Can You Have Double Dental Insurance Coverage?

You have a new job. The new job comes with dental insurance. But you are also still covered under your spouse’s family plan. You look at both cards and think: Can I actually use both?

The short answer is yes. You can have double dental insurance coverage.

However, before you start dreaming of paying absolutely nothing for a root canal, let’s pump the brakes a little. Having two dental plans does not mean you get double the money, double the cleanings, or double the payouts.

In this guide, we will walk you through exactly how dual dental coverage works in the real world. No confusing legal jargon. No false promises. Just honest, practical advice to help you make the most of your benefits.

What Does “Double Dental Insurance” Actually Mean?

Having double dental insurance simply means you are listed as a covered dependent or subscriber on two different dental plans at the same time.

This is very common in households where two partners work. For example:

-

You have your own plan through your employer.

-

You are also covered under your spouse’s plan as a dependent.

It can also happen if you are under 26 and covered by both parents’ separate plans, or if you have an individual plan plus a group plan from a part-time job.

Important Note for Readers

Do not assume you can “double dip.” Dental insurance companies are not banks. They do not let you claim the same service twice and cash two checks. They have strict rules called “Coordination of Benefits” (COB) to prevent this.

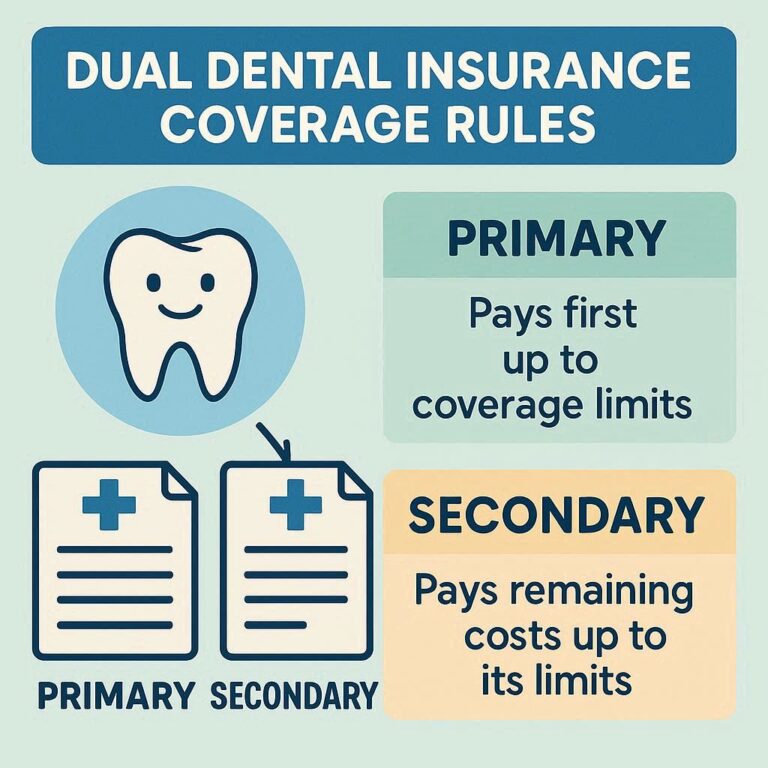

How Does “Coordination of Benefits” (COB) Work?

This is the most important section of this article. If you remember only one thing, remember this: The two insurance companies will talk to each other.

They do not work in isolation. When you have two plans, one is designated as the Primary payer, and the other is the Secondary payer.

The Primary Payer

This plan pays first, up to its limits. They process your claim as if you only had one insurance.

The Secondary Payer

This plan looks at what the primary paid. Then, they might pay some of the remaining balance. But they will never pay more than what they would have paid if they were the only plan.

The Golden Rule of Double Coverage

The total amount paid by both plans combined will never exceed 100% of the dentist’s actual bill.

You will never get paid extra cash back in your pocket.

Who Decides Which Plan is Primary?

The rules are not random. There is a national standard called the “Birthday Rule” and “Non-duplication” clauses. Let’s break it down by real-life scenarios.

Scenario 1: You are the patient (Adult with two jobs)

-

Primary: The plan from the job where you are the employee (active worker).

-

Secondary: The plan where you are a dependent (e.g., spouse’s plan).

Scenario 2: You are a child (Dependent of two parents)

-

Primary: The plan of the parent whose birthday comes first in the calendar year (month/day).

-

Secondary: The plan of the other parent.

Scenario 3: You are a child of divorced or separated parents

-

Primary: The plan of the parent with legal custody.

-

Secondary: The plan of the spouse who has remarried (if applicable) or the non-custodial parent.

