Heartland Dental Insurance Coverage for Dentures and Implants

If you are reading this, chances are you are trying to solve a puzzle. You know you need dental work—specifically, dentures or implants—and you have insurance through Heartland Dental. Or perhaps you are considering a job at Heartland Dental and want to understand what the employee benefits actually cover.

You are not alone in feeling a little overwhelmed. Dental insurance is often misunderstood. It does not work like medical insurance, and when it comes to major procedures like implants and dentures, the fine print matters a great deal.

This guide is designed to be your friendly, honest companion. We will walk through what “Heartland Dental insurance coverage for dentures implants” really looks like. We will look at the difference between being a patient at a Heartland-supported office versus being an employee of the organization. We will also share realistic ways to save money and avoid surprise bills.

Let us get started with the basics.

What Is Heartland Dental? (Patient vs. Employee Context)

Before we talk about coverage, it is important to clarify a common point of confusion. Heartland Dental is not a single insurance company like Delta Dental or Cigna. Instead, it is one of the largest dental support organizations (DSOs) in the United States.

Heartland Dental as a Support Organization

Heartland Dental provides non-clinical administrative support to hundreds of dental offices across the country. You might walk into a practice with a name like “Smith Family Dentistry” or “Coast Dental,” and that office is supported by Heartland Dental. For the patient sitting in the chair, the insurance they use is usually whatever private plan they have, or a PPO plan accepted by that specific office.

Heartland Dental as an Employer

If you work for Heartland Dental (as a dentist, hygienist, or administrative staff), the company offers a specific employee benefits package. In this context, “Heartland Dental insurance” refers to the group health and dental plans provided to employees.

Because of this dual nature, the answer to “does Heartland Dental cover my implants?” changes depending on whether you are a patient visiting a supported office or a team member using your employee benefits.

We will cover both scenarios in detail.

The Reality of Dental Insurance for Major Procedures

Let us be honest for a moment. Dental insurance was not designed to pay for luxury treatments. It was designed decades ago to encourage basic preventive care. Most standard dental plans operate on the “100-80-50” structure.

-

100% covered for preventive care (cleanings, exams, x-rays).

-

80% covered for basic procedures (fillings, simple extractions).

-

50% covered for major procedures (crowns, bridges, dentures, implants).

This means that even with “good” insurance, you are typically responsible for half the cost of dentures or implants. Some plans have a waiting period—meaning you must be enrolled for 6 to 12 months before the insurance will pay anything toward major services.

Another reality check: annual maximums. Most dental plans cap their payout at $1,000 to $2,000 per year. A single dental implant can cost between $3,000 and $6,000. As you can see, the math forces most patients to pay a significant portion out of pocket, even when coverage is active.

Heartland Dental Insurance for Employees: A Closer Look

If you are a team member at Heartland Dental, you have access to a benefits package that is generally more robust than what the average consumer buys on the open market. Heartland Dental is known for offering competitive benefits to attract top dental professionals.

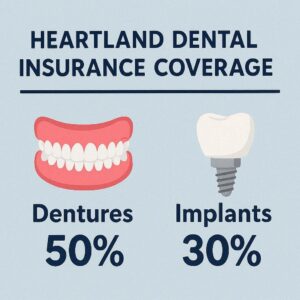

Coverage for Dentures

For employees, denture coverage typically falls under the “major services” category. If you have been with the company for a while and have selected the premium dental plan, the insurance often covers:

-

Complete dentures: Usually covered at 50% after the deductible.

-

Partial dentures: Covered at 50%, though some plans may offer slightly higher coverage if the partial is deemed medically necessary to maintain the integrity of existing teeth.

Many employee plans also offer “in-network” advantages. If you receive treatment at a Heartland-supported office, the fees are usually negotiated down, which saves you money even before the insurance kicks in.

Coverage for Implants

Here is where you need to read your Summary Plan Description (SPD). Historically, many dental plans considered implants “cosmetic” or “non-standard.” However, as implants have become the gold standard for tooth replacement, more employer-sponsored plans are beginning to include them.

In the Heartland Dental employee plan, you may find one of three scenarios:

-

Full Coverage: Implants are covered as a major service at 50%, similar to a bridge or crown.

-

Tiered Coverage: The implant fixture (the screw in the bone) is covered, but the crown (the tooth on top) is covered under a different category.

-

Exclusion: The plan explicitly excludes dental implants, offering a bridge or denture as the only covered options.

Important Note: If you are a Heartland Dental employee, your benefits package is designed to encourage you to seek care within the Heartland network. Usually, this means visiting a supported office near you. Staying in-network maximizes your benefits and minimizes your out-of-pocket costs.

