United Concordia Dental Orthodontics Coverage: A Complete Guide to Braces & Invisalign

If you are considering braces for yourself or your child, you are likely looking at your insurance policy with a mix of hope and confusion. Dental insurance is complex, and orthodontic coverage often sits in its own category, separate from routine cleanings and fillings.

United Concordia Dental is one of the largest dental insurers in the United States, trusted by military families (Tricare), federal employees, and large corporate groups. But understanding what your specific plan covers regarding orthodontics can feel like deciphering a secret code.

Does your plan cover metal braces? What about Invisalign? Is there an age limit? How does the “lifetime maximum” actually work?

This guide is designed to answer all those questions. We will break down the specifics of United Concordia dental orthodontics coverage, helping you navigate the fine print so you can make informed decisions without any nasty surprises.

Understanding the Basics: What Is Orthodontic Coverage?

Before we dive into the specifics of United Concordia, it is important to understand how orthodontic coverage differs from standard dental coverage.

Most dental insurance plans operate on a model that covers preventive care (cleanings, exams) at 100%, basic procedures (fillings, extractions) at 70% to 80%, and major procedures (crowns, bridges) at 50%. Orthodontics, however, is usually treated as a separate specialty benefit.

Key Differences

-

Lifetime Maximum (LTM): Unlike regular dental benefits that reset annually, orthodontic benefits usually have a lifetime maximum. This is the total amount the insurance will pay for orthodontic treatment over the course of your (or your dependent’s) entire life.

-

Deductible: Some plans require you to meet a separate orthodontic deductible, or a general annual deductible, before coverage kicks in.

-

Age Limits: Many plans limit orthodontic coverage to dependents under the age of 19 or 26. Adult orthodontics (19+) is often excluded or has a separate, lower lifetime maximum.

United Concordia offers a wide variety of plans, from the high-tier “Alliance” network plans to more basic employer-sponsored plans. Because there is no single “United Concordia” plan, the specifics can vary drastically.

Types of United Concordia Plans

To understand your coverage, you first need to identify which type of United Concordia plan you have. The company structures its offerings into several distinct categories.

United Concordia Alliance

The Alliance network is United Concordia’s largest and most preferred network. If you have an Alliance plan, you typically have access to the highest level of benefits. Dentists in this network agree to discounted fees, which means your out-of-pocket costs are lower. For orthodontics, Alliance plans often offer the most generous lifetime maximums.

United Concordia National

This network is slightly smaller than Alliance but still offers substantial discounts. If your employer offers a “PPO” plan, it is likely tied to the National network. Orthodontic coverage here is generally good, though the lifetime maximum might be slightly lower than an elite Alliance plan.

Tricare Dental Program (TDP)

This is a significant segment of United Concordia’s business. United Concordia administers the Tricare Dental Program for active-duty family members and National Guard/Reserve members. Under Tricare, orthodontic coverage is available, but it comes with very specific rules regarding pre-authorization, medical necessity, and age limits.

Federal Employees Dental Program (FEDVIP)

United Concordia is a major carrier for federal employees. FEDVIP plans offer different tiers (High Option, Standard Option). The High Option usually includes robust orthodontic coverage for both children and adults, while the Standard Option may offer a more limited benefit or require longer waiting periods.

Important Note: If you are a federal employee or a military family, your plan summary is critical. Tricare and FEDVIP plans have specific brochures that dictate coverage rules differently than commercial employer plans.

Typical Orthodontic Coverage Details

While plans vary, we can look at the typical structure of United Concordia dental orthodontics coverage. Most plans follow a standard formula.

Lifetime Maximums

The lifetime maximum is the most important number on your policy regarding braces.

-

Typical Range: For most employer-sponsored United Concordia plans, the orthodontic lifetime maximum ranges from $1,000 to $3,500 per person.

-

Tricare: Tricare Dental Program often covers up to 50% of the allowed amount with no set dollar maximum for children, but with strict age limits.

-

High-End Plans: Some federal or corporate plans offer a lifetime maximum of $2,500 to $3,500 for adults and children combined.

Coverage Percentage

Unlike a filling where you pay a copay at the time of service, orthodontic coverage is usually paid out in installments.

-

Most United Concordia plans cover 50% of the orthodontic fee (for covered services).

-

The patient is responsible for the remaining 50%.

-

If you use an in-network provider, the 50% is based on the negotiated network fee. If you go out-of-network, the 50% is based on “usual and customary” rates, which may be lower than the dentist’s actual fee, leaving you with a larger balance.

Age Limitations

This is a major point of confusion. Many United Concordia plans separate orthodontic benefits by age.

