average dental care cost per month

Imagine this: you’re biting into a crisp apple and feel a sudden, sharp jolt of pain. Or, you’re in a routine dental check-up, expecting a quick clean, only to hear the dentist say, “We’re seeing some issues that need attention.” In that moment, a single question flashes through your mind, often accompanied by a wave of anxiety: “How much is this going to cost?”

The quest to determine an “average dental care cost per month” is more than an academic exercise; it is a fundamental part of personal financial planning and overall health management. Your oral health is inextricably linked to your systemic health, with research connecting gum disease to conditions like heart disease, diabetes, and stroke. Yet, despite its importance, dental care remains one of the most common sources of financial stress for individuals and families. The challenge is that the “average” is a phantom—a number that can be dangerously misleading without context. A 25-year-old with no issues will have a vastly different monthly cost profile than a 55-year-old needing a dental implant.

This definitive guide moves beyond simplistic averages. We will deconstruct the complex ecosystem of dental costs, insurance, and payment strategies to provide you with a clear, actionable framework for understanding and planning your monthly dental expenses. Our goal is not to give you one number, but to equip you with the knowledge to calculate your own number, transforming dental care from a source of fear into a manageable, predictable part of your healthy lifestyle. We will explore everything from the price of a routine cleaning to the financial impact of major procedures, the pros and cons of insurance, and innovative strategies to make high-quality care accessible. Consider this your comprehensive roadmap to navigating the financial landscape of dental health.

2. Deconstructing the “Average”: Why a Single Monthly Figure is Misleading

When you search for “average dental care cost per month,” you will find figures ranging from $20 to $80 or more. These numbers are often calculated by taking the average annual cost of dental care (including insurance premiums) and dividing by twelve. While mathematically correct, this approach is practically useless for individual planning. It’s like calculating the “average monthly temperature on Earth”—it blends the data from deserts and polar ice caps into a meaningless figure for someone planning what to wear in Chicago in January.

The real monthly cost is a dynamic variable influenced by a confluence of factors:

-

Individual Oral Health: This is the most significant factor. A person with excellent genetics and impeccable hygiene may only incur costs for semi-annual preventive care. Someone with a history of cavities, gum disease, or dental trauma will face higher, irregular costs for restorative work.

-

Dental Insurance Status: Are you paying a monthly premium for insurance? If so, that is a fixed monthly cost. But the value of that insurance—how much it reduces your out-of-pocket costs for procedures—dramatically alters your effective monthly spend.

-

Geographic Location: The cost of living directly impacts dental fees. A dental filling in Manhattan, New York, will cost significantly more than the same filling in Topeka, Kansas.

-

Type of Dentist and Materials Used: A general dentist charges less than a specialist like an endodontist (root canal specialist) or periodontist (gum specialist). Furthermore, the choice of materials (e.g., composite resin vs. amalgam filling, porcelain vs. gold crown) carries different price tags.

-

Age and Life Stage: As we will explore in detail, dental needs and associated costs evolve throughout a person’s life.

Therefore, instead of fixating on a national average, we must shift our thinking to a “Personalized Monthly Allocation.” This is the amount you should budget for to cover both predictable, routine costs and to save for unpredictable, inevitable procedures. The following sections will provide the data and framework to build this personalized budget.

3. The Core Components of Dental Costs: A Line-Item Breakdown

To understand your monthly cost, you must first understand the costs of individual procedures. These can be broadly categorized into four tiers.

Preventive Care: The Foundation of Affordable Dentistry

This is the cornerstone of dental health and cost control. Preventive care aims to stop problems before they start and is, by far, the most cost-effective investment you can make.

-

Routine Check-up and Cleaning (Prophylaxis): Typically recommended every six months. This includes an examination, professional cleaning to remove plaque and tartar, and sometimes periodontal maintenance for those with gum disease.

-

Average Cost without Insurance: $90 – $200 per visit. Annually: $180 – $400.

-

*Effective Monthly Cost (Annual/12):* $15 – $33.

-

-

Dental X-Rays (Radiographs): Bitewing x-rays are usually taken annually, and a full-mouth series (panoramic) every 3-5 years.

-

Average Cost without Insurance: Bitewings: $35 – $80. Full Mouth Series: $100 – $250.

-

Effective Monthly Cost (amortized): $3 – $7.

-

-

Fluoride Treatment: Especially common for children but beneficial for adults at high risk of cavities.