Heartland Dental Supported Offices: Patient Insurance Coverage

Now, let us talk about what happens if you are a patient walking into a Heartland-supported dental office. You likely have insurance through your own employer, the marketplace, or a retirement plan.

When you visit a Heartland-supported office, the office staff acts as a liaison between you and your specific insurance carrier. The coverage is not determined by “Heartland Dental”—it is determined by your specific policy.

How It Works

-

Verification: The front office will verify your benefits before starting treatment.

-

Network Status: Heartland-supported offices are usually in-network with major PPOs (like Aetna, Cigna, Delta Dental, MetLife, etc.).

-

Predetermination: For expensive procedures like implants or dentures, the office will likely send a “predetermination” to your insurance company. This is essentially a pre-claim that tells you exactly what the insurance will pay and what you will owe before the work begins.

Does Being at a Heartland Office Matter?

Yes, for two reasons. First, because Heartland Dental is a large organization, the affiliated offices often have streamlined billing departments. They are very efficient at maximizing insurance benefits. Second, because they are part of a large network, they often have access to in-house discount plans or financing options that smaller private practices might not offer.

Key Terms: Implants vs. Dentures

To understand your coverage, you need to understand the language on your insurance form. Insurance companies often categorize these procedures differently, even though they serve similar purposes.

| Feature | Traditional Dentures | Dental Implants |

|---|---|---|

| Insurance Category | Usually “Major Restorative” | Often “Major Restorative” or sometimes “Surgical/Implants” (a separate category) |

| Typical Coverage | 50% after deductible | 0% to 50% depending on the plan |

| Waiting Period | Often 12 months | Often 12 months; some plans exclude entirely |

| Long-term Value | Requires replacement every 5-10 years | Can last a lifetime with proper care |

| Out-of-Pocket Cost | Lower upfront cost | Higher upfront cost |

What Are Implant-Supported Dentures?

There is also a middle ground called “implant-supported dentures” (or overdentures). These involve placing 2 to 6 implants in the jaw to snap a denture into place.

From an insurance perspective, this is the most complex scenario. The insurance company will look at two separate claims: one for the surgical placement of the implants (surgery) and one for the fabrication of the denture (prosthetics). You need to verify coverage for both components.

Navigating Waiting Periods and Missing Tooth Clauses

Two common pitfalls catch people off guard: waiting periods and the “missing tooth clause.”

Waiting Periods

Most dental insurance plans—especially individual plans or new group plans—have waiting periods for major services.

-

Year 1: Usually only preventive care is covered.

-

Year 2: Basic services (fillings) become covered.

-

Year 3: Major services (dentures/implants) become covered.

If you just started a job or bought a new plan, you might have to wait 12 to 24 months before your insurance pays a cent toward dentures. Heartland Dental offices see this often, and they usually offer alternative payment arrangements to help you start treatment sooner.

The Missing Tooth Clause

This is a tricky one. Some dental insurance policies have a “missing tooth clause.” If you were missing a tooth before your insurance policy began, the insurance company will not pay to replace it.

For example, if you lost a tooth three years ago, and you just started your insurance today, the insurance will consider that a “pre-existing condition” for that specific tooth. They may cover the extraction of a new problem, but not the prosthetic replacement of the old one. Always ask your Heartland-supported office to check for this clause before proceeding.

How to Maximize Your Coverage at a Heartland Dental Office

You have the power to reduce your out-of-pocket costs. Here is a checklist to follow if you are planning for dentures or implants.

-

Ask for a Predetermination: Do not rely on a verbal estimate. Ask the office to send a formal predetermination to your insurance. This comes back on official letterhead and is a binding estimate of what the insurance will pay.

-

Time Your Treatment: If your plan has a $1,500 annual maximum, and you need work that costs $4,000, ask if you can split the treatment over two calendar years. Start the surgery in November, pay half, and finish the crown in January when the benefits reset.

-

Use In-Network Providers: Ensure that the Heartland-supported office you are visiting is a “preferred provider” for your specific insurance. The difference in cost can be 20% to 40% compared to out-of-network.

-

Utilize FSA or HSA Funds: If you have a Flexible Spending Account (FSA) or Health Savings Account (HSA) through your employer, use these tax-free dollars to pay for your portion of the dentures or implants. This saves you about 20-30% in taxes.

Common Scenarios and Realistic Costs

To make this guide truly helpful, let us look at a few realistic scenarios. Please note that prices vary significantly by state and urban location. These are average estimates.

Scenario 1: Full Upper Denture

-

Total Fee (at Heartland-supported office): $1,800 – $2,500

-

Insurance Coverage (50% after deductible): $850 – $1,200

-

Your Estimated Out-of-Pocket: $950 – $1,300

Note: If you need immediate dentures (placed right after extractions), the cost is usually higher because it involves more appointments.