-

Child Orthodontics: Usually covered for dependents up to age 19 (or 26 depending on the plan and student status). The lifetime maximum is fully available.

-

Adult Orthodontics: Many plans either exclude adult orthodontics entirely or offer a separate, smaller lifetime maximum (e.g., $1,000 to $1,500) for those over 19.

Waiting Periods

If you are a new enrollee in a United Concordia plan, you may face a waiting period for orthodontic services.

-

Typical Waiting Period: 12 to 24 months.

-

If you have had continuous dental coverage prior to joining, you may be able to waive the waiting period with a “creditable coverage” letter.

-

Note: Tricare and some employer plans may waive waiting periods for dependents if they are transferring from another plan.

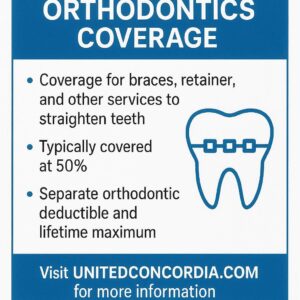

Braces vs. Invisalign: What Does United Concordia Cover?

A common question we hear is, “Does United Concordia cover Invisalign?” The answer is generally yes, but with caveats.

Most United Concordia plans do not differentiate between traditional metal braces and clear aligners (like Invisalign or ClearCorrect). They categorize both under the umbrella of “orthodontics.”

However, there are two scenarios to watch out for:

-

Medical Necessity: Some plans only cover orthodontics if there is a medical necessity (severe malocclusion, crossbite, etc.). If the treatment is purely cosmetic, coverage might be denied.

-

Lingual Braces: If you want braces placed on the inside of the teeth (lingual braces), some United Concordia plans consider this a “non-covered” service or a cosmetic upgrade. You will likely pay the difference in cost between standard braces and the lingual option.

Comparative Table: Braces vs. Invisalign Coverage

| Feature | Traditional Braces | Invisalign / Clear Aligners |

|---|---|---|

| Coverage Status | Usually covered (if plan includes ortho) | Usually covered (if plan includes ortho) |

| Lifetime Max | Applies to total treatment cost | Applies to total treatment cost |

| Cost Difference | Typically lower total fee | Often 10-20% higher fee |

| Age Limits | Subject to plan age limits | Subject to plan age limits |

| Pre-Authorization | Almost always required | Almost always required |

| Network Discount | Applies to in-network providers | Applies to in-network providers |

If you are leaning toward Invisalign, check if your specific dentist or orthodontist is in the United Concordia network. Not all providers who offer Invisalign are in-network for every insurance plan.

How to Check Your Specific Coverage

Because United Concordia administers so many different plans, looking up a generic list online is rarely helpful. To get accurate information, you need to look at your specific plan documents.

Here is a step-by-step guide to finding your orthodontic benefits:

-

Locate Your Member ID Card: Look at the back of your card. It usually lists a customer service number and a website URL.

-

Log In to the Portal: Go to the United Concordia website and register for an account. This is the most accurate way to see your benefits.

-

Look for “Orthodontia” or “Orthodontics”: In your benefits summary, scroll past the preventive and basic sections. Look for a specific section labeled “Orthodontics.”

-

Find the “Lifetime Maximum”: This is often listed as “Ortho Lifetime Max” or “Ortho LTM.”

-

Check “Age Limit”: Look for a notation that says “Child only” or “Up to age 19.”

Example of a Benefits Summary (Hypothetical)

| Service | In-Network Coverage | Out-of-Network Coverage | Notes |

|---|---|---|---|

| Orthodontic Diagnosis | 80% | 80% | Limited to 1 per 36 months |

| Orthodontic Treatment (Child) | 50% | 50% | Lifetime Max: $1,500; Age < 19 |

| Orthodontic Treatment (Adult) | 50% | 50% | Lifetime Max: $1,000; Age 19+ |

| Waiting Period | 12 Months | 12 Months | Waived with prior creditable coverage |

The Pre-Authorization Process

Before you or your child get braces, your orthodontist will likely need to submit a pre-authorization (or pre-determination) to United Concordia.

This is not just a formality; it is a crucial step.

-

The Orthodontist Submits: The orthodontist sends X-rays, photos, and a treatment plan to United Concordia.

-

Insurance Reviews: United Concordia reviews the case to confirm:

-

The patient is eligible (age, active coverage).

-

The treatment is medically necessary (if required by the plan).

-

The provider is in-network.

-

-

The Result: You receive a document stating what the insurance will pay, what the patient’s responsibility is, and the estimated timeline.

Why this matters: If you start treatment without pre-authorization, and the plan denies the claim, you are responsible for the full cost. Always wait for the written pre-authorization before signing a contract with the orthodontist.