-

Average Cost without Insurance: $20 – $50 per treatment.

-

When considering only basic, in-network preventive care for an insured individual, the monthly cost can seem very low, often just the cost of the insurance premium, as these services are frequently covered at 100%. For the uninsured, the predictable monthly allocation for prevention would be roughly $20 – $45.

Basic Restorative Procedures: Fixing Problems Before They Escalate

When prevention fails, basic restorative procedures address common issues like cavities and minor infections.

-

Dental Fillings: Used to treat cavities. Cost varies by the number of surfaces involved and the material (amalgam is cheaper than tooth-colored composite).

-

Average Cost without Insurance per filling: $100 – $300.

-

-

Root Canal Therapy (Endodontics): Treatment for an infected tooth nerve. Cost varies significantly by tooth location (molars are more complex).

-

Average Cost without Insurance: Front Tooth: $600 – $900. Premolar: $700 – $1,000. Molar: $900 – $1,500+.

-

-

Simple Tooth Extraction: Removal of a visible, non-impacted tooth.

-

Average Cost without Insurance: $75 – $300.

-

These procedures are not annual events but unpredictable occurrences. Financially, this means your monthly allocation must include a “savings buffer” to cover these inevitable expenses.

Major Restorative Procedures: The High-Cost Scenarios

This tier includes the procedures that constitute a major financial burden for many households.

-

Dental Crowns (Caps): Used to restore a damaged or root-canaled tooth. Materials (porcelain-fused-to-metal, all-ceramic, gold) greatly affect price.

-

Average Cost without Insurance per crown: $1,000 – $2,500+.

-

-

Dental Bridges: Used to replace one or more missing teeth by anchoring to adjacent teeth.

-

*Average Cost without Insurance for a 3-unit bridge:* $2,000 – $5,000.

-

-

Dental Implants: The modern gold standard for tooth replacement. This is a multi-step process involving a titanium post surgically placed in the jawbone, an abutment, and a crown.

-

Average Cost without Insurance for a single implant (all stages): $3,000 – $6,000+.

-

-

Dentures: Full or partial plates to replace multiple missing teeth.

-

Average Cost without Insurance: Partial: $700 – $1,800. Full (per arch): $1,000 – $3,000+.

-

The cost of a single major procedure can exceed the entire annual “average” dental cost. This underscores the critical importance of insurance or a robust savings plan.

Cosmetic Dentistry: The Elective Investment

These procedures are not medically necessary but are chosen to enhance appearance. They are rarely covered by insurance.

-

Teeth Whitening: Professional in-office or take-home kits.

-

Average Cost without Insurance: $300 – $1,000.

-

-

Porcelain Veneers: Thin shells bonded to the front of teeth to correct shape and color.

-

Average Cost without Insurance per veneer: $1,000 – $2,500.

-

Summary of Common Dental Procedure Costs (Without Insurance)

| Procedure Category | Specific Procedure | Low-End Estimate | High-End Estimate | Typical Frequency |

|---|---|---|---|---|

| Preventive | Routine Check-up & Cleaning | $90 | $200 | Every 6 Months |

| Preventive | Bitewing X-Rays | $35 | $80 | Annually |

| Basic Restorative | Composite Filling (1 surface) | $100 | $300 | As Needed |

| Basic Restorative | Root Canal (Molar) | $900 | $1,500 | As Needed |

| Basic Restorative | Simple Extraction | $75 | $300 | As Needed |

| Major Restorative | Porcelain Crown | $1,000 | $2,500 | As Needed |

| Major Restorative | Dental Implant (Single) | $3,000 | $6,000 | As Needed |

| Cosmetic | Professional Teeth Whitening | $300 | $1,000 | Elective |

4. The Great Moderator: Dental Insurance and Its Impact on Monthly Outlays

For many, dental insurance is the primary tool for managing costs. However, it functions very differently from major medical insurance, and misunderstanding its mechanics is a common financial pitfall.

