Does Medical Insurance Cover Dental Implants?

Let’s be honest: when you hear the words “dental implant,” your mind probably goes straight to the cost. You are not alone. It is one of the most significant investments in oral health a person can make. The question that almost every patient asks is simple: will my insurance help?

If you are hoping to use your dental plan, you might be in for a disappointment. Most standard dental insurance plans categorize implants as a cosmetic or major restorative procedure, often covering only a fraction—or nothing at all.

But here is the detail most people overlook: your medical insurance might actually be the key.

While it is not a guarantee, there are specific medical scenarios where a dental implant stops being just a tooth replacement and starts being a medical necessity. When that happens, your medical benefits can sometimes step in to cover a portion of the treatment.

This guide is designed to help you understand exactly how that works. We will explore the fine line between dental and medical coverage, the specific conditions that qualify, and how to build a strategy to make this life-changing procedure more affordable.

Understanding the Dental vs. Medical Insurance Divide

To understand why medical insurance sometimes covers dental implants, you first have to understand the strange separation between our teeth and the rest of our bodies. In the world of insurance, your mouth is often treated like a separate entity.

Why Dental and Medical Insurance Are Separate

Historically, dental care and medical care evolved along different paths. Medical insurance was designed to cover illness, injury, and surgery. Dental insurance was designed as a preventive, maintenance-based benefit—think cleanings, fillings, and extractions.

This split means that dental insurance usually has a low annual maximum (often between $1,000 and $2,000). Medical insurance, on the other hand, has high deductibles but much higher coverage limits.

The key to bridging this gap is medical necessity. If a dentist or oral surgeon can prove that a dental implant is not merely for chewing or aesthetics, but is medically required to treat a disease, injury, or congenital defect, the medical side of your insurance may open its doors.

When a Tooth Becomes a Medical Issue

Your teeth are technically part of your body. So, when does a missing tooth turn into a medical problem? It usually happens when the tooth loss is caused by something beyond standard decay or gum disease, or when the lack of a tooth creates a broader health risk.

Here are the common scenarios where medical coverage becomes a possibility:

-

Trauma or Accidents: If you lose a tooth in a car accident, a fall, or a sports injury, your medical insurance (often under the accident benefits) may cover the reconstruction, including implants.

-

Pathology: If a tumor or cyst is removed from your jaw, leaving a void that requires a dental implant to restore structure, this falls under medical necessity.

-

Congenital Defects: Conditions like ectodermal dysplasia, where teeth never form, or cleft palate, are often covered by medical insurance because they are present from birth and require surgical intervention.

-

Radiation or Cancer Treatment: Patients who undergo radiation therapy for head or neck cancer (specifically osteoradionecrosis) or those who have had jaw reconstruction following cancer removal often qualify for medically necessary implants.

Dental Implants Medical Insurance Coverage: What Qualifies?

Let’s dive deeper into the specific clinical situations where your medical insurance is most likely to provide coverage. It is important to remember that “likely” does not mean “automatic.” You will need to fight for it with documentation.

Congenital Abnormalities and Developmental Defects

If you or your child were born with a condition that affects the development of teeth or the jaw, medical insurance typically views this as a structural issue, not just a dental one.

Ectodermal Dysplasia is a prime example. Individuals with this condition are missing teeth (hypodontia or anodontia). Because they never developed permanent teeth, dental implants are not cosmetic; they are essential for jawbone preservation, nutrition, and speech development. Medical insurers often cover these implants under pediatric or reconstructive surgery benefits.

Similarly, cleft lip and palate repair often involves bone grafting and dental implants to fill the gaps in the dental arch. This is considered part of the overall reconstructive surgical plan.

Accidents and Traumatic Injuries

If you are in an accident, the emergency room visit, X-rays, and initial surgery to stabilize the jaw are covered by your medical insurance. But what about the implant to replace the tooth that was knocked out?

If the injury is acute and the tooth loss is a direct result of a covered accident, you may have a strong case. You will need to ensure the claim is coded correctly. Instead of using a standard dental code (D6010 for implant placement), the surgeon needs to use medical codes (CPT codes) that describe the surgical procedure.

Important Note: If the accident was due to a car crash, your auto insurance (MedPay or PIP) might be the primary payer before your health insurance kicks in.

Jaw Reconstruction and Orthognathic Surgery

Sometimes, the issue is not the teeth themselves but the jaw structure. Patients undergoing orthognathic surgery (corrective jaw surgery) often require dental implants to complete the restoration.

