: A Critical Distinction

A common point of confusion arises from the difference between traditional dental insurance and dental savings plans (also known as dental discount plans). They are fundamentally different products.

How Traditional Dental Insurance Works (DHMO vs. PPO)

Traditional dental insurance operates on a model similar to medical insurance, where you pay a monthly or annual premium. In return, the insurance company agrees to pay for a portion of your dental care costs, as outlined in your plan documents.

-

Dental Health Maintenance Organization (DHMO): A DHMO is a more restrictive, but typically lower-cost, model. You must choose a primary care dentist from a designated network and receive all your care from that dentist or a specialist to whom they refer you. There are no annual maximums or deductibles in the traditional sense; instead, you pay a fixed copayment for each service (e.g., $10 for a cleaning, $25 for a filling). DHMOs do not cover out-of-network care except in true emergencies.

-

Preferred Provider Organization (PPO): A dental PPO offers more flexibility at a higher cost. You have the freedom to see any dentist you choose, but you will pay significantly less if you use a dentist within the plan’s “preferred” network. PPO plans typically have an annual deductible (e.g., $50) that you must meet before the insurance starts paying, and they pay a percentage of the costs (e.g., 100% for preventive, 80% for basic, 50% for major). They also have an annual maximum (e.g., $1,500), which is the most the insurance will pay in a given year.

The Rise of Dental Savings Plans: An Alternative Model

A dental savings plan is not insurance. It is a membership program that provides access to discounted rates on dental services. You pay an annual membership fee (typically $80-$200 for an individual) to gain access to a network of dentists who have agreed to provide services at a reduced, pre-negotiated rate for plan members. There are no deductibles, no annual maximums, and no claims forms. You simply pay the discounted fee directly to the dentist at the time of service. For example, a cleaning that normally costs $120 might be available for $60 through the plan. A crown that costs $1,200 might be discounted to $800.

Side-by-Side Comparison: Which is Right for You?

The following table provides a clear, side-by-side comparison to help you decide.

Table 1: Dental Insurance vs. Dental Savings Plan

| Feature | Traditional Dental Insurance | Dental Savings Plan |

|---|---|---|

| Cost Model | Monthly/Annual Premiums, Deductibles, Copays/Coinsurance | Annual Membership Fee |

| How it Pays | Insurance company pays a portion of the cost after deductible. | You pay 100% of the discounted fee directly to the dentist. |

| Annual Maximum | Yes, typically $1,000 – $2,000. | No annual maximum on discounts. |

| Waiting Periods | Common for basic and major procedures. | Usually no waiting periods; discounts active immediately. |

| Network | Must use in-network providers for best rates (especially DHMO). | Must use in-network providers to receive the discount. |

| Best For | Students who need predictable coverage for a mix of preventive and expected restorative work and value the safety net of an annual maximum. | Students who are primarily seeking preventive care, have no immediate major needs, are facing long waiting periods on insurance, or need significant work that would exceed a low annual maximum. |

4. A Step-by-Step Guide to Choosing the Right Plan

Armed with an understanding of the options, you can now systematically evaluate which path is best for you.

Step 1: Conduct a Personal Dental Health Assessment

Be honest with yourself about the current state of your oral health and your anticipated needs. Have you been diligent with check-ups and have no known issues? A basic plan or discount plan may suffice. Do you have a history of cavities, know your wisdom teeth are problematic, or haven’t seen a dentist in several years? A more robust PPO plan, despite its higher premium, could save you money in the long run.

Step 2: Analyze Your Financial Landscape (Premiums, Deductibles, Copays)

Look beyond the monthly premium. Calculate the total potential annual cost:

-

Premium: $25/month x 12 months = $300 per year.

-

Deductible: If the plan has a $50 deductible, add that.

-

Copays/Coinsurance: Estimate the cost for two cleanings, an exam, and any potential fillings.

Compare this total estimated cost across different plans. A plan with a $0 premium but a 20% coinsurance on a $1,000 procedure would cost you $200, which might be more than a plan with a $200 premium that covers the same procedure at 80% ($160 out-of-pocket).

Step 3: Understand Key Terminology: Annual Maximums, Waiting Periods, and UCR

-

Annual Maximum: The total amount the insurer will pay in a benefit year. Once you hit this limit, you pay 100% of all further costs. This is a critical number for anyone anticipating significant work.

-

Waiting Periods: The time you must wait after enrollment before being eligible for certain services. Avoid plans with long waiting periods if you need care soon.

-

UCR (Usual, Customary, and Reasonable): The amount your insurer considers a reasonable fee for a service in your geographic area. If your dentist charges more than the UCR, you will be responsible for the difference (if you are out-of-network).