Cost Scenarios: What You Will Actually Pay

To give you a realistic picture, let’s look at typical costs associated with United Concordia dental orthodontics coverage.

Orthodontic treatment in the United States typically ranges from:

-

Traditional Metal Braces: $3,000 – $7,000

-

Invisalign/Clear Aligners: $3,500 – $8,000

Scenario 1: Excellent Plan (High Option FEDVIP or Large Employer)

-

Total Treatment Cost: $5,500 (In-Network negotiated rate)

-

Insurance Covers: 50% ($2,750)

-

Lifetime Max Applied: $2,750 (assuming no cap, or cap not reached)

-

Your Estimated Cost: $2,750 (plus any deductible)

Scenario 2: Standard Employer Plan (Typical)

-

Total Treatment Cost: $6,000 (In-Network)

-

Insurance Covers: 50% ($3,000)

-

Lifetime Max Cap: $1,500 (This is the key difference)

-

Your Estimated Cost: $4,500 ($3,000 patient portion + $1,500 that insurance would have paid if not capped)

In Scenario 2, the insurance pays $1,500, and you pay $4,500. This highlights why the lifetime maximum is so critical. If the lifetime maximum is low, you are essentially self-paying for a large portion of the braces.

Scenario 3: Tricare Dental Program (Active Duty Family)

-

Total Treatment Cost: $5,000 (Network)

-

Insurance Covers: 50% ($2,500)

-

Lifetime Max: No set dollar cap (for children)

-

Your Estimated Cost: $2,500

-

Note: Tricare often requires that the child be enrolled in the program for 12 months before orthodontic benefits begin.

Maximizing Your United Concordia Orthodontic Benefits

If you know you need braces, you want to squeeze every dollar out of your insurance plan. Here are strategies to maximize your United Concordia benefits.

1. Use an In-Network Provider

This is the single most effective way to save money. United Concordia negotiates fees with in-network orthodontists. Even if your plan covers 50%, the base fee is lower. Out-of-network providers can charge whatever they want, leaving you to pay the difference between the insurance allowance and the actual bill.

2. Understand the Billing Timeline

Orthodontic treatment is usually billed in monthly installments over 18 to 24 months. Insurance typically pays their portion in the same installments.

-

If you have a flexible spending account (FSA) or health savings account (HSA), you can use those pre-tax dollars to pay your monthly portion.

-

If you are planning to change jobs, be aware that orthodontic benefits do not usually transfer. If you leave your employer mid-treatment, United Concordia will stop paying. You may want to delay treatment until you are confident you will stay with the employer for the duration of the treatment.

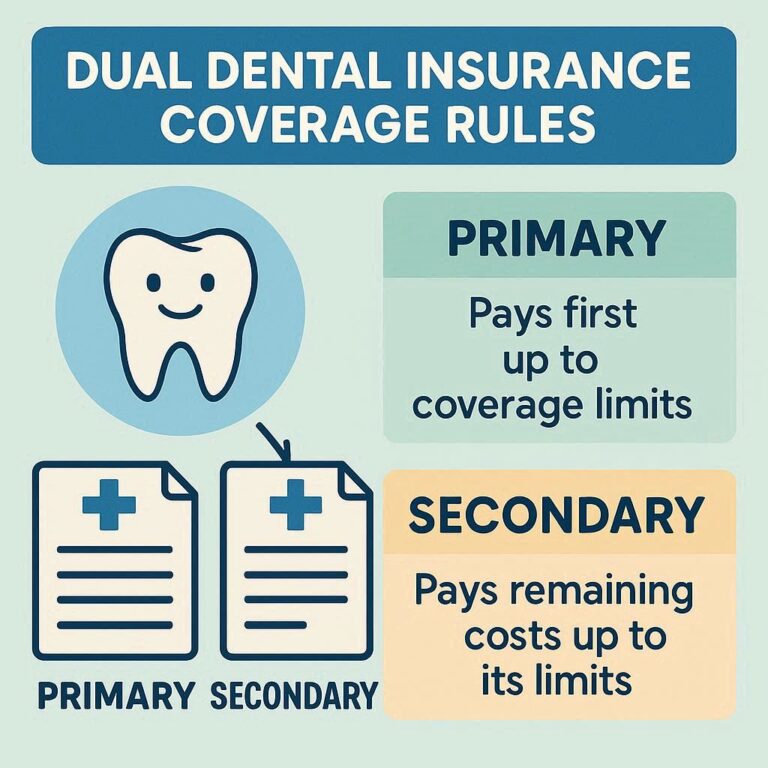

3. Coordinate Benefits

If you and your spouse both have dental insurance, you may be able to coordinate benefits.