Comparative Table: Primary vs. Secondary Responsibility

| Patient Type | Primary Insurance (Pays first) | Secondary Insurance (Pays second) |

|---|---|---|

| You (Employee + Spouse’s plan) | Your employer’s plan | Spouse’s plan |

| You (Medicare + Employer) | Employer group plan | Medicare |

| Child (Married parents) | Parent with earliest birthday | Parent with later birthday |

| Child (Divorced parents) | Custodial parent’s plan | Non-custodial parent’s plan |

The Two Main Types of Dual Coverage Rules

Not all secondary insurance plans are generous. You need to check your policy booklet (the “Evidence of Coverage”) for one of these two clauses.

1. Non-Duplication of Benefits (The Common One)

Most modern dental plans use this rule. It sounds complex, but it is simple.

The secondary plan asks: “Did the primary plan pay more than I would have paid alone?”

If the answer is Yes, the secondary plan pays $0.

If the answer is No, the secondary plan pays the difference (up to their limit).

Real Example (Non-Duplication):

-

Dental bill: $200

-

Primary plan pays: $160 (80%)

-

Secondary plan’s usual rate: $140 (70% of $200)

-

Since $160 is more than $140, the secondary pays $0.

-

You pay: $40 out of pocket.

2. Maintenance of Benefits (The Generous One)

This is older and rarer. Here, the secondary plan adds its benefit on top of the primary’s payment, but still never exceeds the total bill.

Real Example (Maintenance):

-

Dental bill: $200

-

Primary pays: $160

-

Secondary pays: Up to $40 (to reach 100% coverage)

-

You pay: $0.

Most companies today use Non-Duplication because it saves them money. Do not expect full coverage.

Can You Get Two Cleanings Per Year?

This is the number one question people ask.

No. Generally, you cannot get two preventive cleanings per year by using two insurances.

Here is why: Frequency limitations are attached to the patient, not the plan. If Plan A covers two cleanings per year and Plan B covers two cleanings per year, you still only get two cleanings per year as a human being.

If you try to get a cleaning in January (paid by Plan A) and another cleaning in March (paid by Plan B), the dentist’s office will likely catch this. Insurance companies share data through databases like the NEA (National Electronic Attachment) or coordination forms.

Honest advice: Do not try to “game” the system. If you get a cleaning every three months, your dentist will have to submit x-rays and notes. Eventually, the secondary insurance will deny the claim, and you will be stuck with the full dentist bill.

When Does Double Dental Insurance Actually Help?

Having two plans is not useless. It is very useful in specific, high-cost situations. You will see real savings on major procedures.

Where dual coverage shines:

-

Root Canals (Usually $700–$1,500)

-

Crowns ($800–$2,000)

-

Bridges & Implants ($1,500–$5,000)

-

Orthodontics (Braces) for adults or children

How it helps with braces:

Let’s say your primary plan covers 50% of braces up to $1,500 lifetime max. Your secondary plan covers 50% of braces up to $1,000 lifetime max.

-

Total braces cost: $4,000

-

Primary pays: $1,500 (hits its max)

-

Remaining balance: $2,500

-

Secondary pays: $1,000 (hits its max)

-

You pay: $1,500 (instead of $2,500).

That is real savings. Not free, but significantly cheaper.

List: Top 3 Procedures Where Double Coverage Pays Off

-

Oral Surgery (Wisdom teeth removal) – High bills often exceed one plan’s annual maximum.

-

Periodontal (Gum) treatment – Scaling and root planing across four quadrants adds up fast.

-

Full dentures – A full set can cost $3,000+. Two plans can split the weight.

The Hidden “Annual Maximum” Trap

Every dental plan has an annual maximum (usually between $1,000 and $2,500). This is the most money the insurance will pay in 12 months.

When you have double coverage, you have two annual maximums.

-

Plan A Max: $1,500

-

Plan B Max: $1,500

-

Total available: $3,000

However, thanks to the Non-duplication clause, you likely won’t use all of Plan B’s max unless the primary plan runs out of money early in the year.

Think of it like a safety net. The secondary plan is there to catch the overflow, not to double your spending power on small fillings.

The “Dreaded” Deductible Problem

You cannot escape deductibles.

When you have two plans, you usually have to pay both deductibles before either plan pays.

-

Plan A deductible: $50

-

Plan B deductible: $50

-

Total out of pocket before insurance pays: $100

However, some secondary plans will waive their deductible if the primary plan already paid their share. Read your fine print.

How to File a Claim with Two Insurances

Most patients do not need to do anything manually. Your dentist’s office handles this, but they need your help.

