Dental Insurance Coverage in Roseville: Your Complete Guide to a Healthy Smile

- On

- InDENTAL COVERAGE

Finding the right dental insurance can feel a bit like navigating a maze. You know you need it, but understanding the fine print, the costs, and what actually gets covered is often the hardest part. If you live in Roseville, you have access to a wide variety of plans and providers, but the key to saving money and keeping your smile healthy is knowing how to choose the right coverage for your unique needs.

Whether you are new to the area, self-employed, or simply tired of your current plan, this guide is designed to help you understand the ins and outs of dental insurance in our community. We will look at how insurance works, what to expect from local dentists, and how to avoid common pitfalls that can leave you with unexpected bills.

Table of Contents

ToggleUnderstanding the Basics of Dental Plans

Before we dive into the specifics of Roseville providers, it is helpful to look at the general structure of dental insurance. Unlike medical insurance, dental coverage focuses heavily on prevention. Most plans operate on a model that encourages you to visit the dentist regularly.

The 100-80-50 Structure

Most traditional dental insurance plans follow a standard structure often referred to as the “100-80-50” rule. This is the backbone of how your benefits are distributed:

-

Preventive Care (Usually 100% covered): This includes routine cleanings, exams, X-rays, and fluoride treatments. Insurance companies cover this fully because it is cheaper to prevent cavities than to fix them.

-

Basic Procedures (Usually 80% covered): This category typically includes fillings, simple extractions, and sometimes periodontal (gum) treatments. You are usually responsible for the remaining 20% as a co-pay or coinsurance.

-

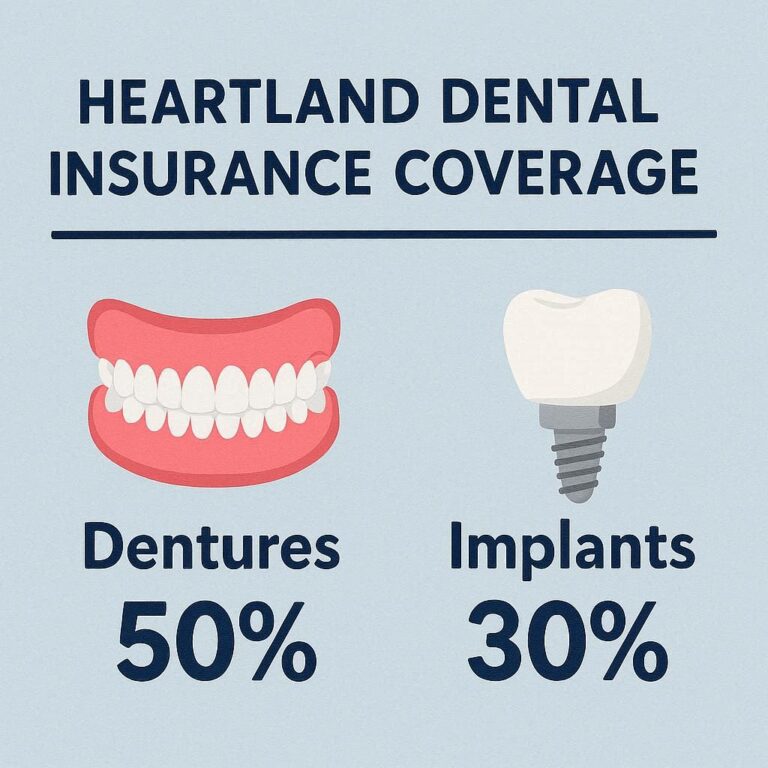

Major Procedures (Usually 50% covered): This includes crowns, bridges, dentures, and implants. These are the most expensive services, and insurance typically pays half, leaving you to cover the rest.

Annual Maximums and Deductibles

It is crucial to understand the concept of the annual maximum. This is the cap on what your insurance company will pay in a single calendar year. In Roseville, as in the rest of the country, the average annual maximum ranges from $1,000 to $2,000 per person.

If you need a crown that costs $1,200 and your plan covers 50% of major work, the insurance pays $600. If you have already used $500 of your annual maximum on fillings earlier in the year, you may run out of coverage for the year.

Additionally, most plans have a deductible. This is a small amount you must pay out-of-pocket before the insurance kicks in. For dental plans, this is usually between $50 and $100 per person.

Types of Dental Insurance Plans Available in Roseville

When searching for coverage in Roseville, you will encounter several types of plans. Each has its own advantages and disadvantages depending on your lifestyle and dental health.

Preferred Provider Organization (PPO)

PPO plans are the most common type of dental insurance in Roseville. They offer a network of dentists who have agreed to provide services at discounted rates.

Pros:

-

Flexibility: You can see any dentist, but you save the most by staying in-network.