Scenario 2: Single Dental Implant (Tooth #19)

-

Total Fee (Implant + Abutment + Crown): $3,500 – $5,000

-

Insurance Coverage (If covered at 50%): $1,750 – $2,500 (up to annual max)

-

Your Estimated Out-of-Pocket: $1,750 – $2,500

Note: If the annual maximum is $1,500, the insurance will stop paying once they hit that limit. You pay the rest.

Scenario 3: Implant-Supported Lower Denture (2 Implants)

-

Total Fee: $6,000 – $10,000

-

Insurance Coverage: Varies wildly. Some plans pay 50% of implants but 0% of the denture; others pay the opposite.

-

Your Estimated Out-of-Pocket: $3,000 – $7,000

Alternative Financing Options

If your Heartland Dental insurance coverage for dentures and implants is not enough to cover the cost, do not give up. There are several ways to make treatment affordable.

In-House Membership Plans

Many Heartland-supported offices offer an in-house “membership” or “savings” plan. This is not insurance. It is a discount program. You pay a yearly fee (around $100-$300) and receive a set percentage off all services—often 15-20% off major procedures like implants and dentures. This is an excellent option for patients who do not have dental insurance or whose insurance has low annual maximums.

Third-Party Financing (CareCredit)

CareCredit is a healthcare credit card accepted at most Heartland-supported offices. They often offer promotional financing, such as:

-

6, 12, or 18 months: No interest if paid in full by the end of the term.

-

Extended plans: Lower monthly payments with fixed interest for longer terms (24, 36, 60 months).

Employer-Subsidized Loans

For employees of Heartland Dental, there may be internal programs or relationships with financial institutions that offer lower-interest loans for necessary medical and dental care. It is worth asking your HR representative if such a benefit exists.

Questions to Ask Your Heartland Dental Office

Before you schedule your consultation for dentures or implants, arm yourself with these questions. A good office will be happy to answer them.

-

“Can you verify my benefits and send a predetermination for the implant and crown separately?”

-

“Does my plan have a missing tooth clause?”

-

“Are there any waiting periods left for major services?”

-

“If I am an employee, do I get a discount for using an affiliated office?”

-

“What financing options are available if my insurance covers less than expected?”

-

“If I need extractions, are they covered under medical or dental insurance?”

The Connection Between Medical and Dental Insurance

Sometimes, dentures and implants are not just a dental issue. If you have a medical condition that necessitates the removal of teeth (such as radiation therapy for cancer, or a severe infection requiring hospitalization), the extraction portion may be covered by your medical insurance.

Furthermore, if you are getting implant-supported dentures to address a functional problem like severe malnutrition due to inability to chew, some medical plans are beginning to contribute to these costs. It is rare, but it is worth asking your dentist if they have ever successfully billed medical insurance for your specific case.

Frequently Asked Questions (FAQ)

1. Does Heartland Dental offer free dental implants?

No, Heartland Dental does not offer free implants. However, if you are an employee, you may have access to discounted treatment within the network. For patients, treatment is fee-for-service, though insurance and financing can help manage costs.

2. How long do I have to wait for implant coverage?

If you have a new dental plan, you typically wait 12 months for major services. Check your policy’s “waiting period” section. Some employer plans waive waiting periods if you had prior coverage.

3. Will my insurance cover the entire cost of dentures?

Almost never. Most standard plans cover 50% of the cost. You are responsible for the remaining 50%, plus the deductible and any costs exceeding the annual maximum.

4. Can I use my Heartland Dental employee insurance at any dentist?

It depends on your specific plan. Typically, to maximize benefits, you must visit a Heartland-supported office. If you go out-of-network, you may still have coverage, but the reimbursement rates are usually lower, and you may be responsible for balance billing.

5. What is a predetermination, and should I get one?

A predetermination is a request sent to your insurance company to calculate exactly what they will pay for a specific treatment plan. You should always get one for implants or dentures. It takes 2-4 weeks but prevents billing surprises.

6. Are mini-implants covered by insurance?

Mini-implants are often used to stabilize lower dentures. Coverage varies. Some plans treat them like standard implants; others do not cover them at all because they are sometimes considered a less traditional treatment. Always verify coverage in writing.

Conclusion

Navigating Heartland Dental insurance coverage for dentures and implants requires understanding the difference between patient and employee benefits. While most plans cover dentures at 50% and implants inconsistently, proactive steps like requesting predeterminations and timing treatment can significantly reduce costs. By working closely with your local Heartland-supported office and exploring financing options, you can achieve a functional and beautiful smile without financial stress.