Step-by-step for you (the patient):

-

Inform your dentist you have two plans. Do not hide it.

-

Provide both insurance ID cards at your first visit.

-

Tell the receptionist which plan is primary. If you don’t know, they can help you figure it out using the “birthday rule” or “employee rule.”

-

Wait. The dentist will submit to Plan A first. Once Plan A pays, they submit the remaining bill to Plan B automatically.

What you should never do:

-

Never submit the claim yourself to Plan B without the dentist’s Explanation of Benefits (EOB) from Plan A. You will get rejected.

-

Never pay the full bill upfront assuming double insurance will reimburse you later. Ask the dentist to wait for both insurances.

The “Non-Covered Service” Trap

What if Plan A says, “We don’t cover implants. Only bridges.”

Can Plan B cover the implant?

Yes, sometimes. If Plan B explicitly covers implants, they can pay as the primary for that specific service (since Plan A pays $0). But again, they will only pay up to their usual fee.

Example:

-

Implant cost: $2,000

-

Plan A: $0 (not covered)

-

Plan B: $1,200 (60% coverage)

-

You pay: $800.

Double coverage saved you $1,200 compared to having no secondary plan.

Realistic Savings Examples (With Numbers)

Let’s look at three real patients to see how this works in practice.

Case 1: Maria (Two fillings)

-

Bill: $300

-

Plan A (Primary): Covers 80% ($240)

-

Plan B (Secondary, Non-duplication): Usually covers 80% ($240). Since Plan A paid $240, Plan B pays $0.

-

Maria pays: $60

Case 2: John (Crown + Root Canal)

-

Bill: $1,800

-

Plan A (Primary): Covers 50% ($900). Annual max is $1,000 (remaining $100 left).

-

Plan B (Secondary): Covers 50% ($900) but has non-duplication. Since Plan A paid $900, Plan B compares. Plan B’s usual benefit is $900. They pay $0 because the primary already paid the equivalent of 50%.

-

John pays: $900. (No real help here because Plan A’s percentage was high).

Case 3: Linda (Braces – $5,000)

-

Plan A: Covers 50% up to $1,500 max.

-

Plan B: Covers 50% up to $1,500 max (Maintenance of benefits – generous plan).

-

Plan A pays: $1,500

-

Plan B pays: $1,500 (remaining balance up to their max)

-

Linda pays: $2,000 (instead of $3,500 with only Plan A).

Is It Worth Paying for Two Dental Plans?

This is the million-dollar question.

When it IS worth it:

-

Your spouse’s plan is free or very cheap ($10/month).

-

You need orthodontics (braces) for yourself or a child.

-

You have poor dental health (need crowns, bridges, or implants).

-

Your primary plan has a very low annual max ($1,000 or less).

When it is NOT worth it:

-

You pay full price for the secondary plan (e.g., $80+/month).

-

You have perfect teeth and only need two cleanings per year.

-

Your secondary plan has a strict “non-duplication of benefits” clause and your primary plan already has good coverage (80%+).

-

The secondary plan’s deductible + premium costs more than the potential savings.

A hard truth from a former insurance agent: For a healthy adult with no major dental work planned, paying for a second dental plan usually costs you more money than you save. You are better off putting that premium money into a Health Savings Account (HSA) or a simple savings account for dental emergencies.

Common Myths About Double Dental Insurance

Let’s clean up some bad information floating around the internet.

Myth 1: “I can get my filling done twice and get paid twice.”

Reality: Fraud. Jail time. Do not do this. The dentist only does the work once.

Myth 2: “The secondary plan will always cover my deductible.”

Reality: Only if the secondary plan has a “maintenance of benefits” clause, which is rare today.

Myth 3: “I don’t need to tell my dentist about the second plan.”

Reality: You must. If you don’t, the dentist will only bill one plan. You will lose money, and the secondary plan will retroactively deny the claim for “failure to coordinate.”

Myth 4: “Dual coverage doubles my in-network discounts.”

Reality: No. You get the discount from the primary plan’s network. The secondary plan will honor that discounted rate, but you don’t get an extra discount.

How to Check If Your Secondary Plan is Useful

Before you get excited, do this simple test.

Call the customer service number on your secondary dental insurance card. Ask them one question:

“Does my plan have a ‘Non-duplication of benefits’ clause for coordination of benefits?”

-

If they say Yes (most common): Your secondary plan will likely pay $0 for routine care (fillings, cleanings). It will only help if your primary plan has a very low annual maximum or doesn’t cover a specific service.

-

If they say No or “Maintenance of benefits”: Keep this plan. It is valuable.

What About Medicare and Double Dental?