-

No referrals needed: You do not need a referral to see a specialist.

-

Predictable costs: Co-pays and coinsurance rates are clearly defined.

Cons:

-

Higher premiums: Generally more expensive than HMO plans.

-

Annual maximums: You are still limited by the cap on what the insurance pays.

Health Maintenance Organization (HMO) or Dental Managed Care

HMO plans usually have lower monthly premiums and no annual maximums. Instead, you pay a set co-pay for each service.

Pros:

-

Low premiums: Often the cheapest option for monthly costs.

-

No annual maximum: You can get significant work done without worrying about hitting a cap.

Cons:

-

Limited network: You must choose a primary care dentist from a specific list. If your favorite Roseville dentist is not on the list, you may have to switch.

-

Pre-authorization: Many services require approval before they can be performed.

Discount or Referral Plans

These are not technically insurance. They are membership plans where you pay an annual fee to receive discounted rates from participating dentists.

Pros:

-

No waiting periods: You can use the discount immediately.

-

No annual limits: You pay for what you get at a reduced rate.

Cons:

-

Not insurance: You still pay the full cost of treatment, just at a discount.

-

Limited savings: The discount percentage varies widely by provider.

Indemnity Plans

These are traditional “fee-for-service” plans. You pay the dentist upfront and then submit a claim to the insurance company for reimbursement.

Pros:

-

Freedom of choice: You can see any dentist in Roseville.

-

No networks: You are never “out-of-network.”

Cons:

-

Paperwork: You are responsible for filing claims.

-

Higher out-of-pocket costs: You must pay upfront and wait for reimbursement.

Navigating Dental Insurance in Roseville: Local Considerations

Roseville is a vibrant community with a high concentration of dental professionals. This competition is generally good for consumers, as it keeps pricing competitive. However, it also means you need to be diligent about understanding network status.

In-Network vs. Out-of-Network

One of the biggest sources of confusion for patients in Roseville is the difference between in-network and out-of-network providers.

If you choose a dentist who is “in-network” with your PPO plan, they have signed a contract with your insurance company. They agree to accept a specific fee schedule. This means your out-of-pocket costs are predictable and usually lower.

If you choose an “out-of-network” dentist, they have not signed that agreement. They can charge their standard fees. Your insurance will still pay a portion, but it will be based on what they deem “usual and customary” rates. If the dentist charges $1,500 for a crown and the insurance says the usual rate is $1,000, you are responsible for the $500 difference plus your standard co-pay.

Important Note for Roseville Residents: Always verify with both the dental office and your insurance company that the provider is in-network. Don’t rely solely on the insurance company’s online directory, as these are sometimes outdated. A quick phone call can save you hundreds of dollars.

Waiting Periods

Many dental plans in Roseville impose waiting periods for basic and major services. A waiting period is the time you must be enrolled in the plan before the insurance will cover certain procedures.

-

No waiting period: Usually for preventive care (cleanings, exams).

-

3 to 6 months: Often for basic procedures like fillings.

-

12 to 18 months: Commonly for major procedures like crowns, bridges, and implants.

If you are moving to Roseville and need immediate work done, look for plans that waive waiting periods. Some employers offer plans with no waiting periods as a perk.

How to Choose the Right Plan for Your Family

Choosing the right dental insurance in Roseville depends entirely on your personal circumstances. A single person with healthy teeth has different needs than a family with children or a retiree needing restorative work.

For Individuals and Couples

If you have good oral health and simply need coverage for twice-yearly cleanings and the occasional filling, a low-premium PPO or HMO plan might be ideal. Focus on plans that cover preventive care at 100% with no waiting period.

Calculate the total cost of the premiums versus the cost of paying out-of-pocket for cleanings. Sometimes, paying cash for preventive care and self-insuring for emergencies can be cheaper than paying monthly premiums.

For Families

When covering a family in Roseville, consider orthodontic coverage. If your children are approaching the age where they might need braces, look for a plan that includes orthodontics. However, be aware that orthodontic coverage usually has a separate lifetime maximum (often $1,000 to $1,500) that is separate from the annual maximum.

Families should also consider the network size. Having a wide network ensures that if one dentist is booked, you have alternatives.

For Seniors and Retirees

If you are on Medicare, it is important to know that original Medicare does not cover routine dental care. Many seniors in Roseville opt for a Medicare Advantage plan that includes dental benefits, or they purchase a standalone dental plan.

Seniors often require more complex restorative work, such as crowns, dentures, or implants. For this demographic, focusing on plans with a higher annual maximum ($2,000 or more) and shorter waiting periods for major services is a smart strategy.