If you are having your jaw surgically broken and repositioned to correct a malocclusion, sleep apnea, or TMJ disorders, the entire surgical package—including the implants placed to anchor new teeth—can sometimes be bundled under medical coverage. The key is that the primary reason for the surgery is functional (breathing, eating, pain relief), with the implants being a necessary part of that functional restoration.

Post-Oncology Reconstruction

This is perhaps the most straightforward path to medical coverage. If you have been diagnosed with oral cancer or head and neck cancer, and your treatment involves:

-

Mandibular resection: Removing part of the jawbone.

-

Radiation therapy: Which can damage the jawbone and make standard dentures impossible (due to osteoradionecrosis risk).

In these cases, dental implants are often covered as part of the reconstructive surgery following cancer treatment. The goal is to restore the ability to eat and speak, which are core medical functions.

The Role of the Oral Surgeon in Getting Coverage

If you want to use medical insurance for dental implants, your choice of provider matters immensely. A general dentist may not be equipped to bill medical insurance. However, an oral surgeon or a maxillofacial prosthodontist is a medical specialist.

These specialists have National Provider Identifier (NPI) numbers and are accustomed to billing major medical plans (Blue Cross Blue Shield, Cigna, Aetna, UnitedHealthcare, etc.) for complex procedures.

The Power of Proper Coding

The difference between a denied claim and an approved claim often comes down to a single code.

-

Dental Codes (CDT): Used by dentists. These are for “teeth.” When insurers see D6010, they often route it to the dental benefit plan.

-

Medical Codes (CPT): Used by surgeons. Codes like CPT 21044 (excision of tumor, mandible) or CPT 21193 (reconstruction of mandible) are processed by medical insurance.

If your surgeon uses a CPT code that describes the surgical reconstruction of the jaw rather than the placement of a tooth, it is much more likely to be considered a medical necessity.

Pre-Determination: Your Best Friend

Never go into an implant procedure assuming coverage. Before the surgery, ask your surgeon’s office to send a pre-determination of benefits (also called a pre-authorization) to your medical insurance.

This is a formal request where the surgeon submits the treatment plan, X-rays, and a letter of medical necessity to the insurance company. The insurer then tells you—in writing—what they will pay. This document protects you from surprise bills.

Step-by-Step Guide to Checking Your Coverage

Navigating insurance jargon can feel like reading a foreign language. Here is a step-by-step process to demystify it.

Step 1: Identify Your Insurance Type

Look at your insurance card. Do you have a PPO, HMO, EPO, or POS?

-

PPO (Preferred Provider Organization): Usually offers the most flexibility. You can see an out-of-network specialist (like an oral surgeon) and still get partial coverage.

-

HMO (Health Maintenance Organization): Strict networks. You will likely need a referral from a primary care physician (PCP) to see a specialist. Coverage is limited to in-network providers.

-

Medicare/Medicaid: Rules vary drastically by state and plan. Traditional Medicare does not cover dental implants for routine tooth loss, but may cover them if they are part of a covered surgical procedure (like jaw reconstruction after cancer). Medicare Advantage plans (Part C) sometimes offer dental benefits, but medical necessity still trumps the dental cap.

Step 2: Read Your Summary of Benefits

Find your policy’s “Exclusions” section.

Look for language regarding “dental services” or “oral surgery.”

-

Good sign: “Coverage for medically necessary oral surgery.” This is your door.

-

Red flag: “Exclusion of all dental implants regardless of medical necessity.” Some policies explicitly exclude implants. If this is the case, appealing will be very difficult.

Step 3: Ask the Right Questions

When you call your insurance provider, do not ask, “Do you cover implants?” The customer service rep will likely say no. Instead, ask these specific questions:

-

“Under my medical plan, what are the criteria for medically necessary oral surgery?”

-

“Does my plan cover reconstructive surgery of the jaw following trauma or pathology?”

-

“If I need a bone graft or implant to restore function after a covered surgery, is that considered part of the surgical benefit?”

Step 4: Gather Documentation

If you are pursuing medical necessity, you need evidence. Your surgeon should provide:

-

Radiographic evidence: CT scans or panoramic X-rays showing bone loss or defect.