-

Primary vs. Secondary: If you both cover your child, United Concordia might act as the primary or secondary payer. In some cases, you can combine lifetime maximums or get the secondary plan to cover a portion of the remaining balance.

-

Call United Concordia and ask about “coordination of benefits” to see if this applies to your family.

4. Time Your Treatment

If your plan has a waiting period, do not start treatment until it is satisfied. Similarly, if your child is approaching the age limit (e.g., 19), ensure the treatment plan fits within the coverage window. If the treatment takes 24 months and the child turns 19 in 12 months, coverage may stop at age 19.

Common Exclusions and Limitations

It is just as important to know what is not covered as what is. Reading the exclusions section of your United Concordia plan can save you from unexpected bills.

-

Treatment Started Before Coverage: If you started braces with a previous insurer or paid out-of-pocket, United Concordia will not retroactively cover them.

-

Cosmetic Treatment: If the orthodontic treatment is deemed purely for cosmetic purposes and not for functional bite correction, it may be excluded.

-

Retainers After Treatment: While the initial braces/aligners are covered, replacement retainers lost or broken after treatment may not be covered.

-

Surgical Orthodontics: If you need jaw surgery (orthognathic surgery) in conjunction with braces, this often falls under medical insurance, not dental. You will need to coordinate with your medical plan.

-

Missing Teeth: Orthodontics to create space for implants or bridges is sometimes covered, but the implants themselves are usually a separate major service with a different waiting period.

United Concordia for Adults: What to Expect

If you are an adult seeking orthodontic treatment, your coverage landscape looks different than it does for a child.

Many United Concordia plans offered through employers have a bifurcated benefit structure.

Typical Adult Orthodontic Limitations

-

Lower Lifetime Maximum: Instead of $1,500 to $2,500, adult coverage might max out at $1,000.

-

Exclusion: Some plans exclude adults entirely. If you are over 19, the orthodontic section of the brochure might simply say “Not Covered.”

-

Tricare: Tricare does not cover orthodontic treatment for active-duty service members. It covers dependents (children) but generally not the service member themselves for braces unless related to a severe, documented medical condition.

If you are an adult with a plan that excludes orthodontics, you have a few options:

-

Upgrade during open enrollment: If your employer offers a “buy-up” or high option plan, switch to that during open enrollment to gain orthodontic benefits for the next year.

-

Use an FSA/HSA: Even if insurance doesn’t cover it, you can use pre-tax dollars to pay for braces, effectively getting a 20-30% discount depending on your tax bracket.

-

Ask about payment plans: Many orthodontists offer in-house financing. Combining an in-network discount (even without insurance paying 50%) with a payment plan can make treatment manageable.

Realistic Scenarios: Frequently Asked Situations

To make this guide as practical as possible, let’s walk through a few common scenarios that readers often face.

Scenario A: The Child Needs Phase I (Early) Treatment

*“My 8-year-old needs an expander and partial braces. How does that affect future coverage?”*

Orthodontic treatment is often split into Phase I (early intervention) and Phase II (full braces). United Concordia views these as two separate treatment episodes. However, the lifetime maximum applies to the sum total.

If your plan has a $1,500 lifetime maximum, and Phase I costs $2,000 (insurance pays 50% = $1,000), you have used $1,000 of the $1,500 max. When Phase II is needed in a few years, you will only have $500 left in benefits. You will be responsible for the remaining 50% of the Phase II costs plus the $1,000 gap in the lifetime max.

Tip: Ask your orthodontist to provide a long-term treatment plan so you can budget for the total out-of-pocket across both phases.

Scenario B: Moving States Mid-Treatment

“We are relocating from Texas to Virginia. My child has braces with a United Concordia in-network orthodontist in Texas. What happens?”

This is a tricky situation. Your insurance is still active, but you need to find a new in-network orthodontist in Virginia who is willing to “take over” the case.

-

Transfer Fees: The new orthodontist may charge a transfer fee to take over the existing braces. United Concordia usually does not cover transfer fees.

-

Remaining Benefits: The remaining portion of your lifetime maximum will transfer. If insurance had only paid $800 of a $1,500 max, you still have $700 left to apply to the remaining treatment time.

-

Coordination: You must ensure the old orthodontist releases the records and the new orthodontist files the correct claims under the same pre-authorization number.

Scenario C: Treatment Goes Over the Estimated Time

“The orthodontist said 18 months, but we are going on 24 months. Will insurance still pay?”