Step 4: Scrutinize the Provider Network

Use the insurer’s online directory to search for providers near your campus and your permanent home (for breaks). Ensure there are multiple in-network dentists, specialists (like orthodontists or oral surgeons), and that they are accepting new patients.

Step 5: Read the Fine Print on Exclusions and Limitations

Most plans do not cover cosmetic procedures (teeth whitening). Some may have limitations on the frequency of certain services (e.g., one set of bitewing X-rays per year) or exclude specific materials (e.g., composite/”white” fillings on back teeth).

5. Beyond Insurance: Proactive and Preventative Strategies for Affordable Care

Insurance is a tool, but the most affordable dental care is the care you never need. Combining coverage with proactive strategies is the ultimate key to cost containment.

The Power of Prevention: Your At-Home Dental Arsenal

The cornerstone of affordable dental health is a relentless commitment to prevention. This means brushing your teeth thoroughly twice a day with a fluoride toothpaste, flossing daily to remove plaque from between teeth where brushes cannot reach, and considering the use of an antimicrobial mouthwash. A healthy diet low in sugary and acidic foods and drinks (like soda, sports drinks, and candy) is equally important. These simple, low-cost habits are the most powerful insurance policy you can ever have.

Dental School Clinics: High-Quality Care at a Fraction of the Cost

Dental schools are an outstanding, though often overlooked, resource for high-quality, low-cost dental care. In New Jersey, the Rutgers School of Dental Medicine in Newark provides a wide range of services at significantly reduced rates. The care is provided by dental students who are closely supervised by licensed, experienced faculty dentists. Because the primary goal is education, appointments can take longer than in a private practice. However, the trade-off is access to comprehensive care—from cleanings and fillings to root canals and crowns—at prices that can be 30-50% lower than a private dentist. This is an excellent option for complex procedures that might exceed the annual maximum of a typical student insurance plan.

Community Health Centers: A Pillar of Accessible Care

Federally Qualified Health Centers (FQHCs) and other non-profit community health centers are located throughout New Jersey and provide healthcare, including dental services, on a sliding fee scale based on your income. This means that if you are uninsured or underinsured, the cost of your care will be adjusted to what you can reasonably afford. These centers are mission-driven to serve the community, regardless of a patient’s ability to pay. They offer a safety net for essential dental services and are a critical resource during times of financial hardship.

6. Finding Free Dental Clinics in New Jersey: A Comprehensive Resource

For students facing a true financial emergency, free dental clinics provide a vital lifeline.

How Free Dental Clinics Operate and Who They Serve

Free dental clinics are typically run by non-profit organizations, faith-based groups, or in partnership with local health departments. They are staffed by volunteer dentists, dental hygienists, and other professionals who donate their time and expertise. Due to high demand and limited resources, these clinics often focus on addressing pain and infection (extractions, fillings) rather than providing comprehensive or cosmetic care. They primarily serve low-income, uninsured, and underinsured individuals. Eligibility often requires proof of income and residency.

Navigating the New Jersey Department of Health Resources

A good starting point for finding help is the New Jersey Department of Health’s website. They maintain directories and links to public health services, including dental care resources for low-income residents.

Spotlight on Key Service Providers

-

NJDA Donated Dental Services (DDS): This program, run by the New Jersey Dental Association in conjunction with the Dental Lifeline Network, matches volunteer dentists and dental labs with vulnerable patients who are elderly, disabled, or medically compromised. While not for routine student care, it can be a resource for those with special needs.

-

Zufall Health: With several locations in northern New Jersey (including Dover, Denville, and Flemington), Zufall Health provides integrated medical and dental care on a sliding fee scale. They are a key FQHC for the region.

-

Henry J. Austin Health Center: Located in Trenton, this is another major FQHC providing comprehensive dental services to the community, including students, on a sliding scale.

-

Dental Lifeline Network • New Jersey: This is the umbrella organization for the DDS program mentioned above. Their website is a central hub for information on accessing donated dental care for those who qualify.

What to Expect at Your First Free Clinic Visit

Be prepared for potential wait times, both to get an appointment and on the day of your visit. Bring any form of identification you have, proof of address, and any documentation of your income (such as a student financial aid award letter, pay stubs, or a bank statement). Be patient and respectful of the staff and volunteers who are providing this essential service. The care you receive will be focused on resolving your most urgent dental problems.

7. Case Studies: Real-World Scenarios for New Jersey College Students

Case Study 1: Anisa, the Rutgers University Sophomore

Anisa is a 19-year-old sophomore at Rutgers University-New Brunswick living on campus. Her parents’ insurance is a medical-only plan, so she has no dental coverage. She is generally healthy but hasn’t had a cleaning in over a year and is concerned about cost.