-

Letter of Medical Necessity: A formal letter stating why the implant is required to restore mastication (chewing), speech, or to prevent further medical deterioration (e.g., bone atrophy, inability to wear dentures due to gag reflex or cancer history).

Alternative Strategies: Making Implants Affordable

If your medical insurance denies coverage, or if your case does not fit the “medical necessity” criteria, do not despair. There are still ways to make implants manageable without draining your savings.

1. Dental Insurance with Implant Riders

While standard dental insurance has low caps, some plans (particularly PPOs) offer “implant riders” or major medical coverage within the dental plan. If you have the flexibility to choose a plan during open enrollment, look for one with:

-

No waiting period for major services.

-

An annual maximum higher than $2,000 (some premium plans go up to $5,000 or unlimited).

-

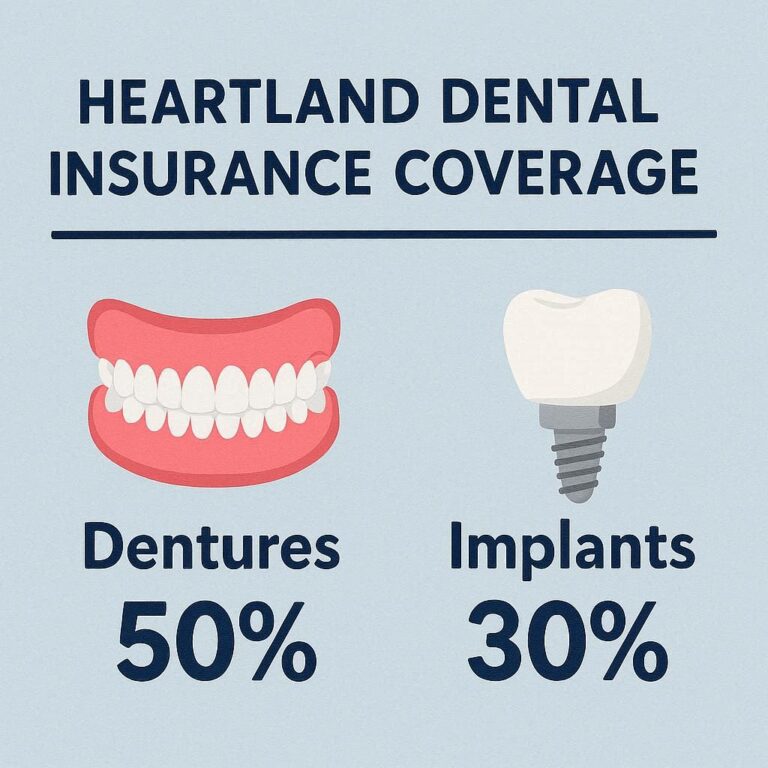

Coverage for implants listed specifically in the policy (usually 50% coverage after deductible).

2. Health Savings Account (HSA) or Flexible Spending Account (FSA)

Even if insurance does not pay, you can pay with pre-tax dollars.

-

HSA: If you have a high-deductible health plan (HDHP), you can contribute pre-tax money. This effectively gives you a 20-30% discount on the procedure because you avoid paying income tax on the money used.

-

FSA: Use it or lose it. If you know you are getting implants this year, fund your FSA to the maximum to save on taxes.

3. In-House Membership Plans

Many dental practices are moving away from traditional insurance and offering in-house membership plans. For a flat annual fee (usually $200–$400), you get free exams, X-rays, and a significant discount (often 10-20%) on major procedures like implants. This is often a better deal than paying for high-premium dental insurance that barely covers implants.

4. Dental Schools

If you live near a major university with a dental school or residency program (especially in prosthodontics or periodontics), you can receive implant treatment for roughly 50% less than private practice. The trade-off is time—appointments are longer because students work under the supervision of experienced faculty—but the quality is often exceptional.

5. Charitable Organizations and Grants

For specific cases (cancer survivors, congenital defects, veterans), there are organizations that provide grants or low-cost care:

-

Dental Lifeline Network: Connects vulnerable individuals (elderly, disabled, medically fragile) with volunteer dentists.

-

American Academy of Implant Dentistry (AAID) Foundation: Occasionally offers grants for patients in need.

-

VA Benefits: Veterans with service-connected injuries may have dental implants covered by the VA if the tooth loss is related to their service.