Understanding Coverage for Common Procedures

To make this more practical, let’s look at how insurance typically handles the most common dental procedures in Roseville.

| Procedure | Category | Typical Insurance Coverage | Patient Responsibility |

|---|---|---|---|

| Routine Cleaning | Preventive | 100% | $0 (if in-network) |

| Full Mouth X-rays | Preventive | 100% | $0 (if in-network) |

| Composite Filling | Basic | 80% | 20% + Deductible |

| Simple Extraction | Basic | 80% | 20% + Deductible |

| Root Canal (Molar) | Major | 50% | 50% + Deductible |

| Porcelain Crown | Major | 50% | 50% + Deductible |

| Implant | Major | 50% (often limited) | 50% + High out-of-pocket |

| Orthodontics | Specialty | 50% (Lifetime Max) | 50% up to lifetime max |

The Reality of Implant Coverage

One area where patients in Roseville are often surprised is dental implant coverage. Many plans technically cover implants under “major services,” but they often have a low annual maximum. Since a single implant can cost between $3,000 and $5,000, and insurance only pays up to $1,500 or $2,000 per year, the patient ends up covering the majority of the cost.

Furthermore, some plans separate the procedure into three parts (the implant fixture, the abutment, and the crown) and apply the deductible to each part separately. Always ask your dentist’s billing coordinator to verify coverage before proceeding with implants.

Maximizing Your Dental Benefits

If you already have dental insurance, or are about to sign up, you want to make sure you are getting the most value for your money. Here are practical tips tailored for residents of Roseville.

Use Your Benefits Before Year-End

Dental insurance operates on a calendar year for most plans. The annual maximum does not roll over. If you do not use it by December 31st, you lose it.

If you have been putting off a filling or a crown, schedule it before the end of the year. Many dental offices in Roseville get busy in November and December as patients rush to use their remaining benefits, so book your appointment early.

Coordinate Benefits for Couples

If you and your spouse both have dental insurance through your respective employers, you can coordinate benefits. This is called “dual coverage.” You do not get double the benefits, but you can often reduce your out-of-pocket costs significantly.

For example, if your plan pays 50% for a crown and your spouse’s plan pays 50% for the same procedure, the two plans together might cover 100% of the cost, minus deductibles. This is a valuable benefit that many families in Roseville overlook.

Don’t Skip Preventive Care

It might be tempting to skip a cleaning to save time or money, but this is a false economy. By using your 100% preventive coverage twice a year, your dentist can catch small issues like cracks or early decay before they turn into root canals or crowns.

Prevention is the only way to truly avoid hitting your annual maximum.

Common Pitfalls and How to Avoid Them

Even with a good plan, misunderstandings can happen. Here are common issues Roseville patients face and how to navigate them.

The “UCR” Trap

When you go out-of-network, insurance companies use “Usual, Customary, and Reasonable” (UCR) fees to determine what they will pay. The problem is that each insurance company defines UCR differently. What the insurance company considers “reasonable” might be far less than what the dentist in Roseville actually charges.

Solution: If you have your heart set on a specific out-of-network dentist, ask the office to provide a “predetermination of benefits.” This is a pre-treatment estimate sent to your insurance company. It gives you a written breakdown of what the insurance will pay and what you owe before the work is done.

The Downgrade Clause

Some insurance plans use a “downgrade clause” for fillings. If you want a tooth-colored composite filling, but the plan’s base coverage is for silver amalgam fillings, they will only pay what they would have paid for the silver. You are responsible for the difference in cost.

Solution: If aesthetics are important to you, look for a plan that explicitly covers composite fillings without downgrading, or be prepared to pay the upgrade cost.

The “Missing Tooth” Clause

This is a critical one for those considering implants or bridges. Many insurance policies have a “missing tooth clause.” If you lost a tooth before the policy became active, the insurance will not cover the replacement of that tooth. They consider it a pre-existing condition.

Solution: If you are switching jobs or moving to Roseville and have missing teeth, check the policy wording carefully. Some group plans waive this clause, but many individual plans enforce it strictly.

The Future of Dental Benefits in Roseville

The landscape of dental insurance is slowly changing. With the rise of group purchasing organizations and a growing awareness of the link between oral health and systemic health (like heart disease and diabetes), employers in the Roseville area are starting to offer more robust plans.

There is also a growing trend toward “transparent pricing.” Some dental offices in Roseville are beginning to offer in-house membership plans. These are excellent for the uninsured or underinsured. For a flat annual fee (often between $200 and $400 for an individual), you receive two cleanings, exams, and X-rays, plus a discount (often 10-20%) on any additional work. This is not insurance, but for many freelancers and small business owners in Roseville, it is a predictable and affordable alternative.