-

Solution: Anisa visits the Rutgers Student Health website and discovers the university offers a voluntary Delta Dental PPO student plan. The premium is $25/month, with no deductible for preventive care and a large network of dentists in New Brunswick. She enrolls during the fall open enrollment, schedules a cleaning and exam, and pays only a $5 copay for each visit. The plan gives her peace of mind for the rest of the academic year.

Case Study 2: Ben, the Montclair State University Graduate Student

Ben is a 25-year-old graduate student at Montclair State University working as a teaching assistant. His stipend is $18,000 per year. He has a severe toothache and knows he needs significant work.

-

Solution: Ben’s low income makes him eligible for NJ FamilyCare. He applies online and is approved within a few weeks. His coverage includes comprehensive dental benefits. He finds an in-network dentist near campus, gets a root canal and crown, and only pays minimal copays for the procedures, saving him thousands of dollars.

Case Study 3: Chloe, the Princeton University Student on a Gap Year

Chloe has just graduated from Princeton and is taking a gap year before starting medical school. She is working part-time and will lose her university-sponsored insurance in two months. She needs to find her own coverage.

-

Solution: Since losing her student coverage is a Qualifying Life Event, Chloe is eligible for a Special Enrollment Period on Get Covered NJ. She shops for a stand-alone dental plan and chooses a DHMO from a major carrier. The plan costs her $15/month, has no deductible, and provides the preventive care she needs with low, predictable copays until she starts her next program.

8. Conclusion: Investing in Your Smile is Investing in Your Future

Neglecting dental health during your college years can lead to severe physical, financial, and academic consequences down the line. By thoroughly exploring all available options—from parental plans and university offerings to Medicaid and dental discount plans—you can find a solution that fits your budget. Proactive prevention, combined with the strategic use of low-cost resources like dental schools and community clinics, ensures that you can maintain a healthy smile throughout your academic journey and beyond. Your oral health is a critical component of your overall well-being and success; make it a priority today.

9. Frequently Asked Questions (FAQs)

Q1: I’m 24 and on my parents’ health insurance. Am I automatically on their dental plan?

A: Not necessarily. You must check with your parents or their insurance provider to confirm if their health plan includes embedded dental benefits or if they have a separate, stand-alone dental plan that you are enrolled on. Many medical plans do not include dental for adults.

Q2: What is the single most important thing I can do to save money on dental care?

A: Without a doubt, it is prevention. Consistent and proper brushing and flossing, combined with regular professional cleanings (even if you pay out-of-pocket for them), are far less expensive than treating a single cavity or, worse, a root canal.

Q3: I have a dental emergency right now (severe pain, swelling) and no insurance. What should I do in New Jersey?

A: Do not wait. Your first stop should be a Federally Qualified Health Center (FQHC) like Zufall Health or Henry J. Austin, which can often see patients urgently and use a sliding fee scale. You can also call 211 in New Jersey, which is a free, confidential helpline that can connect you to the nearest emergency dental clinic or charitable care provider.

Q4: Are dental savings plans a scam?

A: Reputable dental savings plans from major companies are not scams. They are legitimate membership programs that provide discounts. However, it is crucial to verify that there are several participating dentists in your area before you sign up. Always research the company and read reviews.

Q5: How can I find a dentist near my New Jersey college campus that accepts my insurance?

A: The most reliable method is to use the “Find a Dentist” or “Provider Directory” tool on your insurance company’s website. You can search by zip code and filter for providers who are accepting new patients. It is always a good practice to call the dentist’s office directly to confirm they are still in-network before booking your appointment.

10. Additional Resources

-

Get Covered NJ: https://www.getcovered.nj.gov – The official health insurance marketplace for New Jersey.

-

NJ FamilyCare: https://www.njfamilycare.dhs.state.nj.us – Official site for Medicaid and CHIP in New Jersey.

-

Rutgers School of Dental Medicine Patient Care: https://sdm.rutgers.edu/patient_care/ – Information on services and appointments at the dental school clinic.

-

NJ 211: Dial 2-1-1 or visit https://nj211.org – A comprehensive resource database for health and human services in New Jersey.

-

Dental Lifeline Network • New Jersey: https://dentallifeline.org/new-jersey/ – Information on the Donated Dental Services program.

Disclaimer: This article is for informational purposes only and does not constitute financial, medical, or insurance advice. The information presented was accurate as of the stated publication date, but insurance plans, policies, and clinic details are subject to change. Always verify details directly with insurance providers, educational institutions, and healthcare clinics before making any decisions.

Date: November 15, 2025

Author: The Student Wellness Guide Team