United Concordia typically pays based on the total contracted fee, not the number of months. If the total treatment fee was $5,000 and the insurance agreed to pay $2,500 (50%), they will pay that amount regardless of whether it takes 12 months or 30 months. They usually pay in monthly installments until their portion of the total fee is exhausted. You will continue to pay your monthly portion until the total fee is paid in full.

How to Handle Denials and Appeals

Sometimes, United Concordia may deny a pre-authorization or a claim for orthodontic treatment. This can be frustrating, especially if you were expecting coverage.

Common Reasons for Denial

-

Missing Pre-Authorization: Starting treatment without getting approval first.

-

Age Limit Exceeded: The dependent turned 19 (or the plan’s cut-off age) before the start of treatment.

-

Lack of Medical Necessity: The plan only covers severe malocclusions (like a 7mm overjet) and the patient’s case is mild.

-

Waiting Period Not Satisfied: You enrolled 6 months ago, but the waiting period is 12 months.

Steps to Appeal

-

Read the Explanation of Benefits (EOB): The denial letter will have a code (e.g., CO-97, PR-204). Look up what this means.

-

Contact Your Orthodontist: Often, the denial is due to missing paperwork. Your orthodontist’s billing coordinator can resubmit with additional X-rays or a more detailed narrative.

-

File a Formal Appeal: If the orthodontist cannot resolve it, you have the right to appeal. United Concordia’s website and the back of your member card provide instructions for filing a grievance or appeal. You typically have 180 days from the date of the denial to file.

-

Request a Peer Review: For complex medical necessity denials, you can request a peer-to-peer review where your orthodontist speaks directly with a dental consultant at United Concordia.

Alternative Financing Options

If your United Concordia plan has a low lifetime maximum or excludes adult orthodontics, you may need to look beyond insurance to afford treatment.

Dental Discount Plans

Some families purchase a separate dental discount plan (not insurance) to supplement their United Concordia coverage. These plans offer a set discount (e.g., 20-30% off braces) at participating providers. While you don’t get a “co-pay,” you do get a guaranteed reduced fee.

Orthodontist In-House Financing

Most orthodontists offer interest-free payment plans. Typically, they require a down payment (often $500 to $1,500) followed by monthly payments over the course of treatment. Since insurance usually pays in monthly installments, this aligns well with their billing cycle.

CareCredit

CareCredit is a healthcare credit card that offers promotional financing (e.g., 12, 18, or 24 months interest-free). If your United Concordia coverage leaves a significant balance, using CareCredit can help you spread the cost without paying interest, provided you pay it off within the promotional period.

Conclusion

Understanding United Concordia dental orthodontics coverage comes down to knowing your specific plan details. The key factors—lifetime maximum, age limits, and network status—determine your actual out-of-pocket costs far more than the general “50% coverage” promise. By securing a pre-authorization, choosing an in-network provider, and planning for the lifetime cap, you can navigate the process confidently and avoid financial surprises.

Remember, every plan is unique. Take the time to log into your member portal or call the number on the back of your card. Armed with the right information, you can focus on what truly matters: achieving a healthy, confident smile.

Frequently Asked Questions (FAQ)

1. Does United Concordia cover braces for adults?

It depends on your specific plan. Many employer-sponsored plans offer a reduced lifetime maximum for adults (19+), while others exclude adult orthodontics entirely. Check your plan’s “Orthodontics” section for age limitations.

2. Does United Concordia cover Invisalign?

In most cases, yes. United Concordia usually classifies Invisalign and other clear aligners under the same orthodontic benefit as traditional braces. However, some plans may require a pre-authorization to confirm medical necessity.

3. How long do I have to wait for orthodontic coverage?

Most United Concordia plans have a waiting period of 12 to 24 months for major services like orthodontics. If you had prior dental coverage without a lapse, you may be able to waive this waiting period by providing proof of creditable coverage.

4. What is the lifetime maximum for orthodontics?

The lifetime maximum (LTM) is the total amount United Concordia will pay for orthodontic treatment over a person’s lifetime. It typically ranges from $1,000 to $3,500 depending on your plan. Once used, it does not reset.

5. How do I find an in-network orthodontist?

You can use the “Find a Dentist” tool on the United Concordia website. Filter your search by specialty (Orthodontics) and by your specific plan network (Alliance, National, etc.) to ensure you are seeing a participating provider.

Additional Resource

For the most accurate and personalized information regarding your plan, always refer to your official member account.

Link: United Concordia Member Login & Benefits Portal

Note: This article is for informational purposes only and does not constitute legal or medical advice. Insurance plans, coverage details, and benefits vary significantly by employer group, location, and policy type. Always consult your official plan documents and verify coverage with your insurance provider before beginning treatment.