Comparing Your Payment Options

To help you visualize the financial landscape, here is a comparison of how different funding sources stack up when facing a typical $5,000 implant crown procedure.

| Payment Method | Pros | Cons | Best For |

|---|---|---|---|

| Medical Insurance | Covers high costs if medically necessary. | Strict criteria; requires pre-auth; may exclude implants outright. | Patients with trauma, cancer, or congenital defects. |

| Dental Insurance | Helps with exam/X-ray costs. | Low annual max ($1k-$2k); often excludes implant/crown. | Routine maintenance; not ideal for major work. |

| HSA/FSA | Tax savings (20-30% off). | Requires account setup; FSA funds expire annually. | Anyone paying out-of-pocket. |

| In-House Plan | Immediate discounts; no deductibles. | Limited to one practice; non-refundable fee. | Patients loyal to one dentist; predictable savings. |

| CareCredit (Financing) | 0% interest promotional periods. | High interest if not paid off in time. | Those who can pay within 12-24 months. |

| Dental School | 30-50% cheaper than private practice. | Longer wait times; multiple appointments. | Flexible schedules; budget-focused patients. |

Common Myths About Implant Coverage

Let’s clear up a few misconceptions that often lead patients down the wrong path.

Myth 1: “If I have a Medicare Advantage plan, my implants are free.”

Reality: Medicare Advantage plans (Part C) often include some dental coverage, but they rarely cover the entire implant procedure. They typically have a hard cap on dental spending (e.g., $1,500 per year). Since a single implant can cost $3,000 to $6,000, you will still have a significant out-of-pocket portion.

Myth 2: “My medical insurance denied it, so I have to pay full price.”

Reality: A denial letter is not the end. It is the beginning of an appeal. Many claims are denied automatically by algorithm. If your surgeon submits a detailed appeal with the letter of medical necessity, X-rays, and supporting health history, the decision is often reversed. Do not accept the first “no.”

Myth 3: “Implants are purely cosmetic, so insurance never pays.”

Reality: The medical field defines “cosmetic” as procedures that improve appearance without improving physiological function. If you cannot chew, if your jawbone is deteriorating, or if you have a gap that causes speech impediments or chronic pain, the implant is functional, not cosmetic.

The Fine Print: Exclusions and Limitations

Even when you think you have coverage, there are often hidden limitations.

The “Missing Tooth” Clause

This is a notorious exclusion in many medical insurance policies. The clause states that the plan does not cover the replacement of teeth that were missing before the effective date of the policy, or teeth missing due to dental disease.

If you lost a tooth ten years ago due to gum disease, and you are trying to get medical insurance to pay for an implant today, you will likely hit this exclusion. However, if the tooth was lost recently due to a covered accident (which happened after the policy started), you may be exempt.

Anesthesia and Facility Fees

Sometimes, insurance will deny the implant but cover the anesthesia (if you are going under general anesthesia in a hospital setting) and the facility fees. If you have a complex medical history (heart conditions, severe anxiety) that requires you to have the surgery in a hospital rather than a dental office, the hospital portion is often covered by medical insurance even if the implant is not.

Coordination of Benefits

If you have both dental and medical insurance, and you are attempting a medical claim, your providers must coordinate. The medical insurance may ask, “Does the patient have dental coverage?” They may expect the dental plan to pay first (if it has implant coverage), and then the medical plan pays secondary. If you do not coordinate this correctly, claims can be denied for “failure to coordinate.”

How to Appeal a Denial

If your medical insurance denies your claim for dental implants, you have the right to appeal. Here is how to structure a winning appeal.

1. Understand Why It Was Denied

Look at the Explanation of Benefits (EOB). It will have a code:

-

*CO-96:* Not medically necessary. (Most common).

-

*CO-24:* Charges are for a dental service. (They are miscoding).

-

*PR-49:* This is a plan exclusion.

2. Gather a Stronger Case

You need to reframe the narrative. Your appeal letter should not say “I want a tooth to smile.” It should say:

“The patient requires osseointegrated implant placement to restore masticatory function following segmental mandibulectomy (cancer resection). Without surgical restoration of the dental arch, the patient faces nutritional compromise, speech articulation deficits, and continued resorption of the grafted fibula flap, risking structural failure of the previous reconstruction.”

3. Enlist Your Surgeon

Most appeals require a peer-to-peer review. This is where the surgeon (the specialist) calls a medical director at the insurance company (who is also a doctor). A surgeon who does this frequently can speak the medical language necessary to overturn the denial.