How Dental Insurance Really Works: Premiums, Deductibles, Copays, and Annual Maximums

-

Monthly Premium: The fixed amount you (or your employer) pay to the insurance company to maintain coverage. This is a guaranteed monthly expense. *Example: $25 – $60 per month for an individual plan.*

-

Deductible: The amount you must pay out-of-pocket before the insurance starts sharing costs for basic and major services. Preventive care is often exempt from the deductible. *Example: $50 – $100 per year.*

-

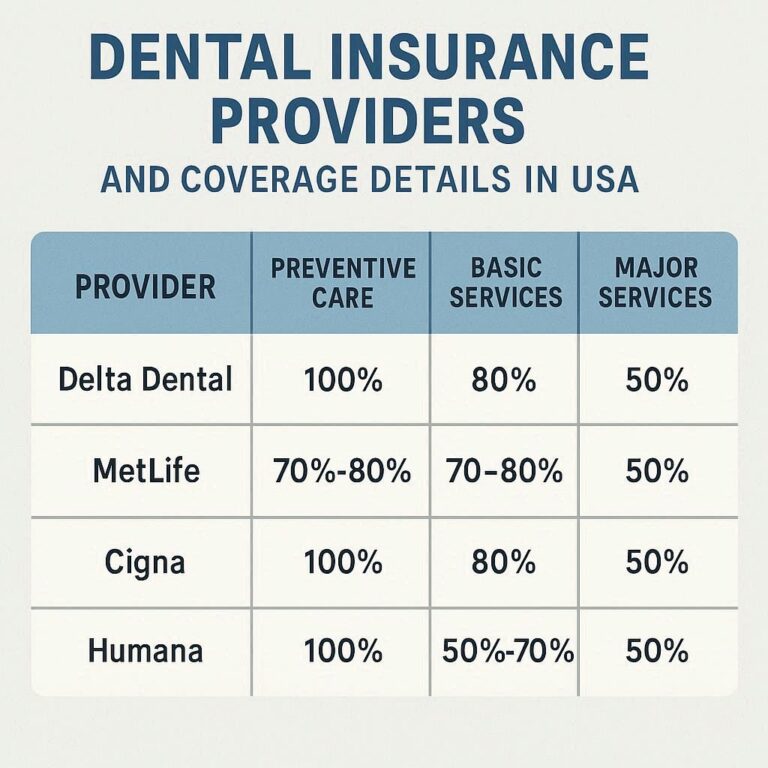

Copay/Coinsurance: The percentage of a procedure’s cost you are responsible for after meeting your deductible. Most plans follow the “100-80-50” structure:

-

Preventive (100%): Cleanings, exams, x-rays are covered at 100%.

-

Basic (80%): Fillings, extractions, root canals are covered at 80%. You pay 20%.

-

Major (50%): Crowns, bridges, implants, dentures are covered at 50%. You pay 50%.

-

-

Annual Maximum: This is the most critical and limiting feature. It is the absolute maximum amount the insurance will pay out for covered services in a calendar year. *Example: $1,000 – $1,500 is a typical range.* Once you hit this maximum, you are 100% responsible for all further costs.

This structure means that dental insurance is designed to manage predictable, moderate expenses, not to fully shield you from catastrophic dental costs. A single crown costing $1,500 could max out a $1,500 policy, leaving you to pay the remaining $500 (your 50%) plus any amount over the maximum.

Types of Dental Insurance Plans: PPO, DHMO, and Discount Plans

-

Dental PPO (Preferred Provider Organization): The most common type. Offers a network of dentists who agree to discounted fees. You can see out-of-network dentists but will pay more. This offers the greatest flexibility.

-

Dental HMO (DHMO or Prepaid Plan): Requires you to choose a primary care dentist from a network. You must get referrals to see specialists. Premiums are lower, but there is typically no coverage for out-of-network care. Copays are fixed amounts rather than percentages.

-

Dental Discount Plans: Not insurance. You pay an annual fee (e.g., $100-$200) to access a network of dentists who have agreed to provide services at a discounted rate (typically 10-60% off). You pay the entire discounted fee at the time of service. There are no annual maximums or claim forms.

Calculating the True Value: Is Dental Insurance Worth It for You?

The value proposition hinges on your expected needs.

-

Scenario A (Low Needs): A young, healthy individual who only needs two cleanings and a check-up per year.

-

Without Insurance: Cost ~$400 annually.

-

With Insurance: Premiums ($30/mo * 12 = $360) + Deductible ($50) = $410. The insurance may cost more than paying out-of-pocket. A discount plan might be better.

-

-

Scenario B (Moderate Needs): An individual needing two cleanings, a set of x-rays, and two fillings.

-

Without Insurance: Cost ~$400 (prevention) + $400 (fillings) = $800.