A Comparative Look at Plan Types

To help you visualize the differences, here is a comparison table based on typical plans available to Roseville residents.

| Feature | PPO Plan | HMO Plan | Discount Plan | In-House Membership |

|---|---|---|---|---|

| Monthly Cost | High | Low | Low (Annual fee) | N/A (Annual fee) |

| Network | Large, flexible | Very restrictive | Varies | Single dental office |

| Annual Max | $1,000 – $2,000 | None | None | None |

| Preventive Care | 100% covered | Low co-pay ($5-$15) | 20-30% off | Included in fee |

| Major Work | 50% covered | Low co-pay ($200-$400) | 20-30% off | 10-20% off |

| Best For | Predictable needs | Low monthly budget | No insurance available | Loyalty to one dentist |

Questions to Ask Before You Sign Up

Before you enroll in a dental plan in Roseville, arm yourself with these questions. Asking them upfront will save you from surprises later.

-

“Is this a PPO, HMO, or Indemnity plan?” Know what type of network you are buying into.

-

“What is the annual maximum per person?” This is the single most important number for budgeting.

-

“Are there waiting periods for fillings, crowns, or implants?” If you need work soon, this is a deal-breaker.

-

“Is Dr. [Your Preferred Dentist] in-network?” Don’t assume; verify.

-

“What is the deductible, and does it apply to preventive care?” Some plans waive the deductible for cleanings.

-

“Does the plan cover orthodontics for adults/children?” If braces are in your future, this is essential.

-

“Are implants covered as a major service, or are they excluded?” Many plans are updating this, but it varies widely.

How Roseville Dentists Work with Insurance

Dental offices in Roseville are accustomed to working with a variety of insurance carriers. The most commonly accepted carriers in the area include Delta Dental, Cigna, MetLife, Aetna, and Guardian.

Most dental offices have dedicated billing coordinators whose job is to help you understand your coverage. Do not hesitate to ask them for a breakdown of costs before you agree to treatment. A reputable office will always provide a treatment plan with estimated insurance payments and patient portions in writing.

If you are a new patient, bring your insurance card to your first appointment. The office will typically verify your benefits and let you know what is covered before they proceed with any treatment beyond the initial exam and cleaning.

Conclusion

Navigating dental insurance coverage in Roseville requires a balance of understanding the technical details of your policy and knowing the local dental landscape. By familiarizing yourself with terms like annual maximums, waiting periods, and in-network vs. out-of-network costs, you empower yourself to make decisions that protect both your oral health and your wallet.

Remember that the best plan is not always the one with the lowest monthly premium, but the one that aligns with your dental health needs, whether that is simple preventive care for a young family or comprehensive restorative coverage for a retiree. Take the time to review your options during open enrollment, communicate openly with your local dental office, and use your benefits before they expire to maintain a healthy, confident smile.

Frequently Asked Questions (FAQ)

1. Does dental insurance in Roseville cover cosmetic dentistry like veneers or teeth whitening?

Generally, no. Most standard dental insurance plans do not cover purely cosmetic procedures. If a procedure is deemed medically necessary (for example, a crown that also improves appearance), the structural portion may be covered, but the cosmetic component usually is not.

2. Can I see any dentist in Roseville if I have a PPO plan?

Yes, you can. However, to get the maximum benefit and lowest out-of-pocket cost, you should see a dentist who is in-network. If you go out-of-network, your benefits will likely be reduced, and you may be responsible for balance billing.

3. What happens if I hit my annual maximum?

Once you reach your annual maximum, your insurance will stop paying for covered services for the remainder of the calendar year. You will be responsible for 100% of the cost of any additional treatment until your benefits reset, usually on January 1st.

4. Is orthodontic coverage for braces usually included?

Orthodontic coverage is often an optional add-on or a feature of more comprehensive plans. It typically has a separate lifetime maximum (e.g., $1,500) rather than an annual one. Always check if the plan covers child orthodontics, adult orthodontics, or both.

5. How do I know if a dentist in Roseville is accepting new patients with my insurance?

The best way is to call the dental office directly. While insurance directories can give you a list, they do not always reflect whether a practice is currently accepting new patients. A quick phone call to the office can confirm network status and availability.

Additional Resource

For more detailed information on comparing health and dental plans during open enrollment, you can visit the official California Department of Insurance website. They offer consumer guides that explain your rights and how to file complaints if you encounter issues with a dental insurer.

[Link to resource placeholder: www.insurance.ca.gov]

Note: This article is for informational purposes only and does not constitute legal or financial advice. Dental insurance plans, networks, and benefits change frequently. Always verify coverage details directly with your insurance provider and dental care provider before undergoing treatment.

dentalecostsmile

Newsletter Updates

Enter your email address below and subscribe to our newsletter