4. External Review

If the internal appeal fails, most states allow for an external independent review. An independent third-party medical expert reviews your case. If they rule in your favor, the insurance company is legally bound to pay.

Future Trends: Will Insurance Coverage Improve?

The landscape is slowly shifting. As the population ages and more people retain their natural teeth (or want to retain function), insurance companies are beginning to recognize that implants are often the least expensive long-term solution.

The Cost of Denial

A removable denture might cost $1,500 today, but over 20 years, it leads to bone loss, denture relines, adhesive costs, and potential nutritional issues. An implant-supported denture costs more upfront but has a 95% success rate over decades. Some insurers are starting to do the math.

New Legislation

There are ongoing advocacy efforts to expand Medicare coverage for dental implants for patients with chronic diseases and cancer survivors. While not law yet, the conversation is gaining traction in Washington, D.C.

Employer-Sponsored Plans

Large corporations, like tech companies and manufacturers, are beginning to offer “enhanced dental benefits” that include implants as a standard part of their executive or comprehensive health plans. If you are employed, it is worth checking with your HR department to see if your company offers a “buy-up” plan that includes major restorative coverage.

A Note on Bone Grafting and Medical Insurance

Often, the most expensive part of an implant procedure is not the titanium screw, but the bone graft.

If your jawbone is too thin or soft to support an implant, you need a bone graft. Here is a secret: Bone grafting is easier to get covered by medical insurance than the implant itself.

Why? Because bone grafting (alveolar ridge augmentation) is considered reconstructive surgery. If you are missing bone due to:

-

Trauma (accident)

-

Pathology (cyst removal)

-

Congenital defect

Medical insurance frequently covers the bone graft procedure (CPT codes 21210, 20970, etc.). Even if the implant is ultimately a dental expense, the preparation of the jaw (the graft) is often a medical one.

Conclusion: Knowledge is Your Best Insurance

Navigating the financial side of dental implants requires patience, persistence, and a clear strategy. While the question of dental implants medical insurance coverage does not have a simple yes-or-no answer, the possibilities are far greater than most people assume.

The key is to stop thinking like a dental patient and start thinking like a medical patient. If your need for implants stems from trauma, surgery, congenital conditions, or systemic disease, your path likely leads through medical insurance. If not, leveraging tax-advantaged accounts, in-house dental plans, and specialized financing can make the cost manageable.

Ultimately, a dental implant is an investment in your long-term health, function, and quality of life. By understanding the rules of the game—and knowing how to appeal, code, and choose the right specialist—you can take control of the process and make that investment a reality.

Frequently Asked Questions (FAQ)

1. Can I use my medical insurance for dental implants if I just have one missing tooth from a cavity?

Generally, no. If the tooth loss is due to standard decay or gum disease (which is considered a dental disease), medical insurance will almost always classify this as a dental issue and deny coverage. Your dental insurance, if you have it, would be the primary source, though it will likely only cover a small portion.

2. What is the difference between a dental code and a medical code for implants?

Dental codes (CDT) describe the tooth and are usually sent to dental insurance. Medical codes (CPT) describe the surgical procedure on the jawbone. If an oral surgeon bills using CPT codes (e.g., for jaw reconstruction), the claim goes to your medical insurance, which has a much higher chance of coverage if the surgery is medically necessary.

3. Will Medicare pay for dental implants?

Original Medicare (Parts A and B) does not cover dental implants for routine tooth loss. However, if the implant is part of a covered surgical procedure, such as reconstruction following the removal of a tumor in the jaw (cancer), Part A (hospital insurance) may cover the inpatient surgery costs. Medicare Advantage (Part C) plans often have limited dental benefits that may contribute, but rarely cover the full cost.

4. How do I find an oral surgeon who bills medical insurance?

Look for an “Oral and Maxillofacial Surgeon.” These are dental specialists who are also trained in surgical residency programs. Their offices typically have billing departments that handle both dental and medical insurance claims. When calling, ask directly: “Does your office bill medical insurance for medically necessary implant procedures?”

5. What does a “Letter of Medical Necessity” look like?

It is a formal letter from your surgeon to the insurance company. It must clearly state your diagnosis (e.g., post-traumatic defect, hypodontia), explain the functional impairments (inability to chew, speech issues), describe the proposed surgical plan, and cite relevant medical literature or guidelines that support why an implant—rather than a denture—is the only suitable treatment to restore function.