-

With Insurance: Premiums ($360) + Deductible ($50) + 20% of fillings ($80) = $490. Insurance provides significant savings.

-

-

Scenario C (High Needs): An individual needing a crown.

-

Without Insurance: Cost ~$1,500.

-

With Insurance: Premiums ($360) + Deductible ($50) + 50% of crown ($750, but limited by annual max). If the annual max is $1,500, insurance pays $1,500? No. The calculation is based on the allowed fee. If the crown’s allowed fee is $1,200, insurance pays 50% ($600), and you pay $600. Total cost to you: $360 + $50 + $600 = $1,010. You save $490, but still have a large outlay.

-

The decision is a calculation between your fixed premium and your expected out-of-pocket costs without coverage.

5. Life Stages and Dental Expenses: A Lifelong Financial Journey

Your dental needs are not static. A strategic approach to budgeting must account for these predictable life-stage changes.

Childhood and Adolescence (Ages 0-18)

This stage is heavily focused on prevention, monitoring development, and early intervention. Costs include regular check-ups, cleanings, fluoride treatments, and sealants. Orthodontics (braces) is a major potential expense in the teen years, often costing $3,000-$7,000. Many dental insurance plans have limited orthodontic coverage. Monthly Allocation: Low predictable costs for prevention, but parents should save aggressively for the possibility of orthodontics.

Early to Middle Adulthood (Ages 19-49)

This is often the most variable period. Young adults may neglect care due to cost, leading to more significant problems later. This era sees the need for fillings, possibly root canals from earlier decay, and wisdom teeth extraction. As adults enter their 40s, old fillings may need replacement, and gum disease can become a concern. Monthly Allocation: Should include a robust savings component for restorative work, as this is when the consequences of earlier habits (or lack of care) manifest.

Older Adulthood (Ages 50+)

With age, teeth naturally wear down. Gum recession exposes root surfaces, which are more prone to decay. Existing dental work may fail. This is the stage where major procedures like crowns, bridges, and implants become most common. Dry mouth, a side effect of many medications, can also increase cavity risk. Monthly Allocation: Typically the highest. Focus should be on maintaining existing dental work and having a financial plan for significant replacements.

6. Geographic Variation: The Cost of Care in Your Zip Code

Where you live is a primary driver of cost. Dentists in urban centers and high-cost-of-living areas (Northeast, West Coast) have higher overhead (rent, staff salaries, insurance), which is reflected in their fees. A cleaning in Boston can be 30-50% more expensive than the same cleaning in a rural Midwestern town. When researching costs, always seek localized information.

7. The Dental Savings Plan Alternative: A Modern Approach to Affordability

As discussed, dental discount plans are a popular alternative to traditional insurance, especially for the uninsured. For an annual fee, you gain access to pre-negotiated discounts. The advantages are clear: no annual maximums, no deductibles, no claim forms, and immediate activation. The disadvantage is that you are still paying the entire discounted fee yourself. These plans are excellent for individuals and families who need basic and preventive care and want to lock in lower rates, but they provide no financial protection against a very high-cost procedure.

8. Proactive Strategies to Manage Your Monthly Dental Budget

Taking control of your dental finances requires a proactive, multi-pronged approach.

The Power of Prevention: Daily Habits that Save Thousands

This cannot be overstated. Consistent brushing with fluoride toothpaste, daily flossing, and a diet low in sugary drinks and snacks can prevent the vast majority of common dental problems. The monthly cost of a toothbrush, toothpaste, and floss is negligible compared to the cost of a single filling.

Dental Tourism: A Viable Option or a Risky Gamble?

Traveling to countries like Mexico, Costa Rica, Hungary, or Thailand for major dental work can offer savings of 50-70%. However, this comes with risks: potential issues with quality standards, difficulty in managing complications after returning home, and limited legal recourse. It requires extensive research and is generally recommended only for major, planned procedures with highly vetted clinics.

Negotiating Fees and Understanding Payment Plans

Many dentists are willing to offer a “cash discount” for patients paying upfront. Do not hesitate to ask. For large procedures, most dental offices offer payment plans or can work with third-party medical credit companies like CareCredit. Be sure to understand the terms, as these plans often have high deferred interest rates if not paid in full by the end of the promotional period.