Medicare (Part A & B) does not cover routine dental care (cleanings, fillings, dentures) in the United States.

If you have Medicare and a separate private dental plan, you do not have “double dental coverage.” You just have one dental plan (the private one). Medicare is irrelevant for teeth.

The only exception is if you have a Medicare Advantage Plan (Part C) that includes dental benefits. In that case, the Medicare Advantage plan is your primary dental plan. Your private employer plan would be secondary.

How to Cancel a Secondary Plan Without Penalty

If you realize double coverage is costing you money, here is how to cancel.

-

Check your enrollment window. Employer plans usually only let you cancel during Open Enrollment (October–December) or after a “Qualifying Life Event” (QLE).

-

Qualifying Life Events include: Getting married, divorced, having a baby, losing other coverage, or your spouse changing jobs.

-

If you have no QLE, you may have to wait until the next open enrollment. Read your contract carefully.

Pro tip: If you are paying for a secondary plan that is useless, drop it. Put that $50/month into a “dental sinking fund.” After one year, you have $600 cash to spend on any dentist you want, without insurance paperwork.

State-by-State Differences (Briefly)

Most COB rules follow a national standard, but a few states have unique laws regarding dual coverage for children of divorced parents.

-

Texas & California: The “Birthday Rule” is strictly enforced for children, even in divorce cases unless a court order specifies otherwise.

-

New York: Some group plans prohibit coordination entirely. Read your “out-of-state” rider.

-

Florida: The “Parent with custody” rule always overrides the birthday rule.

Unless you live in one of these states, assume the national standard applies.

Step-by-Step Action Plan for You

Here is your practical checklist to handle double dental insurance today.

Step 1: Gather your cards

Take photos of the front and back of both insurance cards.

Step 2: Call your dentist’s billing office

Say: “Hi, I have dual coverage. My primary is [Company A]. My secondary is [Company B]. Can you verify my benefits before my next appointment?”

Step 3: Ask for a “Predetermination”

For any work over $300 (crowns, root canals, surgery), ask your dentist to send a predetermination to both insurances.

-

This is a free estimate.

-

It tells you exactly how much each plan will pay.

-

It takes 2–4 weeks, but it saves you from surprise bills.

Step 4: Compare your out-of-pocket cost

If the predetermination shows you only save $50 by having the second plan, cancel it. If it saves you $500, keep it.

Step 5: Track your annual maximums

Keep a simple note on your phone:

-

Plan A used: $450 of $1,500

-

Plan B used: $0 of $1,000

Frequently Asked Questions (FAQ)

Q1: Can I have double dental insurance from the same company?

Yes. You can have two plans from Cigna or Delta Dental (one from your job, one from your spouse). They will still coordinate benefits. They do not combine into one super-plan.

Q2: Will my premiums double?

No. You pay premiums separately for each plan. The cost of the secondary plan is whatever your employer (or spouse’s employer) deducts from payroll.

Q3: What happens if both plans say they are secondary?

This happens rarely, but it’s called a “contradiction.” The insurance companies will follow the “Birthday Rule” or “Gender Rule” (older standard). In practice, your dentist’s office will call both and force a resolution.

Q4: Can I use double coverage for cosmetic dentistry (veneers, whitening)?

No. Most plans exclude cosmetic dentistry entirely. If both plans exclude it, you pay 100%. If one plan covers it (rare), the secondary will still follow non-duplication rules.

Q5: Does double coverage work for TMJ treatment (jaw pain)?

Sometimes. TMJ is a gray area. Many dental plans exclude it, but medical insurance might cover it. You would need to coordinate dental-to-medical, which is much harder than dental-to-dental.

Q6: I am a veteran. Can I double up VA dental benefits with private insurance?

Yes, but the VA is not “insurance.” The VA is a healthcare provider. If you use a VA dentist, they will not bill your private insurance unless you ask them to. You can get treatment at the VA (free) and also keep your private plan for other dentists. This is a good strategy.

Q7: My dentist says they don’t accept my secondary insurance. What now?

The secondary insurance does not need to be “in-network” to pay. They will still process the claim at the out-of-network rate (usually 10–20% lower). You can still submit the claim yourself using a paper form. Ask your secondary insurer for a “Patient Claim Form.”

Conclusion: The Three-Line Summary

You can have double dental insurance, but it will not double your benefits or let you get two cleanings per year. Instead, the two plans work together through Coordination of Benefits, where the secondary plan only covers leftover costs after the primary pays, often resulting in $0 extra for small procedures. Double coverage is most valuable for expensive work like crowns, braces, or oral surgery, but you should always check for a “non-duplication” clause before paying for a second plan.