Utilizing Dental Schools for Quality, Low-Cost Care

Dental schools need patients for their students to train on. Care is provided by students under the close supervision of licensed, experienced faculty. The cost is typically 30-50% less than private practice. The trade-off is that appointments take significantly longer. This is an excellent option for budget-conscious individuals needing complex work.

9. Building Your Personal Dental Budget: A Practical Worksheet

Let’s move from theory to practice. Follow these steps to estimate your personalized monthly dental allocation.

-

Identify Your Fixed Monthly Costs:

-

Dental Insurance Premium:

$_________ -

Dental Discount Plan Annual Fee (divided by 12):

$_________ -

Total Fixed Monthly Cost (A):

$_________

-

-

Estimate Your Annual Preventive Costs (if uninsured):

-

2 Check-ups/Cleanings:

$_________ -

Annual X-Rays:

$_________ -

Total Annual Preventive Cost:

$_________ -

Monthly Preventive Allocation (B) (Total/12):

$_________

-

-

Create a “Dental Savings Fund” for Unexpected Procedures:

-

This is the most important step. Based on your age, oral health history, and risk factors, decide on a monthly amount to save for future fillings, crowns, etc. A good starting point is $25 – $75 per month.

-

Monthly Savings Allocation (C):

$_________

-

-

Calculate Your Total Monthly Dental Allocation:

-

A (Fixed Costs) + B (Prevention) + C (Savings) = Your Personalized Monthly Budget

-

Total Monthly Dental Budget:

$_________

-

This budget ensures your routine care is covered and that you are building a financial cushion to handle unexpected procedures without stress.

10. Conclusion: Summarizing the Content of the Article in Three Lines

The average monthly dental cost is a personal calculation, not a universal number, determined by your health, insurance, and location. Effective financial management involves prioritizing preventive care to minimize future expenses and creating a personalized budget that includes both predictable premiums and a savings fund for unforeseen procedures. Ultimately, viewing dental care as a strategic investment in your long-term well-being is the key to achieving both optimal oral health and financial peace of mind.

11. Frequently Asked Questions (FAQs)

Q1: I don’t have dental insurance and need a root canal and crown. What are my options?

A1: This is a common and stressful situation. Your options include: 1) Negotiate a cash discount with your dentist and set up a payment plan. 2) Apply for a medical credit card like CareCredit (read the terms carefully). 3) Seek care at a local dental school for significantly reduced fees. 4) In extreme cases, explore dental tourism, but only after thorough research into the clinic’s credentials.

Q2: Is it better to pay out-of-pocket or have dental insurance?

A2: It depends on your needs. If you are generally healthy and only require routine cleanings and check-ups, paying out-of-pocket might be cheaper than paying monthly premiums. However, if you anticipate needing fillings, crowns, or other restorative work, insurance can provide substantial savings, especially if you stay in-network. Run the numbers based on your expected care.

Q3: Why is dental insurance so limited with low annual maximums?

A3: Unlike medical insurance, which is designed for unpredictable, high-cost events, dental insurance was historically structured as a “benefit” to encourage routine, preventive care. The low annual maximums ($1,000-$1,500) have not kept pace with the rising costs of modern dentistry (e.g., implants), a point of significant criticism.

Q4: How can I reduce my dental costs without sacrificing quality?

A4: The single most effective way is through excellent daily oral hygiene to prevent problems from starting. Secondly, do not skip your six-month cleanings; they are a minor cost that can identify small issues before they become major, expensive ones. Finally, communicate openly with your dentist about financial concerns; they may offer phased treatment plans or alternative solutions.

12. Additional Resources

-

American Dental Association (ADA): www.ada.org – A primary source for finding dentists, understanding procedures, and oral health tips.

-

National Association of Dental Plans (NADP): www.nadp.org – Provides consumer information on understanding different types of dental plans.

-

CareCredit: www.carecredit.com – A leading healthcare credit card for financing treatments (use with caution and understanding of terms).

-

Health Resources & Services Administration (HRSA): findahealthcenter.hrsa.gov – Helps you find federally-funded community health centers that provide dental care on a sliding fee scale based on income.

Date: September 23, 2025

Author: The Financial Wellness Team

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute professional financial or medical advice. Costs, insurance plans, and regulations change frequently. You should consult with a qualified financial advisor, insurance agent, and dental professional for advice tailored to your specific situation before making any decisions. The author and publisher are not liable for any losses or damages related to the use of this information.